Influenza Diagnostics Market Summary

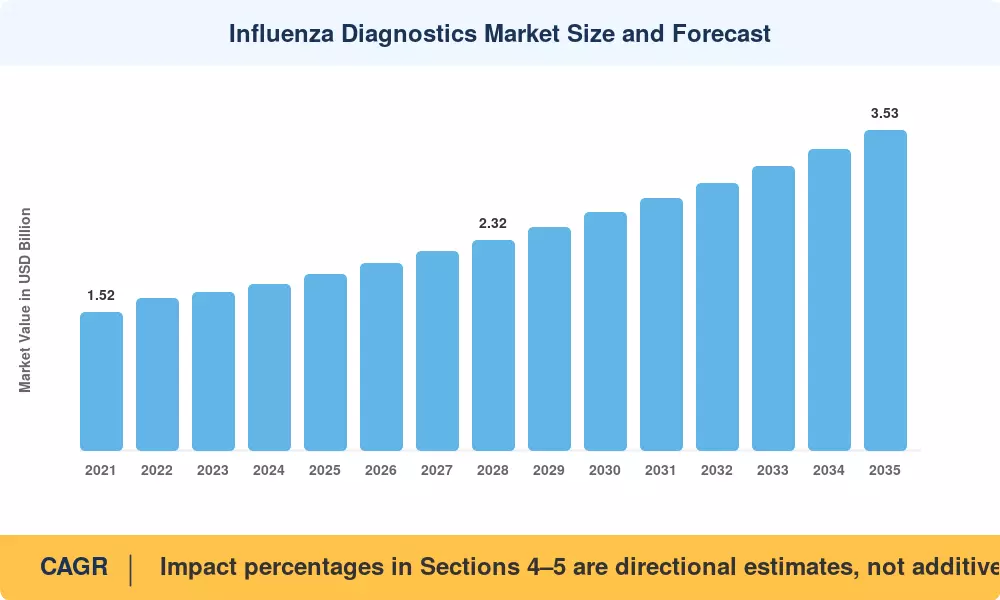

The Global Influenza Diagnostics Market size was valued at USD 1.94 Billion in 2025, and the market is projected to grow from USD 2.06 Billion in 2026 to USD 3.53 Billion by 2035, registering a CAGR of 6.15% during the forecast period 2026–2035. This expansion reflects a structural shift in global healthcare spending toward routine respiratory surveillance, catalyzed by post-pandemic investments in pathogen preparedness. Governments across more than 40 countries have committed incremental funding to sentinel surveillance networks, with the U.S. CDC alone allocating over USD 900 million annually for influenza monitoring and vaccine strain selection [1].

Technology is the accelerant. The gold standard used to be the legacy culture-based approaches, and now molecular platforms are replacing them, which may get you an answer in less than 60 minutes. RT-PCR platforms, loop-mediated isothermal amplification (LAMP) devices, and CRISPR-based assays are displacing slower workflows and cutting hospital turnaround times by 40–60% [2]. At the same time, AI-enhanced quality control software is enabling labs to handle more samples without a commensurate increase in personnel, a key benefit as clinical labor shortages continue around the world [3].

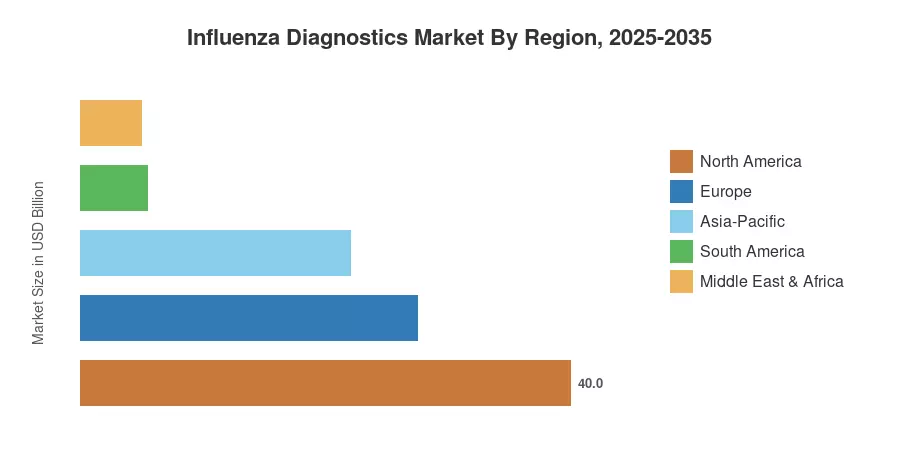

North America has around 40.0% of the Influenza Diagnostics Market due to a large installed base and a conducive reimbursement scenario. The Asia-Pacific region is the fastest-developing region with a CAGR of 8.40% through 2035. China, India and ASEAN countries are building laboratory infrastructure. Europe comes second with 27.5% through the EU’s integrated Epidemic Intelligence system and harmonized IVD regulation [4]. As co-circulation of influenza with other respiratory viruses becomes an annual planning assumption, diagnostic demand will stay structurally elevated through 2035.

Key Report Takeaways

• By Test Type

- Rapid Influenza Diagnostic Tests captured 44.0% of the Influenza Diagnostics Market share in 2025, remaining the highest-volume test category despite lower sensitivity than molecular alternatives.

- CRISPR-based assays are projected to grow at a 10.0% CAGR through 2035, the fastest among all test type sub-segments.

- RT-PCR platforms accounted for USD 0.54 billion in 2025 revenue, underpinned by hospital laboratory procurement cycles.

• By End User

- Hospitals and Clinical Laboratories held 45.0% of the Influenza Diagnostics Market in 2025, reflecting centralized testing workflows.

- Point-of-care settings are forecast to expand at a 9.85% CAGR to 2035, supported by decentralized care models.

• By Geography

- North America commanded 40.0% of revenue in 2025, led by U.S. reimbursement clarity and laboratory density.

- Asia-Pacific is anticipated to grow at an 8.40% CAGR to 2035, the fastest among all regions.

Influenza Diagnostics Market Size and Forecast (2021–2035)

Market Research Future (MRFR) follows a triangulated approach that includes initial interviews with hospital procurement officers and laboratory directors, secondary research of IVD regulatory submissions, and proprietary demand modeling based on seasonal influenza monitoring data. Historical data are derived from actual diagnostic volumes scaled for average selling price deflation, and forecast estimates include pipeline product launches and announced reimbursement policy changes through Q1 2025.