Industrial Coatings Market Summary

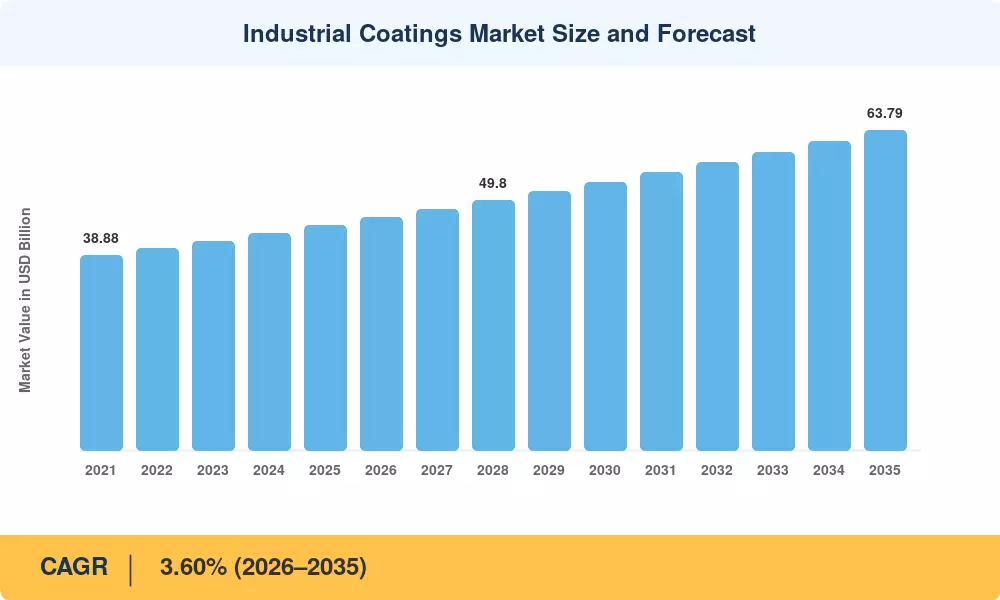

The Industrial Coatings Market was valued at USD 44.89 billion in 2025 and is projected to reach USD 46.40 billion in 2026 before climbing to USD 63.79 billion by 2035, registering a CAGR of 3.60% during the forecast period. Tightening volatile-organic-compound (VOC) regulations across North America and Europe—anchored by the U.S. EPA's 2024 National Emission Standards update and the EU Industrial Emissions Directive revisions—are pushing end users toward compliant protective coating materials, accelerating reformulation budgets across the supply chain [2][3].

A fundamental shift in coating technology is reshaping how manufacturers protect industrial assets. Solvent-borne systems, long the default for heavy duty coatings, are ceding ground to water-borne, powder, and UV-cured alternatives that cut emissions by 60–80%. Global capital expenditure on powder coating materials lines exceeded USD 2.1 billion in 2024, driven by appliance OEMs and automotive wheel producers seeking near-zero-waste finishing [4]. Meanwhile, UV-LED curing installations in composite and automotive plants have doubled since 2022, lowering energy consumption by roughly 70% per line [5].

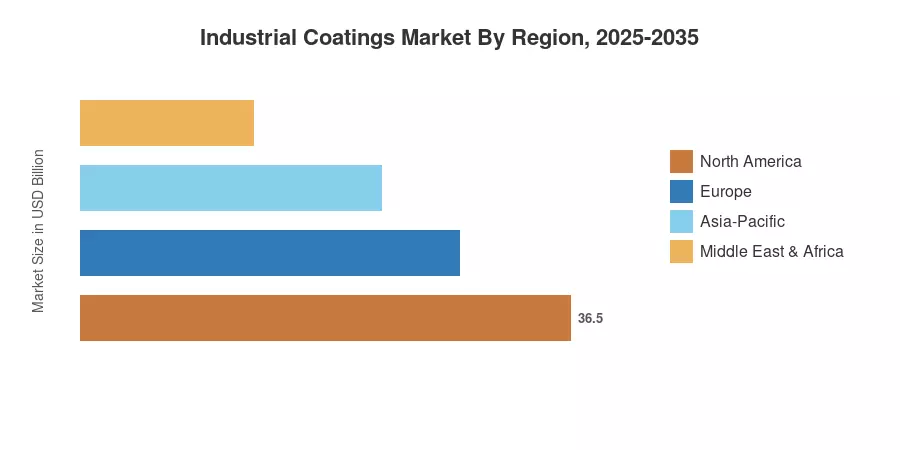

Asia-Pacific commands approximately 54.7% of the Industrial Coatings Market, supported by massive infrastructure spending in China and India. The region is also the fastest-growing, posting a projected CAGR of 4.70% through 2035 as bridge rehabilitation and petrochemical tank construction programs expand. North America holds the second-largest share at around 20.5%, anchored by corrosion resistant coatings demand in oil-and-gas pipeline maintenance and aerospace MRO. Europe follows closely, where sustainability mandates continue to channel investment into epoxy industrial coatings and water-borne reformulations.

Key Report Takeaways

• By Resin Type

- Epoxy resins captured an estimated 33.0% share of the Industrial Coatings Market in 2025, driven by their superior adhesion in metal protective coatings applications.

- Polyurethane systems are forecast to expand at a 5.50% CAGR through 2035, as aerospace and wind-energy sectors demand tougher, UV-stable surface protection coatings.

• By Technology

- Solvent-borne products accounted for roughly 39.5% of the Industrial Coatings Market revenue in 2025, though their share is declining year over year.

- Water-borne coatings are registering the fastest adoption among all technologies, growing at a 5.30% CAGR as VOC compliance tightens globally.

• By End-Use Industry & Substrate

- General industrial applications represented approximately 64.3% of the Industrial Coatings Market in 2025, spanning machinery, HVAC, and heavy equipment finishing.

- Metal substrates led with about 67.0% share, while concrete substrates are projected to grow at a 4.95% CAGR through 2035.

• By Region

- Asia-Pacific dominated the Industrial Coatings Market with a 54.7% share in 2025.

- South America is emerging as a high-potential region, recording a CAGR of 3.85%, fueled by Brazilian infrastructure concessions.

Market Size and Forecast (2021–2035)

MRFR's estimates combine bottom-up revenue tracking across 12 resin families with top-down validation against chemical output indices published by the American Chemistry Council, CEFIC, and China National Chemical Information Center. Historical figures reflect actual shipment data; forecast values apply a calibrated 3.60% CAGR with year-specific adjustments for regulation-driven demand surges and raw-material cost pass-throughs[6].