Heart Attack Diagnostics Market Summary

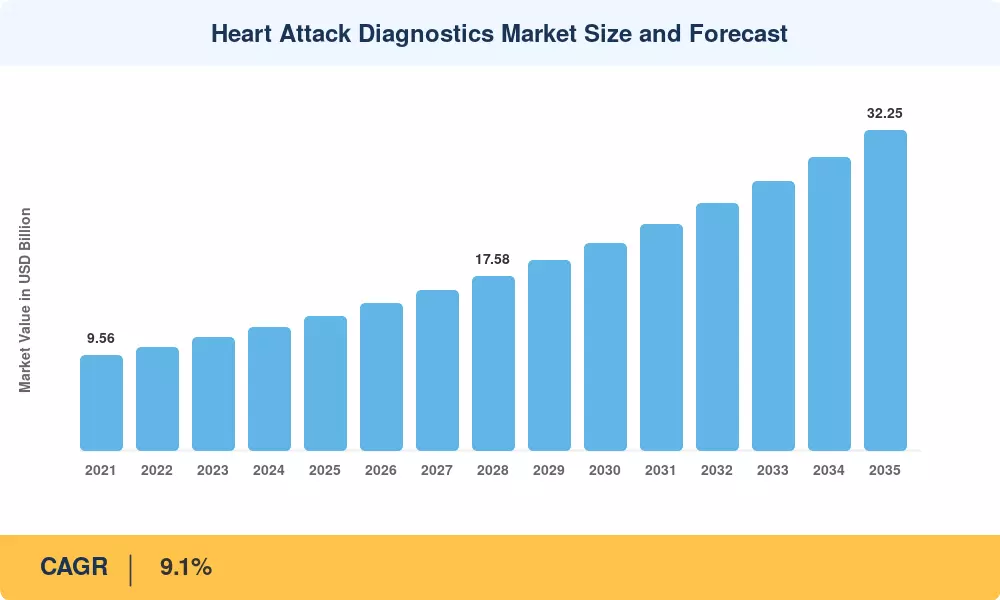

The Global Heart Attack Diagnostics Market size was valued at USD 13.55 Billion in 2025, and the market is projected to grow from USD 14.72 Billion in 2026 to USD 32.25 Billion by 2035, registering a CAGR of 9.1% during the forecast period 2026–2035. Two catalysts stand behind this trajectory: the World Health Organization's renewed push for universal cardiovascular screening in primary-care settings, and a wave of national reimbursement reforms—most prominently CMS's expanded coverage of high-sensitivity cardiac assays in the United States—that have made rapid rule-in/rule-out protocols financially viable for hospitals and freestanding labs alike [1][2].

Technology is reshaping every link in the diagnostic chain. Legacy single-marker immunoassays are giving way to multiplexed panels that quantify troponin, NT-proBNP, and emerging biomarkers on a single cartridge, while AI-augmented electrocardiogram platforms now detect ST-segment anomalies with sensitivity exceeding 95% in peer-reviewed trials [3]. The European Society of Cardiology's 2024 guideline update further accelerated adoption by endorsing zero-hour/one-hour algorithms built around high-sensitivity troponin assays, effectively mandating faster turnaround across EU member states [4].

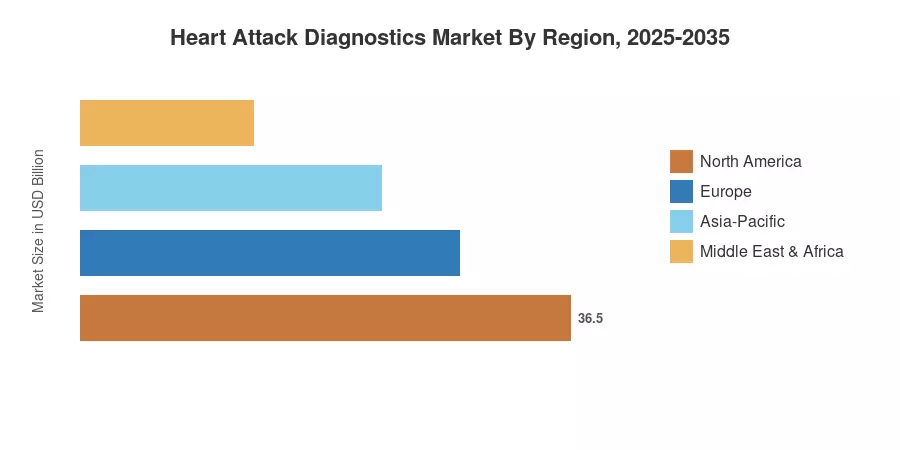

North America commands the largest slice of the heart attack diagnostics market with a 32.9% revenue share, followed by Europe at 27.1%. Asia-Pacific, however, is the fastest-growing region at an 11.2% CAGR through 2035, powered by India's Ayushman Bharat health-insurance expansion and China's county-hospital modernization program. As diagnostic workflows migrate from centralized labs to emergency departments, ambulances, and even patients' homes, the competitive landscape will continue to reward companies that pair analytical precision with connectivity and speed.

Key Report Takeaways

• By Test

- Blood tests held a 43.5% share of the heart attack diagnostics market in 2025, driven by universal adoption of high-sensitivity troponin protocols.

- Wearable and AI-driven ECG systems are forecast to expand at a 13.8% CAGR through 2035, reflecting growing point-of-care and remote-monitoring demand.

• By End User

- Hospitals accounted for 51.1% of global revenue in 2025, anchored by emergency-department spending on rapid-turnaround analyzers.

- Home-based and tele-cardiology settings are projected to grow at 15.2% CAGR, the fastest across all end-user channels.

• By Region

- North America contributed USD 4.46 billion in 2025 revenue, maintaining its position as the dominant market.

- Asia-Pacific is forecast to register the highest regional CAGR at 11.2% through 2035.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining top-down revenue modeling from device-manufacturer filings, bottom-up procedure-volume analysis from hospital discharge databases, and cross-validation against peer-reviewed epidemiological registries. Historical figures reflect actual shipments and reimbursement claims; forecast values apply the calibrated 9.1% CAGR with adjustments for anticipated regulatory and technology inflections.