HLA Typing Market Summary

The HLA Typing Market reached USD 0.85 billion in 2025 and is positioned to climb toward USD 1.78 billion by 2035, advancing at a 7.65% CAGR across the 2026–2035 forecast window from a 2026 starting base near USD 0.91 billion. Record organ-transplant volumes and the mainstreaming of precision medicine anchor this trajectory. Policy momentum reinforces it — the Medicare IOTA Model now rewards precise tissue matching through performance-based hospital payments, sharpening demand for accurate HLA Typing Market services across transplant programs.

A more profound transformation is significantly altering the manner in which laboratories operate. Serological assays and low-resolution antibody panels are being replaced by next-generation sequencing HLA analysis platforms that resolve alleles at full resolution. Venture investment exceeding USD 200 million across diagnostics startups since 2023 signals rising confidence in this transition toward immune gene matching at scale, as high-throughput molecular assays reduce turnaround times and improve match accuracy.

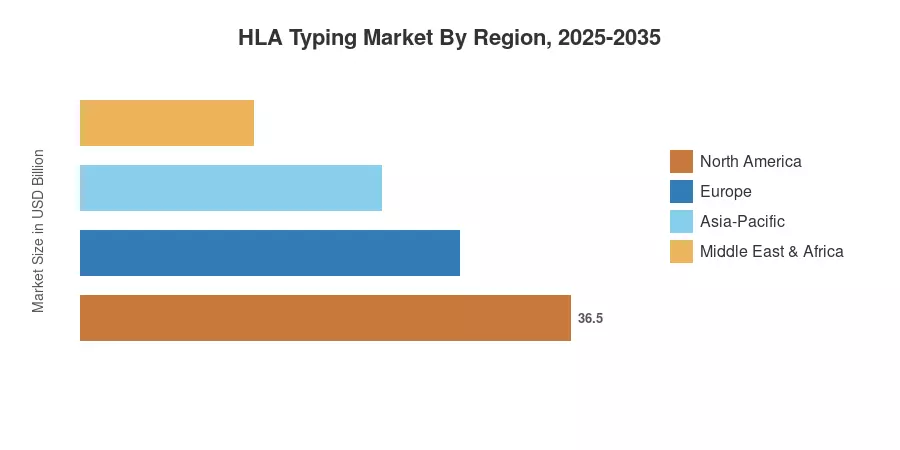

North America is the market leader in the HLA Typing Market, with a 41.8% revenue share, which is bolstered by reimbursement clarity and a dense transplant infrastructure. Asia-Pacific is the fastest-growing region, with a compound annual growth rate (CAGR) of 9.45%, which is attributed to the expansion of donor registries. Europe is the second-largest region, driven by standardized accreditation standards. Players that integrate cloud bioinformatics with sequencing depth will be advantageous in the forthcoming decade.

Key Report Takeaways

• By Technology

- Molecular assays command the largest revenue concentration in human leukocyte antigen testing, holding a 54.9% share of technology demand

- Non-molecular serological methods are advancing at an 8.15% CAGR as confirmatory tools within tissue matching diagnostics

• By End-user

- Diagnostic testing dominates application demand within the HLA Typing Market, contributing roughly USD 0.58 billion in 2025

- Research applications are expanding at a 9.65% CAGR as immune gene matching enters drug discovery pipelines

- Commercial service providers lead end-user demand with a 43.5% share

• By Regional

- North America retains dominance with a 41.8% revenue share of the HLA Typing Market

- Asia-Pacific posts the fastest regional expansion at a 9.45% CAGR

Market Size and Forecast (2021–2035)

Market sizing draws on transplant-volume registries, laboratory revenue disclosures, reimbursement databases, and triangulation against comparable published estimates. Historical figures (2021–2024) reflect reported laboratory activity; forecast years apply a calibrated 7.65% CAGR tied to transplant growth and sequencing adoption.

.webp?v=1783416124)