Industrial Alcohol Market Summary

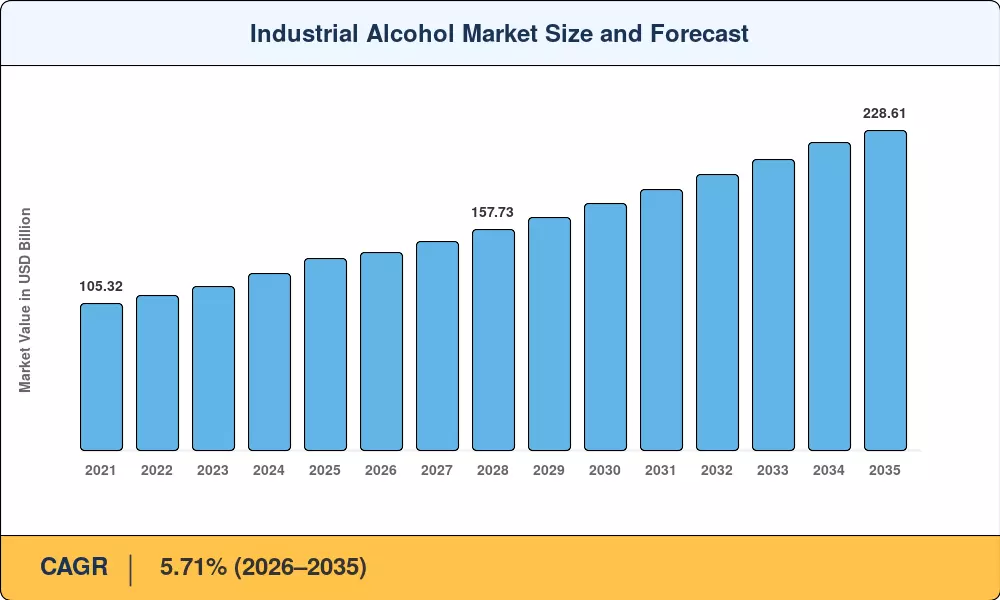

The Industrial Alcohol Market stood at USD 137.28 billion in 2025 and is projected to reach USD 141.15 billion in 2026 before climbing to USD 228.61 billion by 2035, registering a CAGR of 5.71% across the forecast period (2026–2035). Two structural forces are converging to power this trajectory: tightening low-carbon fuel standards across the Americas and the European Union's revised Renewable Energy Directive (RED III), which mandates a 42.5% renewable share in transport energy by 2030 [2]. The US 45Z Clean Fuel Production Tax Credit, worth up to USD 1.00 per gallon for qualifying ethanol production facilities, is accelerating capacity investments among producers capable of driving life-cycle emissions below 50 g CO₂e/MJ [3].

A pronounced shift in feedstock processing technology is reshaping the Industrial Alcohol Market. Legacy dry-mill ethanol production plants are being retrofitted with carbon-capture units and corn-kernel fiber cellulosic bolt-on systems, unlocking higher-value co-products and additional D3 RIN credits worth approximately USD 2.50–3.00 per gallon [4]. Brazil's RenovaBio program has channeled over USD 4.8 billion into sugarcane-based bioethanol chemicals expansion since 2020, positioning the country as the world's lowest-cost fermentation alcohol products hub [5]. Pharmaceutical alcohol purity standards are simultaneously tightening under ICH Q3D guidelines, creating a premium-pricing corridor for chemical grade alcohol suppliers.

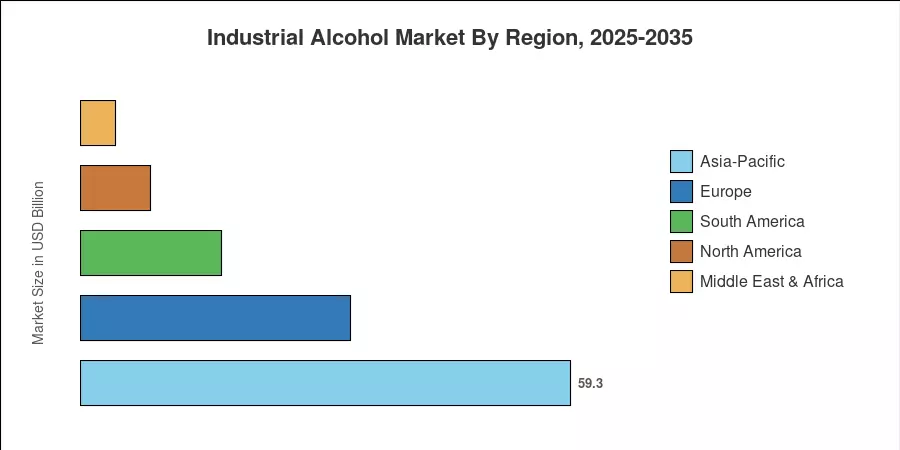

Asia-Pacific commands the largest share of the Industrial Alcohol Market at approximately 43.2% of 2025 revenue, driven by India's molasses-based industrial ethanol market and China's corn-to-ethanol buildout North America is the fastest-growing region, posting a projected CAGR of 6.14%, propelled by fuel ethanol blending mandates and expanding denatured alcohol demand in hand-hygiene applications Europe holds the second-largest position at roughly 23.8% share, anchored by German chemical grade alcohol production and France's advanced bioethanol chemicals capacity. The decade ahead will be defined by feedstock diversification, carbon-intensity scoring, and the convergence of industrial solvents with green-chemistry platforms.

Key Report Takeaways

• By Type

- Ethyl alcohol accounted for a 5.89% CAGR through 2035, reflecting surging demand for fuel ethanol blending and pharmaceutical alcohol across regulated economies

- Isopropyl alcohol is projected to reach USD 28.4 billion by 2035, underpinned by its role as a high-purity industrial solvent in semiconductor fabrication

• By Source

- Sugar and molasses feedstocks captured 39.6% of the Industrial Alcohol Market in 2025, led by Brazil and India's established fermentation alcohol products infrastructure

- Grains are forecast to register a 6.53% CAGR through 2035, driven by US corn-based ethanol production expansion

• By Application

- The fuel and energy segment dominated with USD 56.7 billion in 2025, supported by national blending mandates and carbon-capture credit economics

- Cosmetics and personal care applications are poised for a 7.24% CAGR, the fastest among application segments, as bio-based preservatives displace synthetic alternatives

• By Geography

- Asia-Pacific contributed 43.2% of the 2025 Industrial Alcohol Market, with China and India accounting for the bulk of fermentation alcohol products output

- North America is on track for the quickest regional growth at a 6.14% CAGR, boosted by the 45Z tax credit and expanding denatured alcohol applications

Industrial Alcohol Market Size and Forecast (2021–2035)

MRFR's market sizing integrates a bottom-up production-capacity model with top-down trade-flow analysis. Historical figures (2021–2024) draw on national alcohol excise records, customs data, and audited producer financials. Forecast-period estimates (2026–2035) incorporate regulatory-pipeline modeling, feedstock-cost projections, and demand elasticity curves calibrated against ethanol production capacity announcements through Q1 2026[6].