India Carbon Black Market Summary

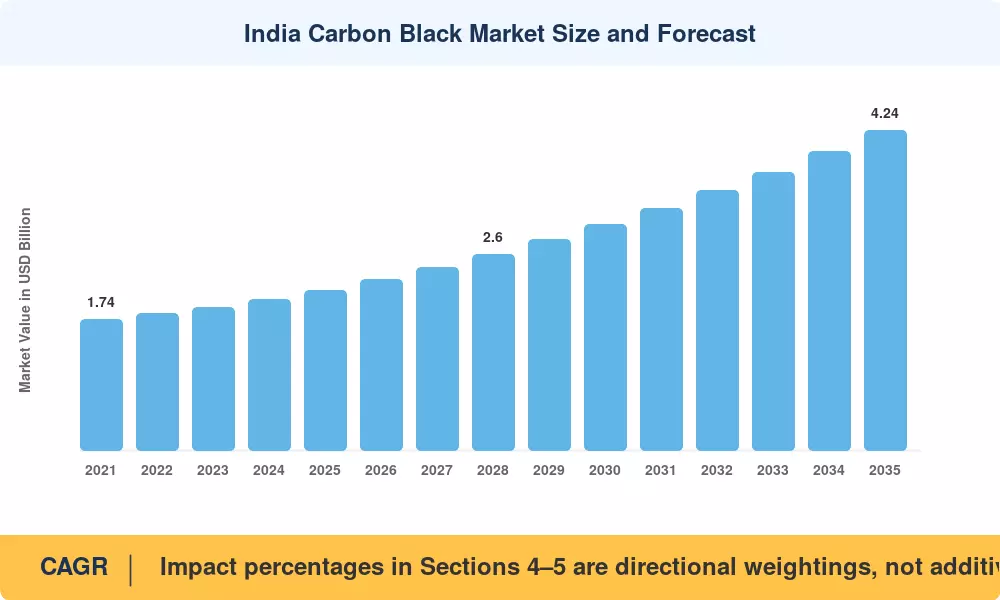

The India Carbon Black Market reached USD 2.12 Billion in 2025, and Market Research Future projects the India Carbon Black Market to grow from USD 2.26 Billion in 2026 to USD 4.24 Billion by 2035, registering a CAGR of 7.25% across the forecast window. India's Production-Linked Incentive (PLI) scheme for specialty chemicals — allocating over INR 10,000 crore through 2028 — alongside the National Infrastructure Pipeline's USD 1.4 trillion spending mandate, underpins robust demand for reinforcement-grade and pigment-grade carbon blacks [1][2].

A structural shift is reshaping the India Carbon Black Market as radial tire penetration climbs past 85% of replacement demand and original equipment manufacturers pivot toward high-structure grades that deliver lower rolling resistance. At the same time, the government's Advanced Chemistry Cell (ACC) battery program, targeting 50 GWh of domestic cell capacity by 2030, is creating a fresh demand vector for conductive-grade material in lithium-ion electrode formulations [3]. Legacy oil-furnace reactor lines are being upgraded with waste-heat co-generation and tail-gas boilers, cutting specific energy consumption by 12–18% per tonne [4].

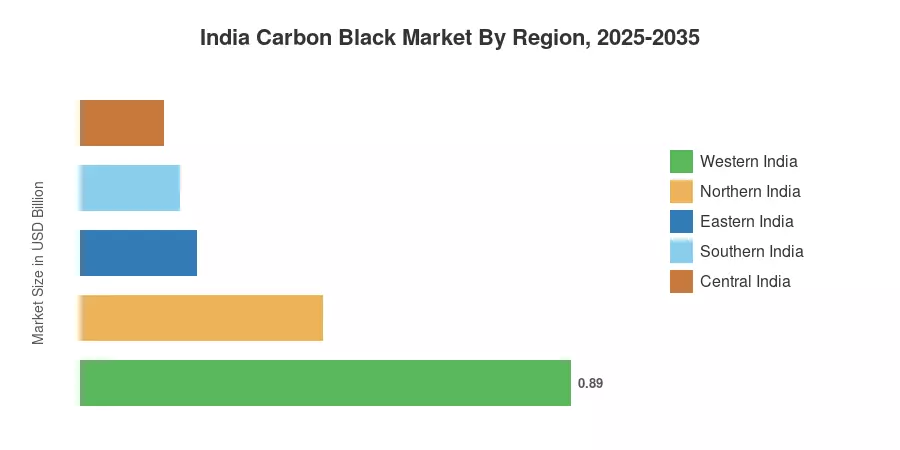

Western India commands roughly 42% of market value, driven by Gujarat's integrated petroleum-coke corridor and Maharashtra's auto-component cluster. Southern India is the fastest-growing region, propelled by Tamil Nadu's expanding tire manufacturing base and Karnataka's battery assembly investments. The India Carbon Black Market is positioned to benefit from import-substitution trends as domestic producers add over 350,000 MTPA of incremental capacity between 2026 and 2030 [5].

Key Report Takeaways

• By Process Type

- Furnace black accounted for approximately 74.9% of India Carbon Black Market revenue in 2025, reflecting its dominance in tire and rubber applications.

- Gas black is projected to register a CAGR of 8.75% through 2035, fueled by rising demand in pigment and coating end-uses.

- Thermal black remains a niche segment valued at an estimated USD 0.06 Billion in 2025.

• By Application

- Tire and industrial rubber products captured 67.5% of the India Carbon Black Market in 2025, anchored by India's status as the world's third-largest tire producer.

- Plastic compounds are poised to expand at an 8.20% CAGR to 2035, driven by UV-stable masterbatch requirements in infrastructure piping.

• By Region

- Western India holds the largest share of the India Carbon Black Market, exceeding 42%.

- Southern India is expanding fastest at an estimated CAGR of 8.4%, underpinned by automotive and electronics clusters.

Market Size and Forecast (2021–2035)

Market Research Future's estimates blend proprietary primary research — including interviews with plant-level procurement heads, feedstock traders, and downstream OEM buyers — with secondary validation from government production statistics, trade data, and corporate filings. Historical figures (2021–2024) reflect audited industry data, while forecast values (2026–2035) incorporate capacity-addition announcements and regulatory policy trajectories.