Hybrid Operating Room Market Summary

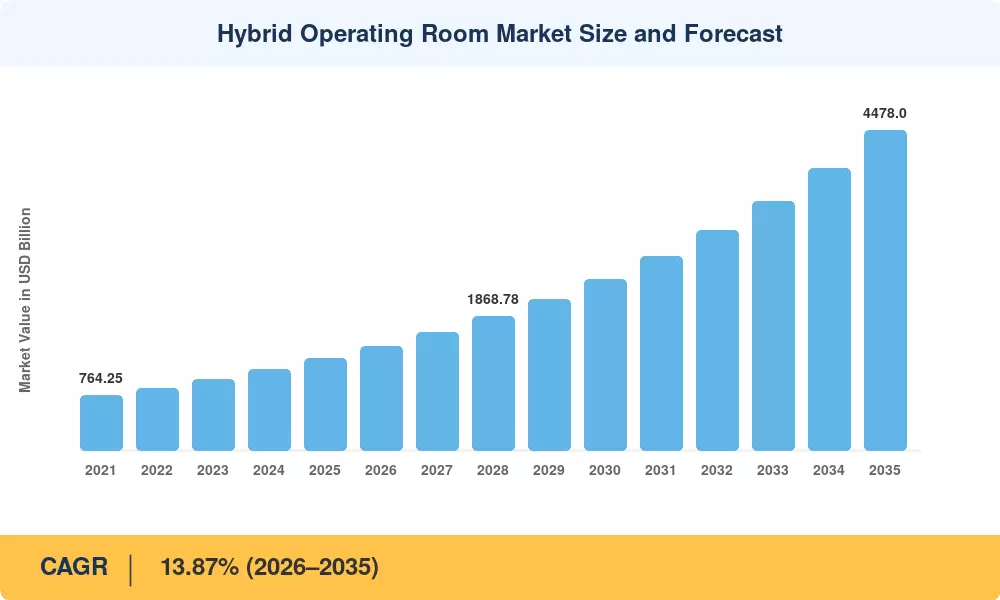

The Hybrid Operating Room Market reached an estimated USD 1,285 Million in 2025, and MRFR projects the sector will grow from USD 1,463 Million in 2026 to USD 4,478 Million by 2035 at a CAGR of 13.87% during 2026–2035. This acceleration is rooted in hospital capital-expenditure cycles that increasingly prioritize combined surgical imaging rooms over single-function suites, alongside government infrastructure grants — such as USAID's USD 1.4 million commitment to LAU Medical Center-Rizk Hospital in 2022 — that directly fund intraoperative imaging suite installations in underserved regions [2].

A quiet but decisive transformation is reshaping surgical infrastructure. Legacy standalone catheterization labs and conventional operating theaters are giving way to fluoroscopy-equipped OR configurations that merge real-time surgical imaging with open and minimally invasive workflows in a single environment. Hospitals investing USD 2–4 million per cardiovascular hybrid suite are betting that procedural consolidation will cut patient transfers, reduce complication rates, and shorten average length-of-stay — economics validated by multi-center outcomes studies published in 2023 [3].

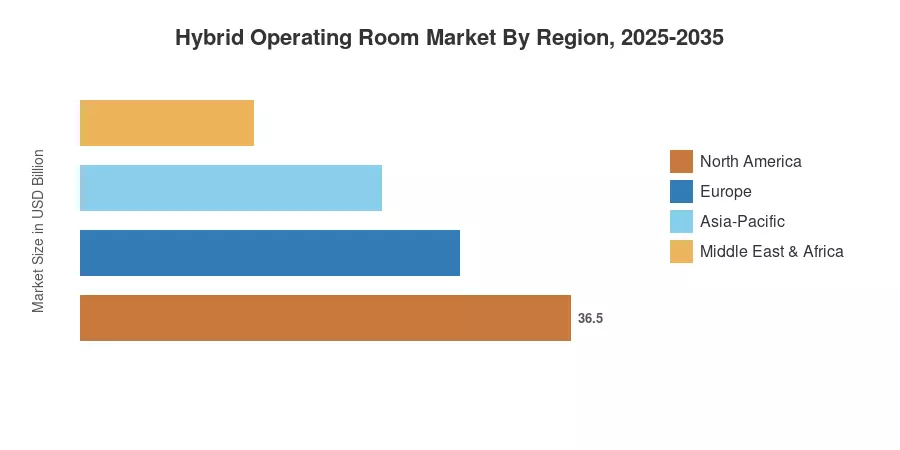

North America commands roughly 38% of the Hybrid Operating Room Market, driven by high procedural volumes and robust reimbursement frameworks. Asia-Pacific is the fastest-growing region at an estimated 15.4% CAGR through 2035, fueled by hospital construction booms in China and India. Europe holds the second-largest share, near 28%, anchored by Germany and the United Kingdom's cardiothoracic centers of excellence The next decade will reward early movers in real-time surgical imaging facility deployment across both mature and emerging healthcare systems.

Key Report Takeaways

• By Equipment

- Diagnostic Imaging Systems captured approximately 47% of the Hybrid Operating Room Market in 2025, powered by demand for fixed C-arm and angiography platforms inside intraoperative imaging suites

- Operating Room Fixtures are forecast to register the strongest segment CAGR through 2035 as modular ceiling-mounted booms and surgical lighting upgrades become standard in combined surgical imaging room retrofits

• By Application

- Cardiovascular Surgery dominates the Hybrid Operating Room Market at an estimated USD 520 Million in 2025, reflecting transcatheter aortic valve replacement (TAVR) procedure growth

- Neurosurgery is gaining traction as intraoperative MRI integration within fluoroscopy-equipped OR suites improves tumor-resection precision

• By Region

- North America leads globally with a 38% share of the Hybrid Operating Room Market, supported by CMS procedural reimbursement updates

- Asia-Pacific's 15.4% CAGR reflects aggressive hospital modernization programs across China, India, and Japan that prioritize real-time surgical imaging facilities

Market Size and Forecast (2021–2035)

MRFR's market-sizing methodology combines bottom-up revenue aggregation from equipment OEMs with top-down validation using hospital construction databases, surgical-procedure registries, and published capital-expenditure filings. Historical figures (2021–2024) are reconciled against company annual reports, while the forecast (2026–2035) applies a segment-weighted compound growth model calibrated to demographic, regulatory, and technology adoption drivers.

.webp?v=1783335279)