Sugar Alcohols Market Summary

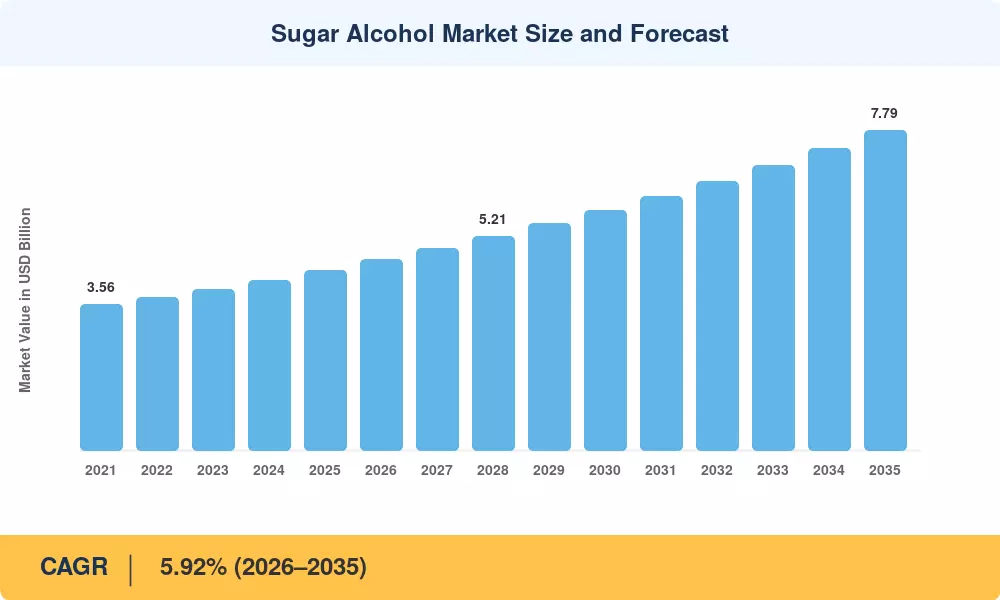

The Sugar Alcohol Market reached a valuation of USD 4.38 billion in 2025 and is projected to grow from USD 4.64 billion in 2026 to USD 7.79 billion by 2035, registering a CAGR of 5.92% during the forecast period. Rising diabetes prevalence — affecting over 537 million adults globally according to the International Diabetes Federation [1] — has propelled demand for polyol-based sweeteners in reformulated food products. Parallel regulatory pressure, including the WHO's 2024 guidelines recommending reduced free sugar intake below 5% of total energy, has given sugar alcohols a renewed policy tailwind across packaged food categories [2].

A major change is occurring in the way sugar alcohols are produced. Conventional hydrogenation-based synthesis from maize starch and wheat is gradually being substituted by fermentation-derived technologies, in particular for erythritol and xylitol. Funding from the European Commission’s Horizon Europe cluster on sustainable food ingredients with EUR 140 million has been focused on the manufacturing of bio-based polyol, hastening the transition away from petrochemical-adjacent feedstocks [3]. Since 2023, Chinese companies have together invested more than USD 200 million in new fermentation capacity [4].

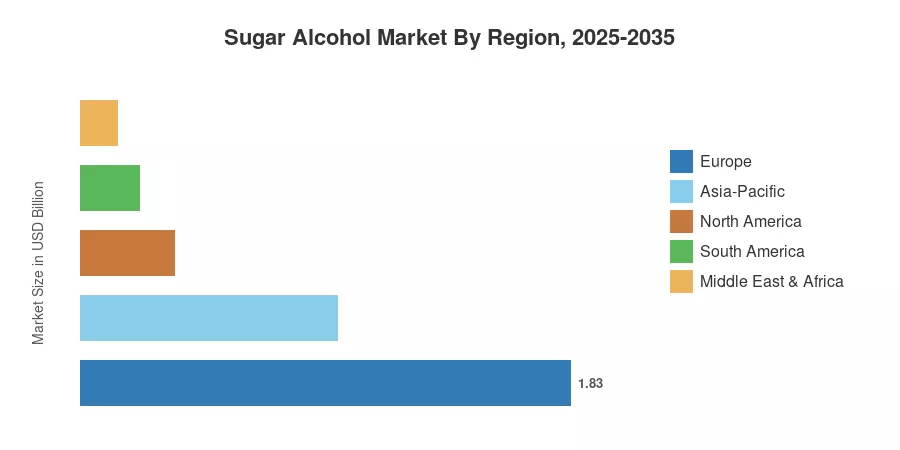

Europe leads the Sugar Alcohol Market with around 41.7% of the share, due to tight EU sugar reduction goals and strong oral-care traditions in the Nordic region. The North America region is expected to register the highest growth rate with a CAGR of 7.95%, owing to the adoption of keto-friendly sweeteners and aggressive clean-label reformulation by key CPG businesses. Asia-Pacific is the second largest market, with about 22% global market share. China is the largest producer and user. The Sugar Alcohol Market is set for continued, broad-based expansion through 2035 as regulatory environments tighten and consumer awareness grows.

Key Report Takeaways

• By Type

- Sorbitol accounted for approximately 39% of the Sugar Alcohol Market in 2025, supported by its cost-effectiveness and versatility in confectionery and pharmaceutical tableting.

- Erythritol is forecast to expand at the fastest pace through 2035, driven by zero-calorie positioning and clean-label demand.

• By Form

- Powder form represented roughly 67.5% of the global Sugar Alcohol Market revenue in 2025, preferred for dry-mix applications and direct compression tableting.

- Liquid form is projected to record a 6.45% CAGR as beverage and personal-care formulators seek ready-to-use solutions.

• By Application

- Food and beverage captured approximately 58% of the Sugar Alcohol Market in 2025, reflecting widespread adoption in sugar-free confectionery, baked goods, and dairy.

- Personal care and cosmetics applications are expected to advance at an 8.55% CAGR through 2035, led by humectant and moisturizer formulations.

• By Geography

- Europe held the largest regional share at 41.7% in the Sugar Alcohol Market in 2025, underpinned by EU regulation on front-of-pack nutrition labeling.

- North America is forecast to grow fastest at 7.95% CAGR through 2035

Sugar Alcohol Market Size and Forecast (2021–2035)

The market sizing is done by a hybrid bottom-up and top-down approach using trade data, producer shipment numbers, end-use consumption surveys and proprietary interviews with formulators across food, pharmaceutical and personal care sectors. The historical years (2021-2024) are actual trade performance, 2025 is the base year validated, and the forecasts for 2026-2035 use the calibrated CAGR adjusted for expected regulatory and demand inflections.

.webp?v=1783952215)