IoT Microcontroller Market Summary

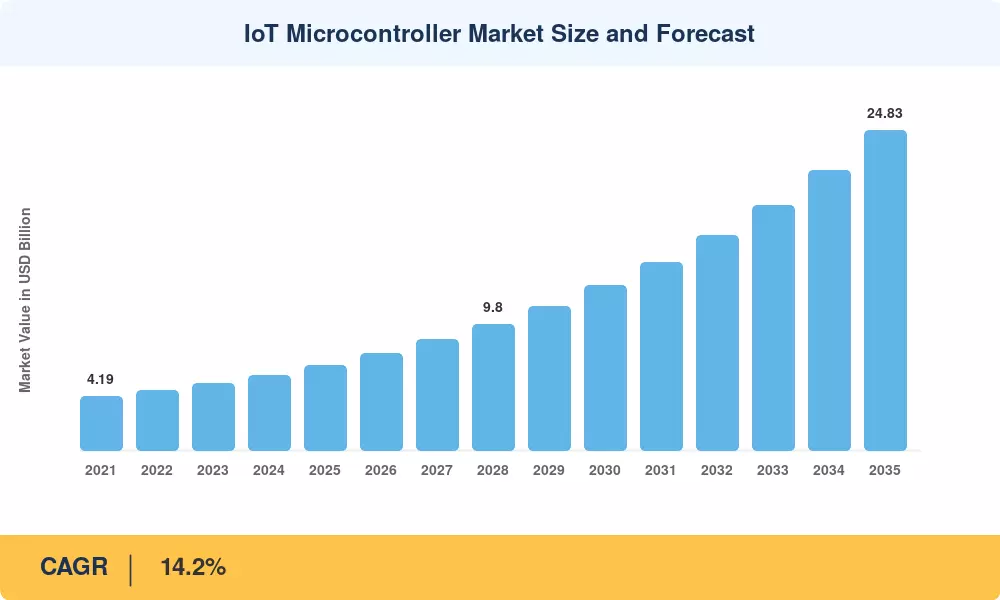

The IoT Microcontroller Market reached an estimated USD 6.58 Billion in 2025 and is projected to grow from USD 7.51 Billion in 2026 to USD 24.83 Billion by 2035, registering a CAGR of 14.2% across the forecast window. Two forces are pulling silicon vendors into high-volume production faster than anyone expected: sovereign semiconductor policies—India's USD 10 Billion India Semiconductor Mission and the U.S. CHIPS Act's USD 52.7 Billion allocation—are guaranteeing long-term wafer capacity, while enterprise budgets for edge analytics keep expanding as manufacturers demand real-time inference at the sensor node rather than the cloud [1][2].

A meaningful technology shift is under way. Legacy 8-bit controllers that dominated building-automation and appliance designs for decades are yielding ground to 32-bit and 64-bit devices capable of running on-device machine-learning models. Multi-protocol radio integration—particularly the emergence of the Matter interoperability standard—is reshaping bill-of-material decisions, steering OEMs toward controllers that manage Wi-Fi, Bluetooth LE, and Thread stacks on a single die without breaching battery budgets [3].

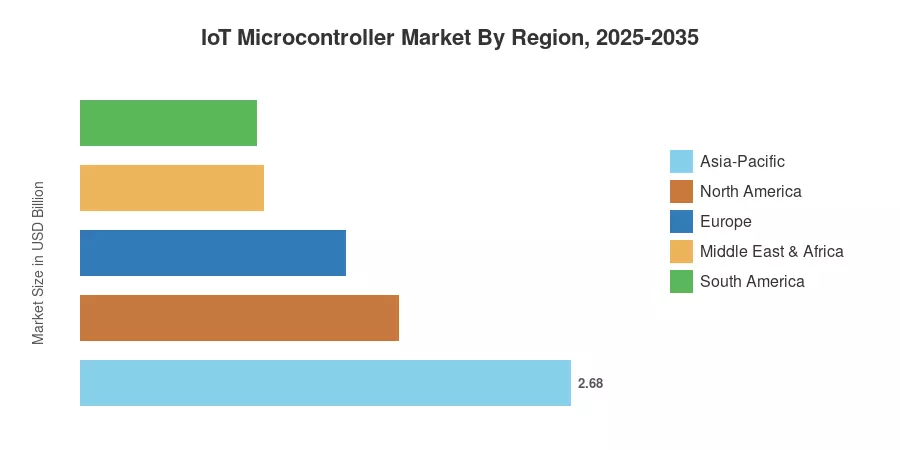

Asia-Pacific commands the largest share of the IoT Microcontroller Market at roughly 40.8% of 2025 revenue, anchored by China's consumer-electronics output and India's expanding smart-infrastructure spending. The Middle East & Africa region is the fastest-growing region at a projected 15.2% CAGR, driven by smart-city mega-projects across the Gulf Cooperation Council states. North America follows as the second-largest market, fueled by industrial-IoT modernization and connected-vehicle rollouts. The next decade will see on-device AI accelerators move from a differentiating feature to a baseline expectation across every IoT Microcontroller Market segment.

Key Report Takeaways

• By Bit Class

- 32-bit microcontrollers held approximately 54% of IoT Microcontroller Market shipments in 2025, reflecting the dominance of ARM Cortex-M architectures in mid-range embedded designs.

• By Instruction Set Architecture

- 32-bit microcontrollers held approximately 54% of IoT Microcontroller Market shipments in 2025, reflecting the dominance of ARM Cortex-M architectures in mid-range embedded designs.

- RISC-V instruction-set devices are poised to register a 17.7% CAGR through 2035, as open-source silicon gains traction among cost-sensitive Asian OEMs and European automotive Tier-1 suppliers.

• By Connectivity Type

- Wi-Fi-integrated modules accounted for roughly 35% of connectivity-type revenue in 2025, though cellular NB-IoT and LTE-M variants are growing fastest at a projected 18.0% CAGR.

• By Application

- Industrial automation and IIoT generated approximately 23% of application-segment revenue in 2025, led by programmable-logic-controller replacement cycles and predictive-maintenance deployments.

- Smart-city infrastructure is forecast to expand at a 15.3% CAGR through 2035, propelled by connected-lighting, traffic-management, and environmental-sensing mandates.

• By Region

- Asia-Pacific produced the largest regional revenue for the IoT Microcontroller Market in 2025 with a 40.8% share.

- The Middle East & Africa region is projected to be the fastest-growing region at a 15.2% CAGR over 2026–2035.

IoT Microcontroller Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing framework combines bottom-up shipment tracking across 14 product families with top-down cross-validation against publicly reported semiconductor revenues, trade-flow databases, and primary interviews with 120+ industry participants conducted between Q3 2024 and Q1 2025.