Industrial Microbiology Market Summary

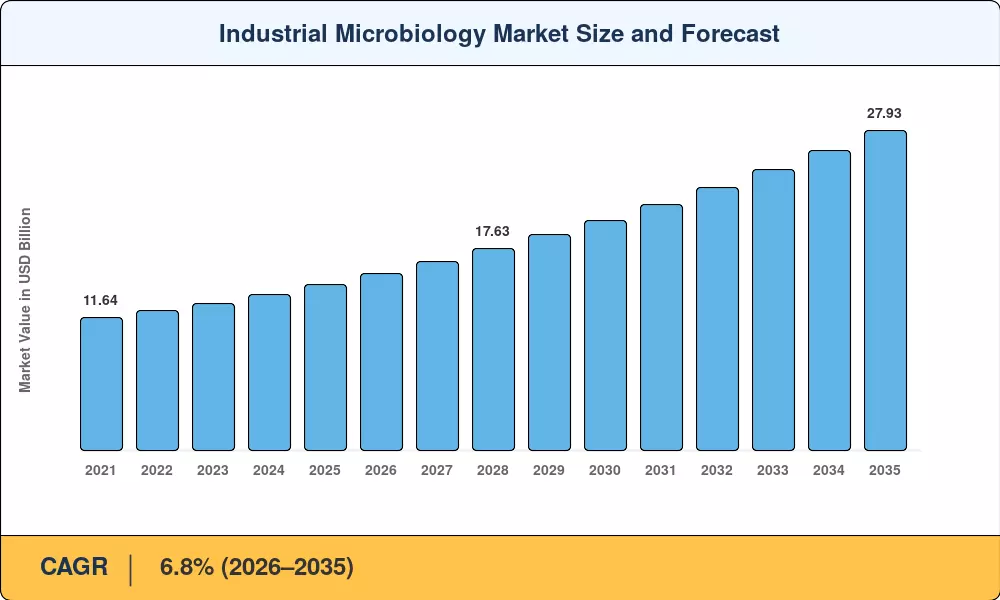

The Global Industrial Microbiology Market size was valued at USD 14.48 Billion in 2025, and the market is projected to grow from USD 15.46 Billion in 2026 to USD 27.93 Billion by 2035, registering a CAGR of 6.8% during the forecast period 2026–2035. Two converging forces are pushing this trajectory: tightening pharmaceutical sterility regulations under FDA's revised guidance on aseptic processing, and the rapid commercial scale-up of cultivated-meat production facilities that require continuous microbial monitoring infrastructure [1][2].

The industry is experiencing a decisive technology shift away from manual colony-counting methods toward automated rapid microbiology detection platforms. Legacy culture-based sterility tests requiring 14-day incubation cycles are yielding ground to ATP bioluminescence, real-time PCR, and AI-powered contamination detection systems. Global investment in bioprocessing capacity exceeded USD 28 Billion in 2024 alone, with single-use bioreactor adoption accelerating demand for compatible microbial control consumables [3][4].

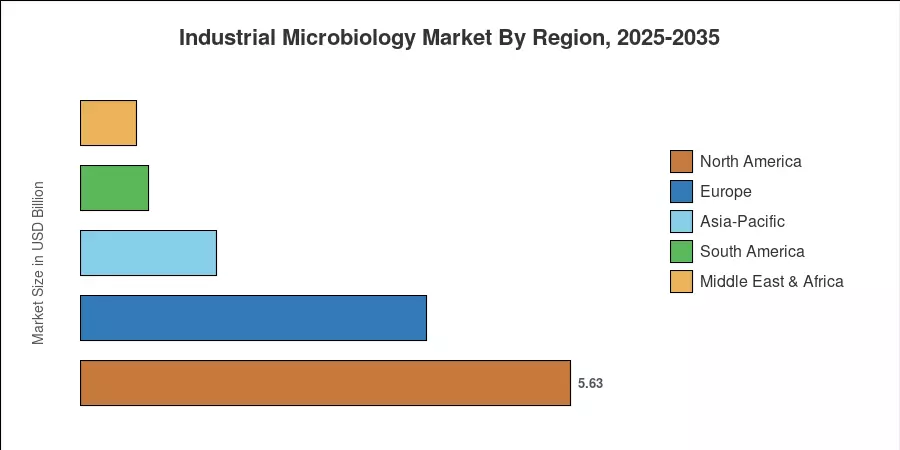

North America commands roughly 38.9% of the industrial microbiology market, anchored by the concentration of FDA-regulated pharmaceutical manufacturing. Asia-Pacific is the fastest-growing region at a 10.8% CAGR, driven by China and India's expanding biopharmaceutical sectors. Europe holds the second-largest share at approximately 27.5%, supported by the European Pharmacopoeia's harmonized testing mandates. The decade ahead will be defined by precision fermentation scale-up, ESG-linked bioremediation demand, and digital microbiology platform adoption.

Key Report Takeaways

• By Product Type

- Consumables accounted for 55.5% of the industrial microbiology market in 2025, led by media and culture preparations used in quality-control workflows.

- Reagents are forecast to expand at a 9.7% CAGR through 2035, driven by molecular-assay adoption in sterility validation.

• By Application

- Food and beverage held 34.3% of the industrial microbiology market in 2025, reflecting mandatory pathogen-screening protocols across processed-food supply chains.

- Pharmaceutical and biotechnology applications are advancing at a 10.7% CAGR to 2035.

• By Region

- North America captured 38.9% of the industrial microbiology market share in 2025, underpinned by the largest installed base of cGMP-compliant testing laboratories.

- Asia-Pacific is forecast to grow at a 10.8% CAGR through 2035.

Market Size and Forecast (2021–2035)

Market Research Future estimates are derived from a proprietary bottom-up model combining equipment shipment data, consumable procurement volumes, laboratory capacity audits, and validated forecasts from regulatory agencies and industry associations.