Human Capital Management Software Market Summary

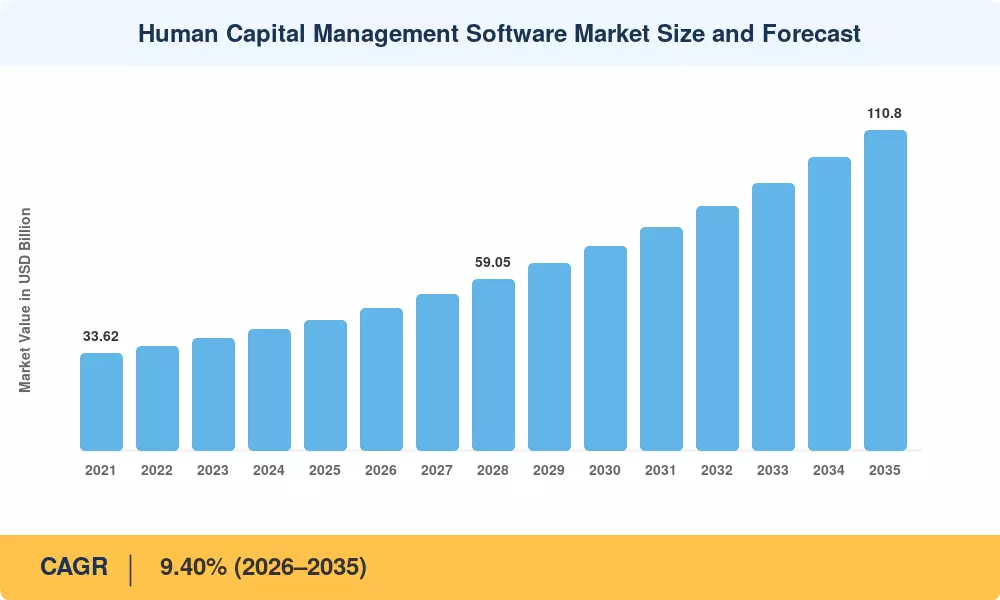

The Human Capital Management Software Market reached an estimated USD 45.10 billion in 2025 and is projected to grow from USD 49.34 billion in 2026 to USD 110.80 billion by 2035, registering a CAGR of 9.40% during the forecast period. Two catalysts are accelerating this trajectory: enterprises racing to embed generative-AI copilots into payroll and talent workflows, and governments worldwide digitizing tax administration and mandating real-time payroll reporting. These twin forces are converting discretionary HR technology budgets into mandatory compliance-driven investments [1].

The monolithic architectures on which legacy on-premises HR suites are built are being replaced by cloud-native platforms that consolidate payroll, benefits, recruiting, learning and analytics into a single data layer. expects global spending on corporate software will approach USD 1.1 trillion in 2025, with HR technology taking a significant part as organizations attempt to cut service-desk resolution times from days to minutes through AI-powered self-service [2]. The vendor differentiator currently comes in the form of ISO 27001 and SOC 2 Type II certifications that address data-sovereignty concerns without losing scalability.

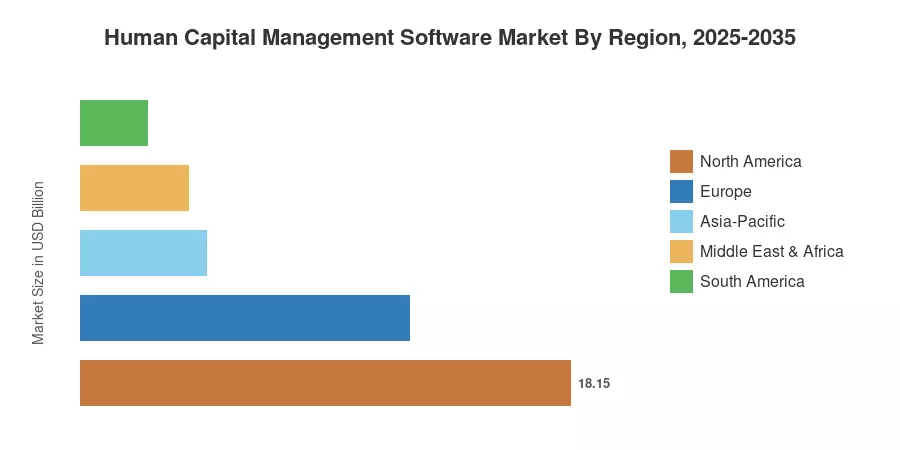

North America accounts for over 40.25% of the Human Capital Management Software Market, supported by mature cloud usage throughout the Fortune 500. Asia-Pacific is the fastest-growing market at 10.37% CAGR through 2035, with new deployments fueled by India’s Digital India program and China’s enterprise SaaS wave. Europe is the second-largest market with around 27% share of this market. Data governance rules in the GDPR age are a boon for integrated HCM solutions. As hybrid work patterns are here to stay, the runway for growth in the business is extending well into the next decade.

Key Report Takeaways

• By Solution

- Payroll management captured roughly 47% of the Human Capital Management Software Market revenue in 2025, reflecting the mission-critical nature of compliant payroll processing across multi-country operations.

- Learning and development is the fastest-growing solution segment, expanding at a 10.50% CAGR through 2035 as enterprises invest in upskilling and reskilling programs.

• By Organization Size

- Large enterprises represented approximately USD 30.01 billion of the Human Capital Management Software Market in 2025, while small and medium enterprises are advancing at a 9.76% CAGR.

• By Geography

- North America led the Human Capital Management Software Market with 40.25% revenue share in 2025.

- Asia-Pacific is projected to record the highest regional CAGR of 10.37% between 2026 and 2035.

- The BFSI vertical commanded roughly 24.5% of spending in 2025, while healthcare is the fastest-growing vertical at an 11.80% CAGR.

Market Size and Forecast (2021–2035)

The sizing technique used by Market Research Future (MRFR) includes bottom-up revenue modeling based on financial disclosures shared by vendors and validation against IT spending benchmarks from primary interviews with over 120 enterprise HR technology users across five regions. Historical data are real vendor revenues, forecast values are based on a calibrated CAGR, commensurate with macroeconomic indices and technology adoption curves.