Laser Welding Machine Market Summary

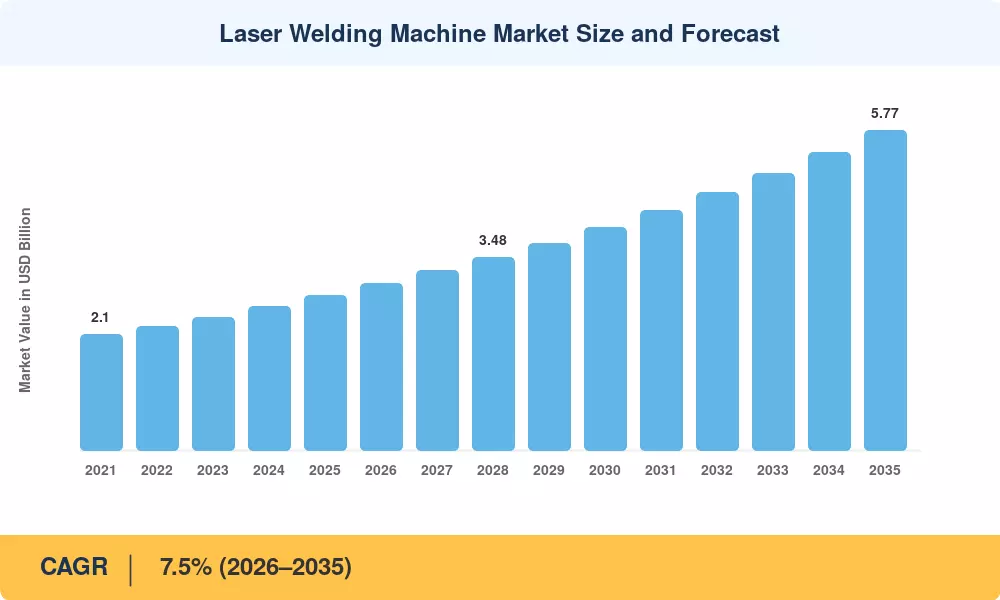

The global Laser Welding Machine Market was valued at USD 2.80 billion in 2025 and is projected to grow from USD 3.01 billion in 2026 to USD 5.77 billion by 2035, registering a CAGR of 7.5% during 2026–2035. Two catalysts stand behind this trajectory: the accelerating shift toward lightweight materials in automotive manufacturing — driven by emissions targets under the EU's Euro 7 standards and the U.S. EPA's Multi-Pollutant Emissions Standards [1] — and the electronics industry's relentless push toward miniaturized, hermetically sealed components that only non-contact joining can reliably produce.

Legacy resistance welding and TIG welding setups are yielding ground to fiber and diode laser platforms that deliver higher beam quality, lower per-watt costs, and dramatically smaller heat-affected zones. The automotive sector alone is channeling an estimated USD 12 billion globally into body-in-white laser joining lines through 2030, according to the International Energy Agency's EV industrial readiness reports [2]. Battery module assembly for electric vehicles has emerged as a particularly high-growth niche, where weld consistency directly affects cell safety and cycle life.

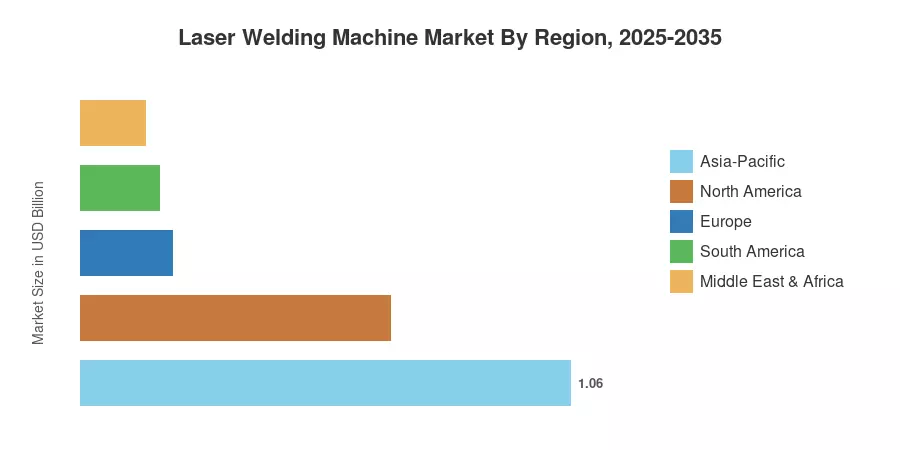

Asia-Pacific commands roughly 38% of the Laser Welding Machine Market, propelled by China's dominance in EV production and consumer electronics assembly. The region also registers the fastest CAGR at 8.8% through 2035. Europe holds the second-largest share at 28%, underpinned by Germany's advanced automotive OEMs and Tier-1 suppliers. North America contributes 24%, with aerospace and medical device manufacturing driving demand. As additive-manufacturing and digital-twin integration deepen, the Laser Welding Machine Market is positioned for sustained double-digit expansion in select verticals through the early 2030s.

Key Report Takeaways

• By Technology

- Fiber laser systems account for approximately 44% of the Laser Welding Machine Market, owing to superior wall-plug efficiency and maintenance simplicity.

- Diode laser welding platforms are growing at a CAGR of 9.2%, the fastest among technology types.

- CO₂ laser machines still hold USD 0.39 billion in annual revenue, concentrated in thick-section industrial cutting and joining.

• By Application

- Automotive and transportation represent roughly 32% of global demand within the Laser Welding Machine Market.

- Electronics and semiconductor packaging are projected to reach a CAGR of 8.6% during the forecast period.

- Medical device manufacturing contributes USD 0.34 billion, driven by Class III implantable device regulations.

• By Region

- Asia-Pacific leads with 38% revenue share, anchored by China, Japan, and South Korea.

- Europe's Laser Welding Machine Market benefits from a CAGR of 7.1%, led by Germany and France.

- The Middle East & Africa is the smallest region at roughly 5% share but shows rising adoption in the energy sector fabrication.

Laser Welding Machine Market Size and Forecast (2021–2035)

Market sizing relies on a bottom-up methodology that aggregates machine-level shipment data from OEM disclosures, customs trade databases (UN Comtrade HS 8515.80), and proprietary primary interviews with 120+ industry stakeholders across 18 countries. Top-down validation cross-references end-user capital expenditure filings and laser source supplier revenue breakdowns [3].