Heat Pump Water Heater Market Summary

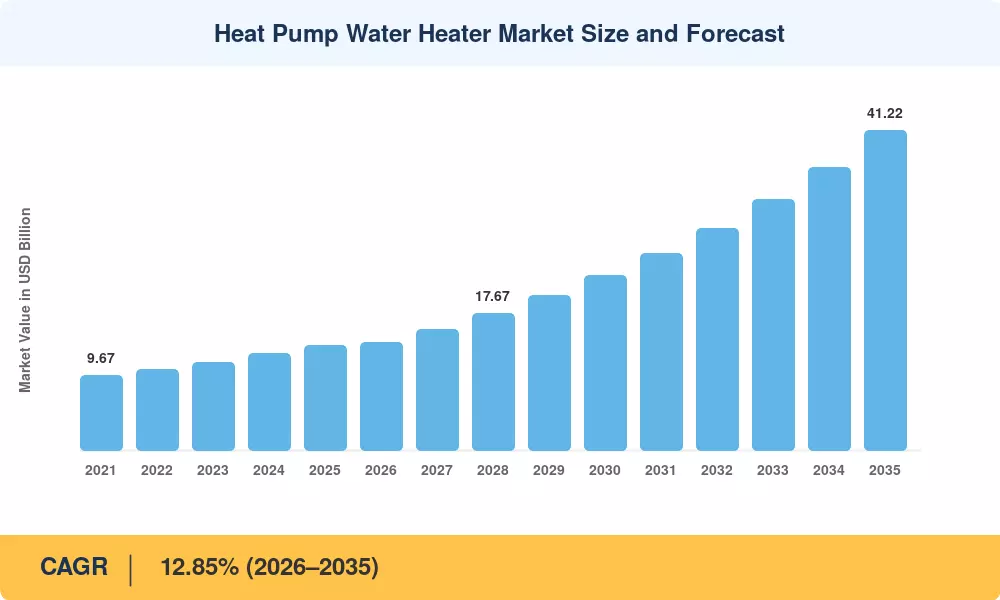

The Heat Pump Water Heater Market reached an estimated USD 13.58 Billion in 2025 and is positioned to grow from USD 13.87 Billion in 2026 to USD 41.22 Billion by 2035, registering a CAGR of 12.85% during the forecast period. Two policy catalysts are reshaping the landscape: the U.S. Department of Energy's April 2024 final rule on electric storage water heaters—effective May 2029—raises efficiency thresholds beyond the reach of conventional resistance elements, effectively mandating heat pump architectures for tanks above 35 gallons [1]. Simultaneously, European Union Regulation 2024/573 accelerates the shift to low-GWP refrigerants, compelling manufacturers to retool product lines years before compliance deadlines [2].

This technology transformation is dismantling the dominance of electric resistance and gas-fired storage water heaters. Where a conventional 50-gallon electric tank operates at a coefficient of performance near 1.0, modern heat pump units deliver COPs between 3.0 and 4.5, cutting energy consumption by 60–70%. The U.S. Inflation Reduction Act's Section 25C credit—covering 30% of installed costs up to USD 2,000—alongside state-level Household Energy Appliance Rebates, has compressed consumer payback periods to under four years in many jurisdictions [3]. Utilities are further layering demand-response incentives tied to CTA-2045-enabled units, positioning the Heat Pump Water Heater Market at the intersection of decarbonization policy and grid flexibility programs.

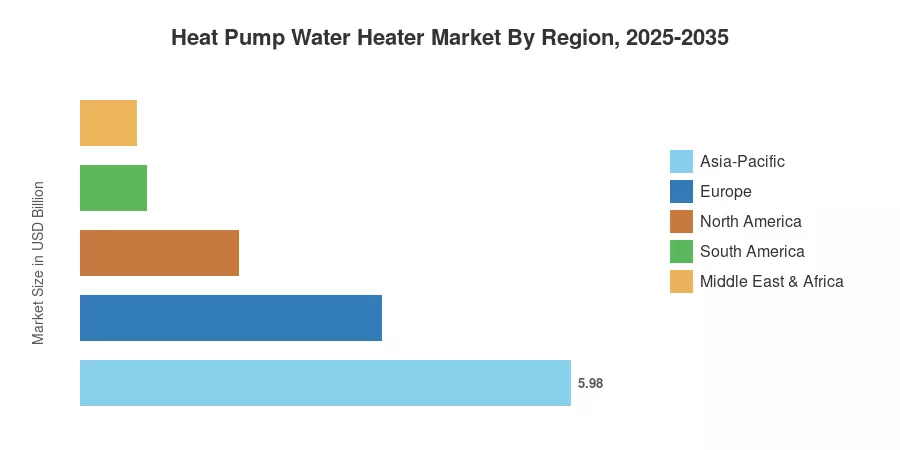

Asia-Pacific commands the largest share at roughly 44% of global revenue, anchored by aggressive adoption in China, Japan, and Australia. North America is the fastest-growing region with an estimated CAGR exceeding 14%, driven by federal standards and tax credits. Europe holds the second-largest share near 27%, propelled by the EU's energy performance directives and national building codes that increasingly favor all-electric thermal systems. As electrification mandates widen and refrigerant regulations tighten, the Heat Pump Water Heater Market is set for sustained double-digit expansion through 2035.

Key Report Takeaways

• By Technology

- Air-source heat pump water heaters captured approximately 67.5% of the Heat Pump Water Heater Market revenue in 2025, reflecting their lower installed cost and broad climate applicability.

- Ground-source systems are projected to expand at a 13.40% CAGR through 2035, the fastest among technology segments, owing to superior cold-climate performance.

• By Capacity

- Units above 500 L accounted for an estimated 41.2% share of the Heat Pump Water Heater Market in 2025, led by commercial hospitality and multifamily installations.

• By End User

- Residential end users represented roughly 62% of total demand, supported by rebate-driven retrofits and new-construction mandates in key markets.

• By Region

- Asia-Pacific held the dominant revenue position in the Heat Pump Water Heater Market, with China alone contributing over half of regional demand.

- North America's CAGR is projected to exceed 14% through 2035, the fastest among all regions, powered by DOE standards and IRA incentives.

- Europe maintained a 27% global share, supported by EU F-gas regulations and national heat pump subsidy schemes.

Market Size and Forecast (2021–2035)

Market size estimates draw on a triangulated methodology combining bottom-up installation volume data, manufacturer revenue filings, and top-down macroeconomic benchmarking against energy efficiency investment databases maintained by the IEA and national energy agencies [4].