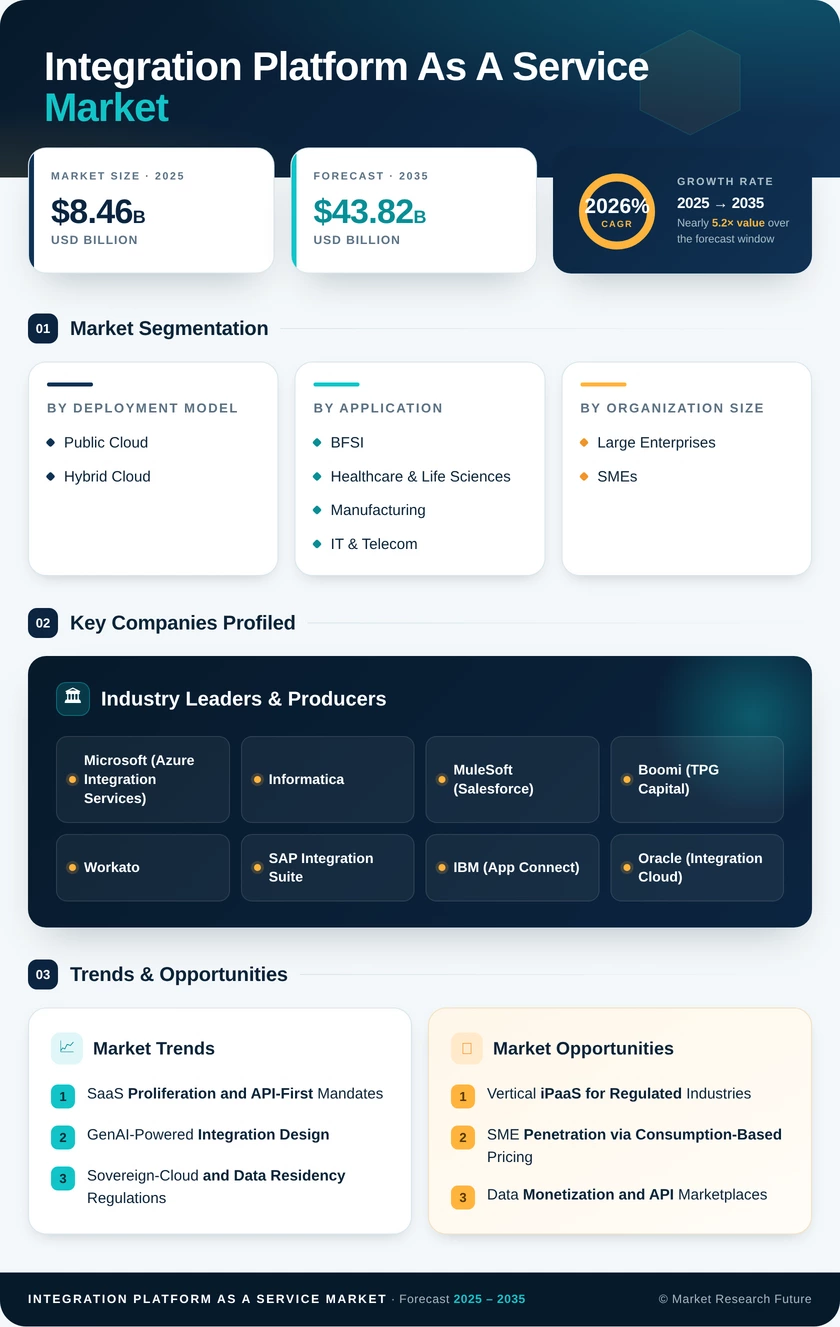

Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

| Deployment Model | Public Cloud, Hybrid Cloud | Public Cloud | Hybrid Cloud |

| End-User Vertical | BFSI, Healthcare & Integration Platform as a Service Market, Manufacturing, IT & Telecom, Retail & E-Commerce, Government & Public Sector, Others | BFSI | Healthcare & Integration Platform as a Service Market |

| Organization Size | Large Enterprises, Small and Mid-Size Enterprises (SMEs) | Large Enterprises | SMEs |

| Integration Platform as a Service Market Type | Application Integration, Data / ETL Integration, API & Event Integration, B2B / EDI Integration, Others | Application Integration | API & Event Integration |

| Geography | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America | Asia-Pacific |

Market Segmentation Overview

By Deployment Model

| Sub-Segment | Key Trend |

| Public Cloud | Dominant deployment mode driven by SaaS-native workloads and consumption-based pricing models |

| Hybrid Cloud | Fastest-growing mode as data residency regulations push sensitive workloads to on-premises or sovereign-cloud environments |

Public Cloud accounts for the majority of iPaaS deployments because enterprises prefer the scalability and OpEx economics of cloud-native integration platforms. Hybrid Cloud adoption is accelerating as sovereign-cloud mandates and latency-sensitive edge use cases require split-workload architectures.

By End-User Vertical

| Sub-Segment | Key Trend |

| BFSI | Open-banking mandates and real-time payment orchestration drive the largest share of platform spending |

| Healthcare & Integration Platform as a Service Market | HL7 FHIR interoperability requirements create compliance-driven adoption cycles |

| Manufacturing | Industry 4.0 and OT-IT convergence demand shop-floor-to-cloud integration fabrics |

| IT & Telecom | 5G network slicing and OSS/BSS modernization fuel API-centric integration needs |

| Retail & E-Commerce | Omnichannel order management and marketplace API connectivity drive mid-market adoption |

| Government & Public Sector | Cross-agency data exchange mandates and e-government portals require secure integration platforms |

| Others | Education, energy, logistics, and media verticals with emerging integration needs |

BFSI leads vertical spending because financial institutions operate among the most complex SaaS and legacy application estates. Healthcare & Integration Platform as a Service Market is compounding fastest as FHIR-based interoperability mandates translate into multi-year platform procurement cycles.

By Organization Size

| Sub-Segment | Key Trend |

| Large Enterprises | Complex multi-cloud estates and regulatory compliance drive majority of current spend |

| Small and Mid-Size Enterprises (SMEs) | Consumption-based pricing, low-code builders, and template-driven onboarding unlock rapid adoption |

Large Enterprises dominate current revenue because they manage hundreds of applications across multiple clouds. SMEs represent the fastest-growing segment as vendors introduce freemium models and pre-built connector templates that lower the barrier to entry.

By Integration Platform as a Service Market Type

| Sub-Segment | Key Trend |

| Application Integration | SaaS-to-SaaS workflow automation remains the primary entry-point use case |

| Data / ETL Integration | Cloud data lake and warehouse population drives demand for managed ETL pipelines |

| API & Event Integration | Real-time event-driven architectures and webhook orchestration compound fastest |

| B2B / EDI Integration | Supply-chain digitization and partner onboarding sustain steady demand |

| Others | Process automation, IoT integration, and emerging integration patterns |

Application Integration holds the largest share as connecting SaaS applications remains the most common buyer motivation. API & Event Integration is the fastest-compounding service type, reflecting the industry-wide shift from batch processing to real-time, event-driven data flows.