Integration Platform as a Service (IPaaS) Market Summary

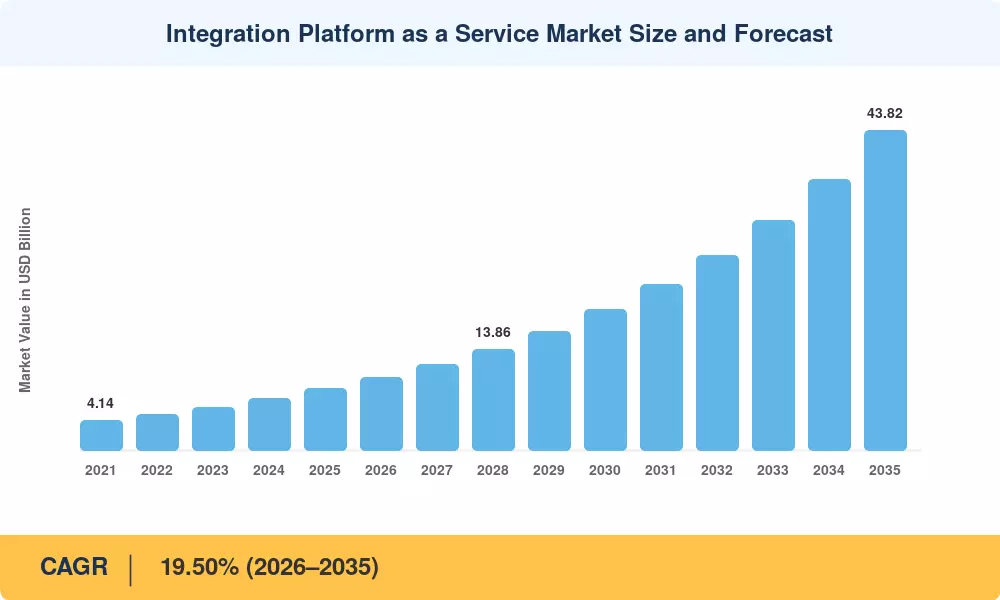

The Integration Platform as a Service Market reached an estimated USD 8.46 Billion in 2025, with the forecast period beginning at USD 10.08 Billion in 2026 and climbing to USD 43.82 Billion by 2035 at a CAGR of 19.50%. Enterprises across every vertical are under pressure to unify fragmented SaaS estates, IoT telemetry streams, and edge computing nodes — and that pressure translates into sustained platform spending. The EU's Data Act, which mandates cross-border data portability by 2027, and the US CHIPS and Science Act's downstream digital infrastructure provisions are two policy catalysts channeling investment into cloud middleware solutions and enterprise cloud connectivity [2][3].

A technology shift is accelerating the Integration Platform as a Service Market: hand-coded point-to-point links and on-premises ESBs are giving way to intelligent, policy-aware integration fabrics. GenAI-powered design assistants now auto-generate data mappings, reducing connector development time by 40–60% according to industry benchmarks [4]. Event-driven architectures built on Apache Kafka and cloud-native pub/sub services are replacing batch ETL pipelines, letting organizations process real-time data across hybrid estates. Global enterprise spending on iPaaS cloud integration surpassed USD 7.2 Billion in 2024, underscoring the momentum behind API integration platforms [5].

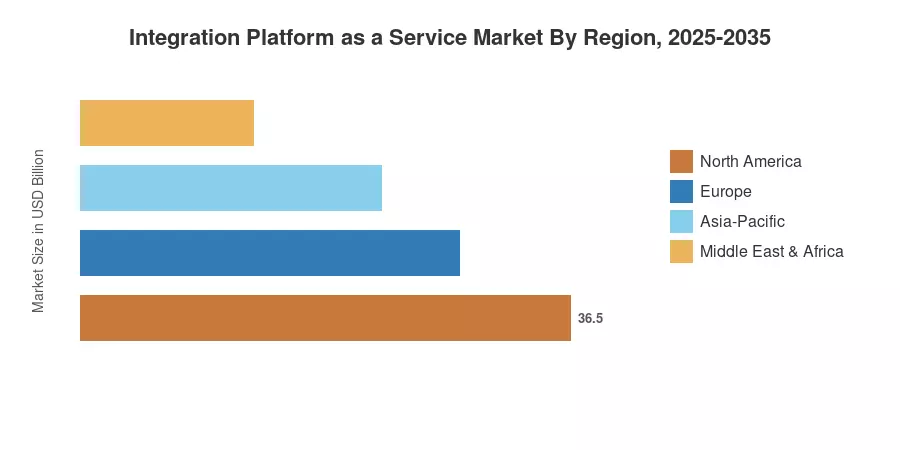

North America commanded roughly 48.70% of the Integration Platform as a Service Market in 2025, anchored by hyperscaler ecosystems and mature SaaS adoption. Asia-Pacific is the fastest-growing region at a projected 25.40% CAGR, driven by manufacturing modernization across China, India, and ASEAN economies Europe holds the second-largest share at approximately 24.10%, where sovereign-cloud mandates and GDPR-driven data residency requirements continue to fuel demand for compliant SaaS integration tools. The next decade will reward platform vendors that combine multi-cloud openness with vertical-specific compliance modules.

Key Report Takeaways

• By Deployment Model

- Public Cloud dominated the Integration Platform as a Service Market with 75.20% revenue share in 2025, reflecting enterprise preference for consumption-based cloud middleware solutions

- Hybrid Cloud deployment is forecast to compound at a 29.80% CAGR through 2035, as data residency regulations push enterprises toward split-workload architectures for enterprise cloud connectivity

• By End-User Vertical

- BFSI accounted for 23.10% of the Integration Platform as a Service Market in 2025, driven by open-banking API mandates and real-time fraud detection pipelines

- Healthcare and Life Sciences are advancing at a 32.50% CAGR, fueled by interoperability standards such as HL7 FHIR and cross-system EHR integration

• By Region

- North America led the Integration Platform as a Service Market at USD 4.12 Billion in 2025, with the US alone representing over 78% of regional revenue

- Asia-Pacific is projected to reach USD 14.35 Billion by 2035, as consumption-based pricing opens iPaaS cloud integration to SMEs across emerging economies

Market Size and Forecast (2021–2035)

MRFR's proprietary estimation framework triangulates vendor revenues, enterprise IT spending surveys, and API traffic proxy data to construct bottom-up market sizing. Historical figures (2021–2024) rely on audited annual reports and validated third-party datasets; forecast values (2026–2035) apply the calibrated 19.50% CAGR with adjustments for macroeconomic and regulatory variables.