Insulin Delivery Devices Market Summary

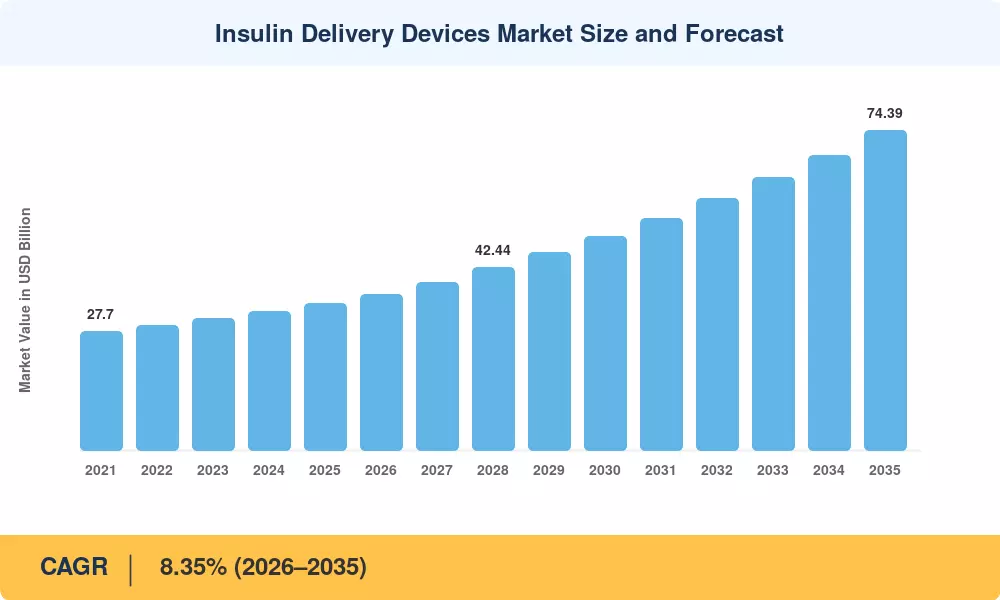

The Insulin Delivery Devices Market size was valued at USD 34.15 Billion in 2025, and the market is projected to grow from USD 36.15 Billion in 2026 to USD 74.39 Billion by 2035, registering a CAGR of 8.35% during the forecast period 2026–2035. Rising diabetes prevalence — the IDF estimates 643 million adults globally living with diabetes by 2030 — has intensified demand for precision dosing hardware [1]. National reimbursement expansions in China's NRDL and India's Ayushman Bharat program have unlocked high-volume, price-sensitive segments that previously relied on vial-and-syringe routines [2].

A significant technology shift is taking place in the Insulin Delivery Devices Market. Legacy manual injection methods are being replaced by algorithm-driven, Bluetooth-enabled platforms that send glucose and dosage data in real time. The US FDA approved three hybrid automated delivery systems between 2023 and 2025. In January 2025, CMS increased Medicare Part D coverage to include wearable patch devices, a policy change anticipated to bring 1.2 million new device users by 2028 [3]. The timescales for European MDR (EU 2017/745) compliance are also driving manufacturers toward digitally certified, cybersecure infrastructures [4].

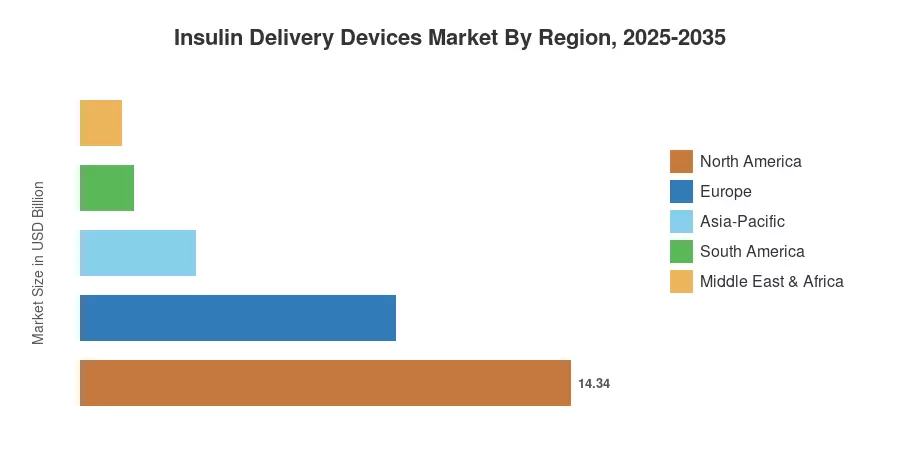

North America had around 42% share of the Insulin Delivery Devices Market in 2025 due to strong private payer coverage and high per-capita insulin expenditure. Asia-Pacific is the fastest expanding market with an anticipated CAGR of 9.9%, led by government procurement initiatives and the rise of indigenous low-cost wearable gadgets at around half the cost of Western equivalents. Europe is the second-highest geographical market at approximately 27% and is driven by NHS and statutory health insurance formulary listings in Germany, France, and the UK.

Key Report Takeaways

• By Product Type

- Pen-based devices held the leading position in the Insulin Delivery Devices Market in 2025 with approximately 48% revenue share, reflecting established prescriber habits and broad retail availability.

- Pump platforms are forecast to expand at a CAGR of 12.4% through 2035, driven by automated dosing algorithms and pediatric adoption.

• By Technology / Connectivity

- Non-connected hardware accounted for around 66% of the Insulin Delivery Devices Market revenue in 2025.

- Connected platforms are projected to grow at a 13.8% CAGR through 2035 as payers incentivize real-time data sharing.

• By Geography

- North America dominated the Insulin Delivery Devices Market, contributing approximately USD 14.34 billion in 2025.

- Asia-Pacific is advancing at the highest regional CAGR of 9.9%, with China and India together expected to surpass USD 18 billion by 2035.

Insulin Delivery Devices Market Size and Forecast (2021–2035)

Market Research Future (MRFR) forecasts are based on corporate financials, regulatory filings, import export databases and proprietary primary research across 18 countries. Historical figures (2021-2024) are based on audited results; the 2025 base year is a combination of actuals (Q3 2025) and full-year estimates; and the 2026-2035 forecast is based on growth models at the segment level, calibrated to diabetes epidemiology, reimbursement dynamics and competition pipeline timelines.