Industrial Valves Market Summary

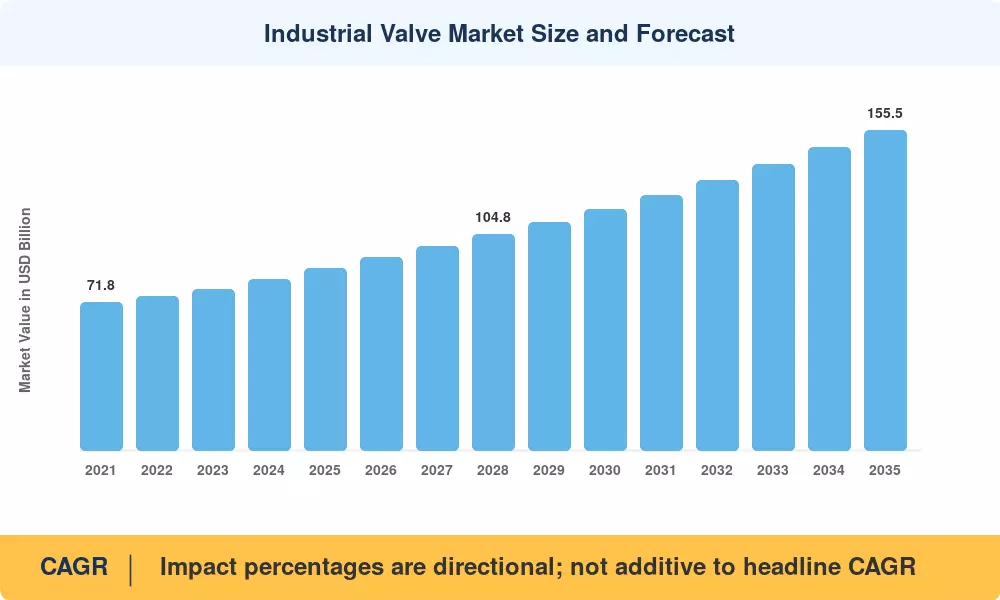

The Industrial Valve Market reached an estimated USD 88.5 billion in 2025, positioning it to grow from USD 93.6 billion in 2026 to USD 155.5 billion by 2035 at a compound annual growth rate of 5.8% during the 2026–2035 forecast window. Two catalysts anchor this trajectory: a global wave of aging infrastructure replacement — the American Society of Civil Engineers estimates USD 2.6 trillion in deferred water infrastructure investment in the U.S. alone [1] — and tightening fugitive emissions regulations across oil-producing nations that mandate upgraded sealing technologies in pipeline networks [2].

A fundamental technology shift is reshaping how valves are specified, operated, and maintained. Legacy manual actuators and analog positioners are giving way to smart valve assemblies equipped with embedded sensors, digital twins, and IIoT connectivity. The International Energy Agency projects that digitized process plants could reduce unplanned downtime by 20–30% by 2030, driving upstream and midstream operators to accelerate valve automation investments [3]. Governments in the EU and India have also introduced stricter methane abatement mandates that directly increase demand for low-emission valve designs [4].

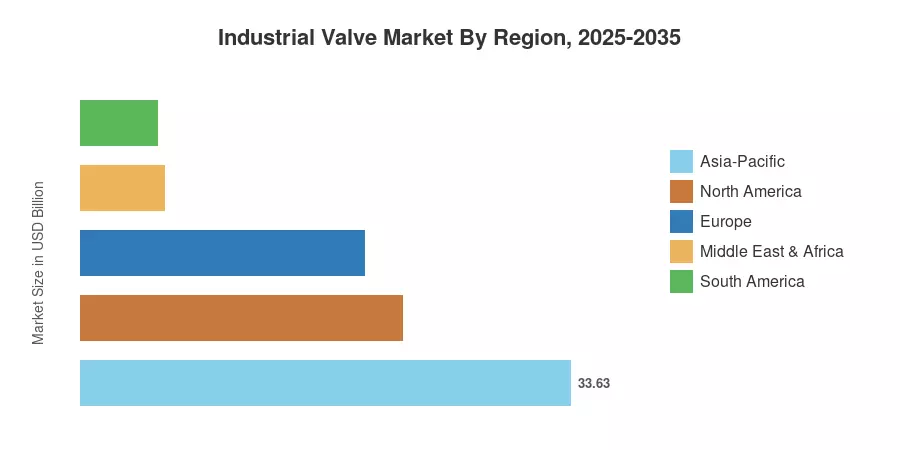

Asia-Pacific commands the largest share of the Industrial Valve Market at roughly 38% of 2025 revenue, buoyed by China's petrochemical expansion and India's Jal Jeevan Mission water infrastructure program. The region also posts the fastest forecast CAGR at approximately 7.2%. North America holds the second-largest share at 25%, driven by LNG export terminal buildouts and shale midstream investment. Europe follows at 22%, anchored by hydrogen pipeline pilot projects and decarbonization retrofits. The decade ahead will reward manufacturers who combine digital capability with regional compliance expertise.

Key Report Takeaways

• By Valve Type

- Gate valves hold the largest revenue share at approximately 28% of the Industrial Valve Market, underpinned by ubiquitous use in isolation duty across oil, gas, and water networks.

- Ball valves register the fastest segment CAGR at 6.4% through 2035, reflecting growing LNG and hydrogen applications that demand tight shut-off and quarter-turn actuation.

- Butterfly valves account for an estimated USD 15.9 billion in 2025 revenue, gaining traction in large-diameter HVAC and water treatment installations.

• By End-User Industry

- The oil and gas sector represents the single largest demand vertical in the Industrial Valve Market, contributing roughly 28% of global spend.

- Water and wastewater utilities show a projected CAGR of 6.8%, the highest among end-user verticals, as governments prioritize clean-water access.

- Power generation accounts for approximately USD 13.3 billion in 2025, with combined-cycle gas turbine plants and nuclear restarts sustaining replacement demand.

• By Region

- Asia-Pacific leads the total market value at USD 33.6 billion in 2025.

- The Middle East and Africa region posts a CAGR of 6.5%, driven by Saudi Vision 2030 megaprojects and UAE gas field expansions.

- North America captures 25% share, anchored by U.S. LNG infrastructure and Canadian oil-sands debottlenecking.

Industrial Valve Market Size and Forecast (2021–2035)

Market sizing draws on a triangulated methodology that cross-references manufacturer revenue disclosures, trade-association shipment data (Valve Manufacturers Association of America, European Industrial Valve Manufacturers' Association), customs databases, and downstream capex budgets from publicly listed end users. Historical figures reflect actuals; forecast values apply a base CAGR adjusted for cyclical capex patterns in oil and gas, water infrastructure stimulus programs, and energy-transition policy timelines [5][6].