Hydrazine Hydrate Market Summary

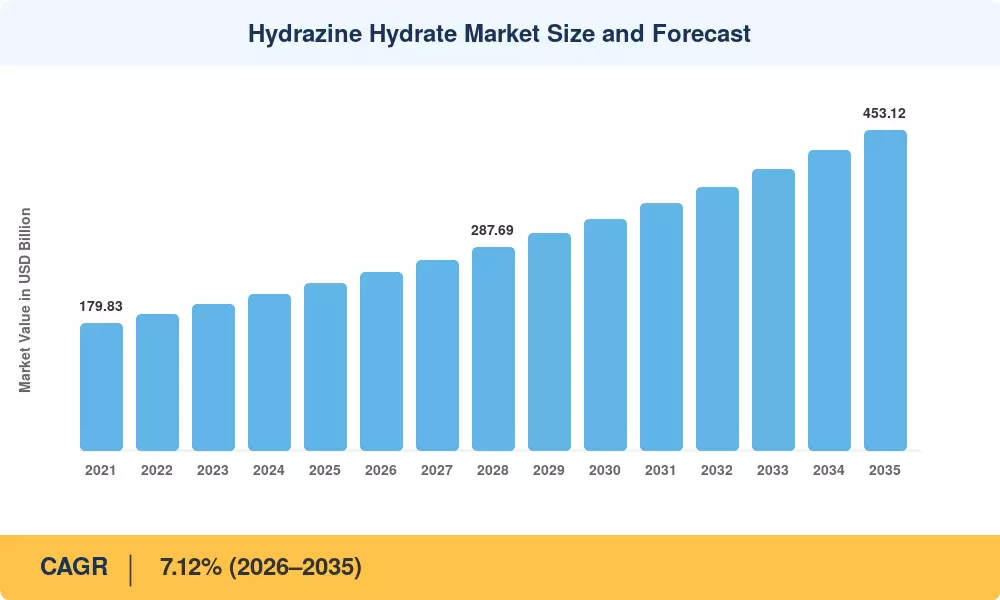

The Hydrazine Hydrate Market reached an estimated 236.80 kilotons in 2025 and is projected to grow from 253.40 kilotons in 2026 to approximately 453.12 kilotons by 2035, registering a CAGR of 7.12% across the forecast window. This expansion is anchored by tightening water treatment regulations under the US EPA's Boiler MACT Rule and the EU Industrial Emissions Directive, both of which mandate enhanced boiler oxygen scavengers and corrosion control chemicals in thermal power and district heating systems[2]. Capital commitments exceeding USD 1.2 billion for new agrochemical intermediate production capacity across India and China are accelerating the consumption of hydrazine hydrate as a pharmaceutical intermediate and polymerization catalyst.

The hydrazine hydrate market's supply economics are changing as a result of a major process change. Modern H2O2-ketazine route facilities, which reduce energy intensity by 30–35% and essentially remove chlorinated waste streams, are gradually displacing legacy Raschig-process plants, which were previously the foundation of global output [3]. Lonza's process-intensification effort and Arkema's EUR 180 million expansion at Lannemezan serve as examples of how integrated companies are using their on-site hydrogen peroxide capacity and experience in fine chemical synthesis to improve their cost positions. For lightweight automobile foams, where OEM demand increased 8% year over year in 2024, chemical blowing agents made from high-purity hydrazine hydrate are still essential [4].

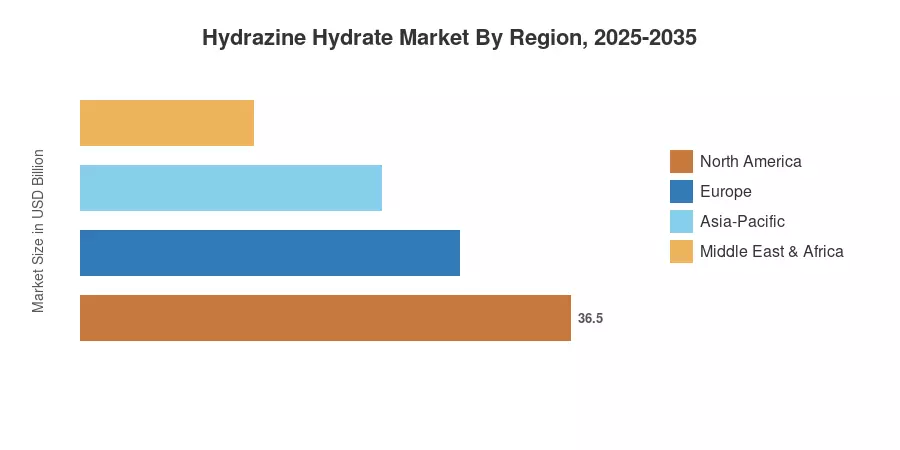

Due to India's growing pharmaceutical API industry and China's hegemony in agricultural intermediates, the Asia-Pacific accounts for about 56.10% of global volume. Additionally, the region reports the fastest CAGR through 2035, at 7.72%. The demand for specialty chemical compounds in aircraft propulsion and water treatment chemicals procurement throughout Nordic power utilities sustains Europe's second-largest position, with roughly 20.50% of the market North America comes in second, helped by orders for defense-grade propellants and the use of industrial reducing agents in petrochemical refining.

Key Report Takeaways

• By Production Process

- The Bayer Ketazine Process accounted for 47.90% of the Hydrazine Hydrate Market in 2025, reflecting its mature installed base and lower capital thresholds

- The H₂O₂–Ketazine Process is set to advance at a 7.85% CAGR through 2035, driven by waste-reduction mandates and polymerization chemicals purity requirements

• By Concentration

- The 80–100% grade held 55.20% share of the Hydrazine Hydrate Market in 2025, serving as the dominant feedstock for chemical blowing agents and water treatment chemicals

- The 100% Anhydrous segment is projected to record the highest CAGR at 7.92% between 2026 and 2035

• By Application

- Polymerization and Blowing Agents captured 44.80% revenue share, reflecting robust demand for specialty chemical compounds in polymer foam manufacturing

- The "Other Applications" category—including rocket propellants and direct hydrazine fuel cells—projects the fastest 8.25% CAGR to 2035

• By Region

- Asia-Pacific retained 56.10% of the Hydrazine Hydrate Market in 2025

- North America is forecast to grow at 6.48% CAGR, propelled by defense procurement of industrial reducing agents

Market Size and Forecast (2021–2035)

The estimates below integrate bottom-up production data from 14 national chemical associations, customs trade databases, and top-down validation against plant-capacity announcements filed with environmental regulators. Historical figures (2021–2024) reflect actual shipment records; the 2025 base year combines preliminary trade data with producer-reported inventory positions. Forecast values (2026–2035) apply MRFR's proprietary demand-modeling framework, incorporating feedstock price trajectories, regulatory phase-in schedules, and announced capacity additions.