Rapid Microbiology Testing Market Summary

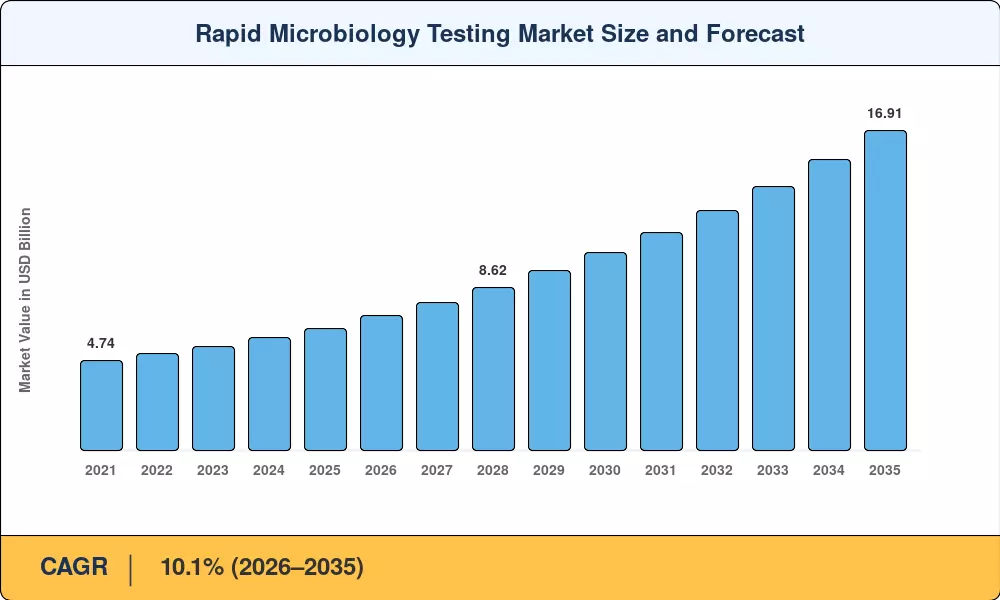

The Global Rapid Microbiology Testing Market size was valued at USD 6.46 Billion in 2025, and the market is projected to grow from USD 7.11 Billion in 2026 to USD 16.91 Billion by 2035, registering a CAGR of 10.1% during the forecast period 2026–2035. Two catalysts are driving this trajectory: an FDA reclassification of clinical mass-spectrometry systems to Class II device status in 2025, which reduced compliance costs for diagnostic labs [1], and a wave of pharmaceutical companies investing over USD 3.2 billion collectively in total laboratory automation between 2023 and 2025 [2]. The rapid microbiology testing market benefits directly from faster release-cycle mandates imposed by the WHO's revised Annex 1 guidelines for sterile manufacturing [3].

Automated platforms and molecular detection systems are gradually replacing legacy culture-based methods that necessitate 7–14 days for sterility confirmation. Automated blood-culture systems have compressed detection windows from days to hours, and MALDI-TOF mass spectrometry achieves bacterial identification accuracy exceeding 94% in under ten minutes [4]. AOAC International and AFNOR have now endorsed regulatory validation pathways that encompass over 150 rapid alternative methods, thereby enabling food manufacturers and pharmaceutical companies to replace conventional colony-count approaches with confidence [5].

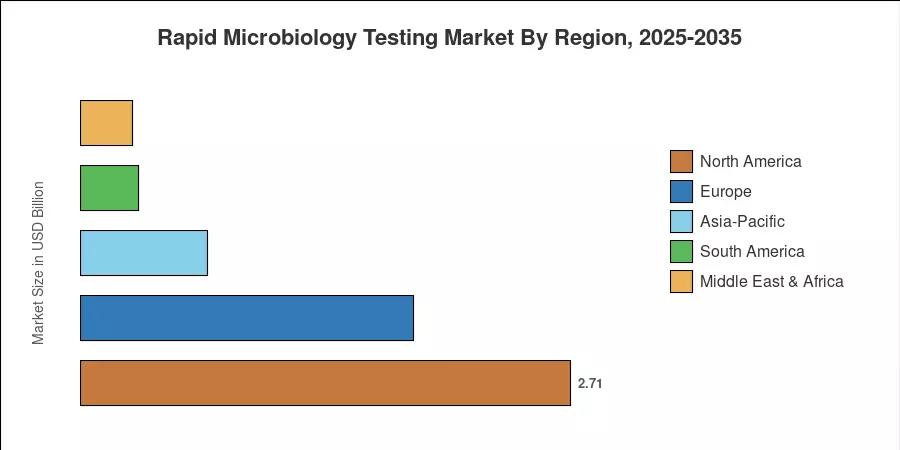

The rapid microbiology testing market is primarily dominated by North America, which is characterized by rigorous FDA and USP <71> enforcement throughout the pharmaceutical supply chain. Specifically, North America controls approximately 42.0% of the market. Propelled by India's food-safety modernization program and China's expanding biopharma sector, the Asia-Pacific region is expected to experience a 10.8% compound annual growth rate (CAGR) through 2035. Europe maintains the second-largest percentage, which is approximately 28.5%, as a result of EMA-aligned sterility testing mandates. The rapid microbiology testing market is poised to capitalize on the global expansion of personalized medicine and cell-therapy manufacturing in the coming decade by enhancing quality-control requirements.

Key Report Takeaways

• By Product Type

- Consumables captured 49.1% of the rapid microbiology testing market share in 2025, driven by recurring demand for culture media, reagent cassettes, and sample-preparation kits.

- Instruments are forecast to expand at a CAGR of 11.6% through 2035, reflecting capital investment in automated platforms and mass-spectrometry analyzers.

• By Method

- Nucleic acid-based technologies held 57.8% revenue share in 2025, underpinned by PCR and next-generation sequencing adoption across clinical and pharmaceutical labs.

- Immunological methods are projected to grow at 11.4% CAGR, supported by lateral-flow assay deployment in decentralized testing sites.

• By Application

- Clinical diagnostics represented 49.2% of the rapid microbiology testing market in 2025, led by blood-culture and respiratory-pathogen testing volumes.

- Pharmaceutical and biotech quality-control applications will register the highest CAGR of 12.9% as sterile-manufacturing oversight intensifies.

• By Geography

- North America led with 42.0% share in 2025; Asia-Pacific is on track for 10.8% CAGR to 2035.

Market Size and Forecast (2021–2035)

Market Research Future's sizing combines bottom-up revenue modelling from company filings, regulatory databases, and primary interviews with laboratory directors and procurement officers across 22 countries. Historical figures (2021–2024) are validated against disclosed revenues from publicly traded diagnostics firms, while forecast projections apply segment-weighted growth assumptions calibrated to reference benchmarks.