Residential Air to Water Heat Pump Market Summary

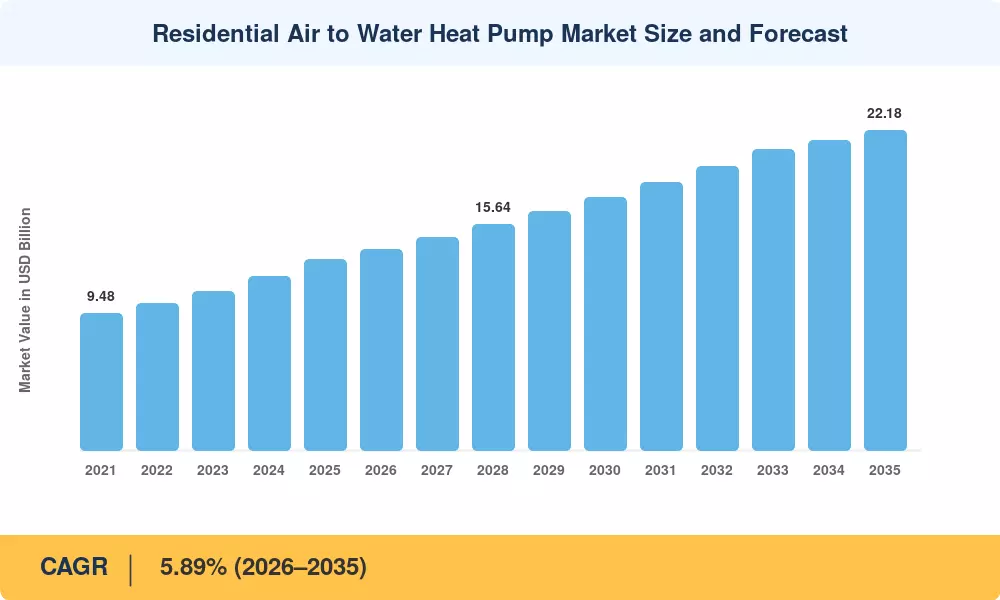

The Residential Air to Water Heat Pump Market reached an estimated USD 13.24 billion in 2025 and is projected to grow from USD 13.93 billion in 2026 to USD 22.18 billion by 2035, registering a CAGR of 5.89% during the forecast period. Aggressive decarbonization mandates—most visibly the EU's revised Energy Performance of Buildings Directive and the U.S. Inflation Reduction Act's 30% federal tax credits for qualifying heat pump installations—are converting policy ambition into real capital deployment [2]. Homeowners increasingly recognize that the total cost of ownership for a monobloc air-to-water heat pump now undercuts a natural-gas boiler within seven to nine years in most temperate climates, a crossover timeline that subsidies compress further.

A technology shift is well underway in the Residential Air to Water Heat Pump Market as legacy oil and gas boilers give way to inverter-driven, low temperature heat pump underfloor heating configurations. The IEA's 2024 Global Heat Pump Tracker estimated that global residential heat pump investment surpassed USD 75 billion, with R290 refrigerant heat pump residential models gaining rapid shelf space as manufacturers prepare for the EU F-Gas Regulation phase-down schedule through 2030 [3]. Hybrid boiler heat pump combo units bridge the confidence gap for homeowners in colder regions, combining a condensing gas backup with a primary hydronic heat pump radiator system.

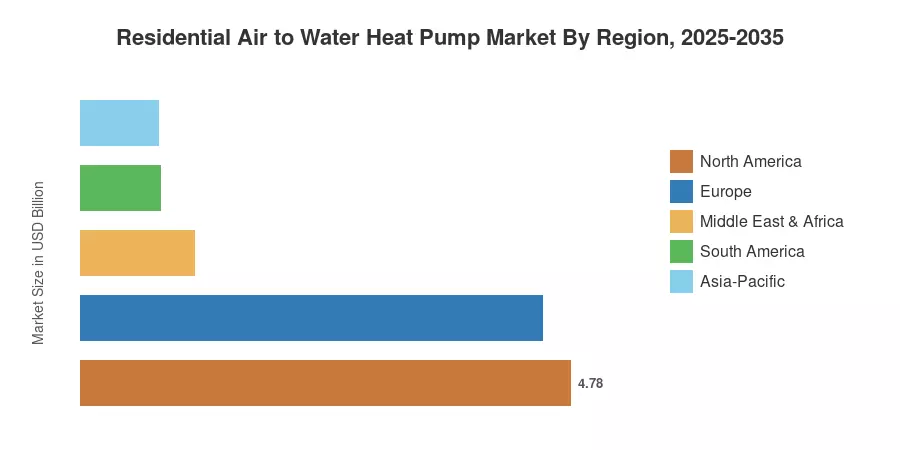

North America commands the largest regional share at roughly 36% of global revenue, buoyed by federal and state-level incentives across the U.S. and Canada Asia-Pacific follows with the second-largest share, driven by China's aggressive electrification push and Japan's longstanding adoption of split-system heat pumps. The Middle East & Africa region is the fastest-growing at an estimated 8.42% CAGR to 2035, as Gulf states pivot toward energy-efficient cooling-dominant systems in new residential developments. The Residential Air to Water Heat Pump Market is positioned for sustained expansion as grid decarbonization, refrigerant regulations, and falling hardware costs converge.

Key Report Takeaways

• By Type

- Split systems held the dominant position in the Residential Air to Water Heat Pump Market with approximately 44% revenue share in 2025, led by established deployment in Japan and Northern Europe

- Hybrid boiler heat pump combo configurations are projected to grow at a 9.50% CAGR through 2035, as they offer fallback heating capacity that reassures homeowners during extreme cold spells

- Monobloc air-to-water heat pump units are gaining traction in retrofit applications thanks to simplified outdoor-only installation requirements

• By Capacity & Application

- Units below 10 kW captured over 58% of the Residential Air to Water Heat Pump Market share in 2025, reflecting the predominance of single-family dwelling installations

- Multi-family residences represent the fastest-growing application segment at a 7.85% CAGR, driven by EU grant programs that subsidize building-wide hydronic heat pump radiator system retrofits

• By Region

- North America led with 36.1% of the Residential Air to Water Heat Pump Market in 2025, anchored by U.S. IRA incentives and Canadian greener homes programs

- Europe accounted for approximately USD 4.51 billion in 2025 revenue, supported by the REPowerEU plan's target of deploying 60 million heat pumps by 2030

- The Middle East & Africa region is forecast to achieve the highest CAGR at 8.42% through 2035

Market Size and Forecast (2021–2035)

MRFR's market sizing combines bottom-up shipment data from OEM disclosures, customs trade databases, and distributor surveys, cross-validated against top-down macroeconomic indicators including residential construction permits and heating fuel substitution rates.