Life Science & Analytical Instruments Market Summary

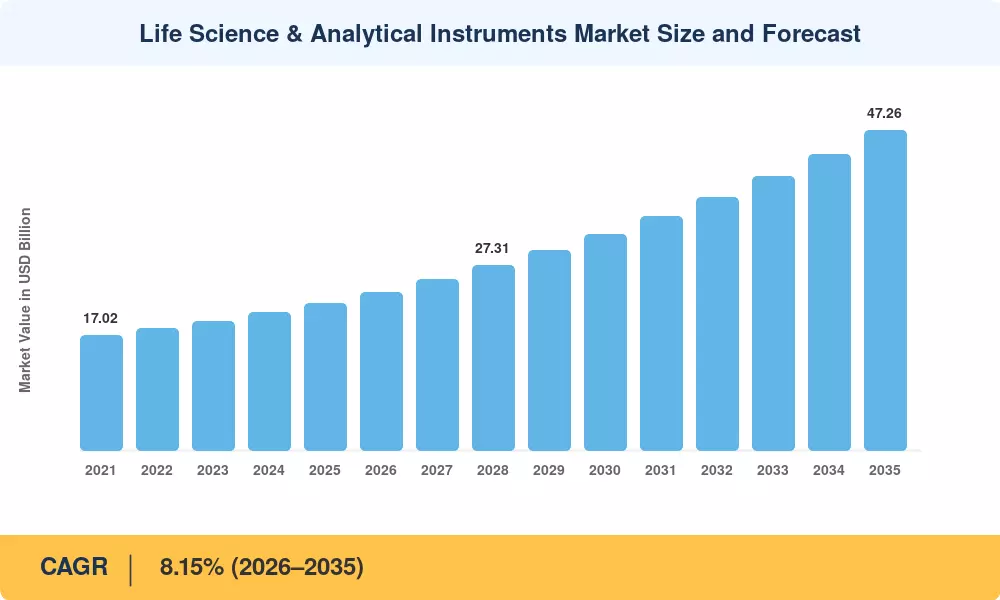

The Life Science and Analytical Instruments Market size was valued at USD 21.68 Billion in 2025, and the market is projected to grow from USD 23.35 Billion in 2026 to USD 47.26 Billion by 2035, registering a CAGR of 8.15% during the forecast period 2026–2035. Accelerating biologics pipelines — the FDA approved 17 novel biological therapies in 2024 alone — and tightening real-time process-analytical-technology (PAT) mandates under ICH Q13 have created sustained demand for high-resolution analytical platforms [1]. Global pharmaceutical R&D spending exceeded USD 265 Billion in 2024, funneling capital directly into instrument procurement cycles [2].

A pronounced technology shift is underway within the Life Science and Analytical Instruments Market. Legacy single-technique benchtop units are giving way to integrated workflow platforms that couple separation science with AI-driven data interpretation. Thermo Fisher's 2024 launch of cloud-connected Orbitrap systems illustrates the trend: instruments now stream analytical data into centralized LIMS environments, cutting method-development timelines by 30–40% according to vendor benchmarks [3]. The European Commission's Horizon Europe program allocated EUR 1.8 Billion to health-research infrastructure between 2024 and 2027, much of it earmarked for next-generation instrumentation [4].

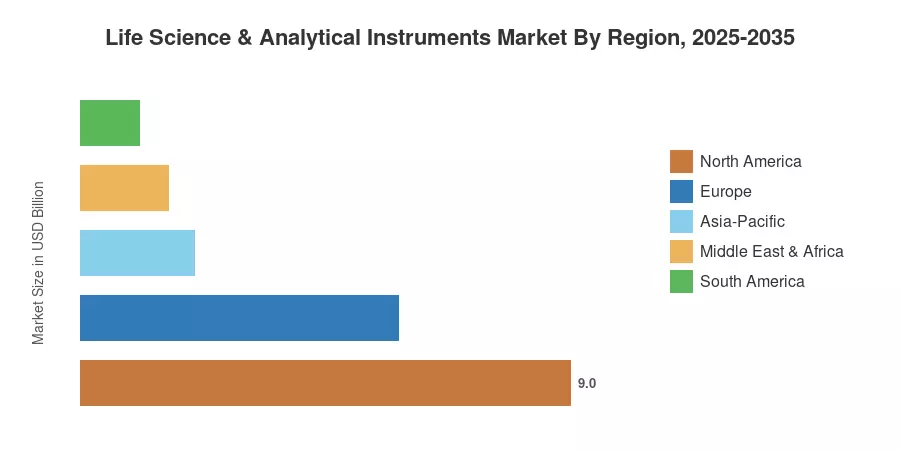

North America commands roughly 41.5% of the Life Science and Analytical Instruments Market, anchored by NIH funding that topped USD 48 Billion in fiscal year 2025 [5]. Asia-Pacific is the fastest-growing region, advancing at a 9.67% CAGR as Chinese and Indian CDMOs standardize high-throughput screening capabilities. Europe holds the second-largest share at approximately 27%, driven by Germany's BioPharma cluster and pan-EU regulatory harmonization. The convergence of precision-medicine programs and continuous-manufacturing adoption positions this market for sustained double-digit instrument refresh cycles through the early 2030s.

Key Report Takeaways

• By Product Type

- Chromatographs captured 31.2% revenue share of the Life Science and Analytical Instruments Market in 2025, underpinned by continuous-manufacturing validation requirements.

- Spectrometers are projected to record the fastest segment CAGR of 8.65% through 2035, propelled by multi-omics research expansion.

- Liquid analyzers generated approximately USD 3.14 Billion in 2025 revenue, reflecting growing inline process-control adoption.

• By End User

- The pharmaceutical vertical held 63.5% of the Life Science and Analytical Instruments Market in 2025.

- Biopharmaceutical and nutraceutical applications are expanding at a 9.35% CAGR, the fastest end-user growth trajectory.

• By Region

- North America contributed 41.5% of global revenue for the Life Science and Analytical Instruments Market in 2025.

- Asia-Pacific is tracking a 9.67% CAGR, the highest among all regions, fueled by CDMO capacity build-outs.

Life Science and Analytical Instruments Market Size and Forecast (2021–2035)

Market Research Future employs a bottom-up estimation model that aggregates instrument shipment data, vendor revenue disclosures, and end-user procurement surveys across 42 countries. Historical figures (2021–2024) are validated against customs-trade databases and public financial filings; forecast projections (2026–2035) incorporate regression analysis calibrated to R&D expenditure trends, regulatory pipeline activity, and installed-base replacement cycles.