Linear Motor Market Summary

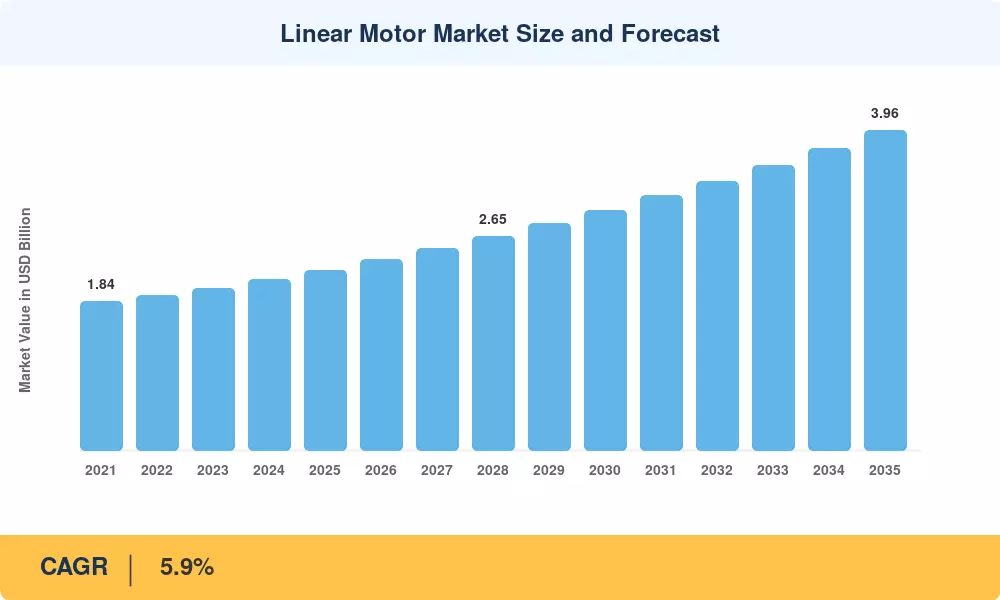

The global Linear Motor Market reached an estimated USD 2.23 Billion in 2025 and is projected to grow from USD 2.36 Billion in 2026 to USD 3.96 Billion by 2035, registering a CAGR of 5.9% during the forecast period (2026–2035). This expansion is anchored in accelerating semiconductor capital expenditure cycles — global wafer fab equipment spending topped USD 100 Billion in 2023 [1] — and the parallel push toward high-precision automation across electronics, automotive, and packaging lines. Government programs such as the U.S. CHIPS and Science Act and the European Chips Act are channeling tens of billions of dollars into domestic semiconductor manufacturing, directly lifting demand for sub-micron positioning stages that rely on linear motors.

Traditional ball-screw and belt-drive motion systems are steadily giving way to direct-drive linear motor platforms that eliminate mechanical backlash, reduce maintenance downtime, and deliver positioning repeatability below one micrometer. This technology transition is reinforced by Industry 4.0 mandates and the integration of AI-driven servo control, enabling real-time adaptive tuning of thrust profiles. The International Federation of Robotics reported a global operational robot stock exceeding 4.2 million units in 2024 [2], many of which interface with linear motor stages for pick-and-place, inspection, and micro-assembly tasks.

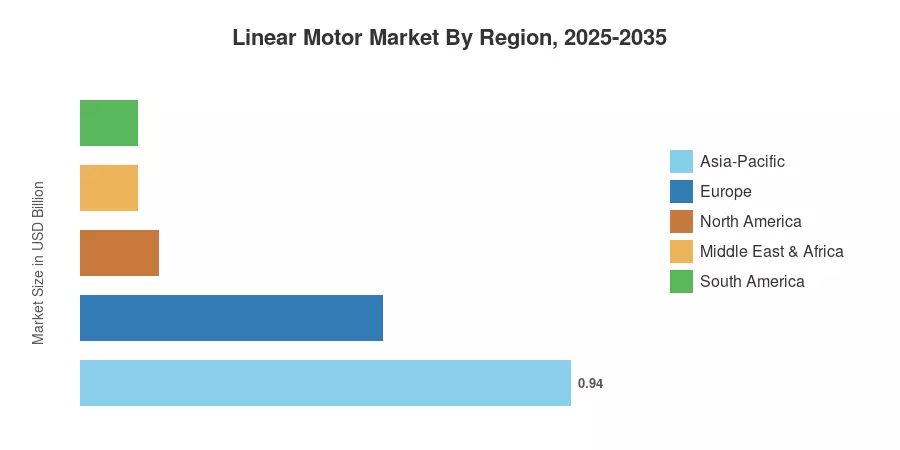

Asia-Pacific commands the largest share of the Linear Motor Market at approximately 42%, driven by China, Japan, and South Korea's dominance in semiconductor and flat-panel display fabrication. North America is the fastest-growing region with a projected CAGR of 6.8%, fueled by reshoring incentives and advanced manufacturing investment. Europe holds the second-largest share at roughly 26%, supported by Germany's precision machine tool ecosystem. As nanoscale manufacturing tolerances tighten and electric vehicle production ramps, the Linear Motor Market is positioned for sustained, broad-based growth through 2035.

Key Report Takeaways

• By Design

- Flat Plate linear motors account for approximately 42% of global revenue, reflecting their dominance in semiconductor lithography and precision inspection stages.

- The Cylindrical segment is forecast to register the highest CAGR at 6.7% through 2035, propelled by automotive production line automation and compact actuator demand.

- U-Channel designs contribute roughly USD 0.45 Billion in 2025 value, favored in heavy-payload machine tool applications.

• By Application

- Electrical and Electronics manufacturing leads application demand in the Linear Motor Market, holding an estimated 28% share.

- The Automotive segment is expanding at a CAGR of 6.3%, driven by EV powertrain assembly and battery cell production.

- Food and Beverage packaging lines account for approximately USD 0.27 billion, increasingly adopting linear motors for hygienic, contactless conveying.

• By Region

- Asia-Pacific dominates with a 42% share of the Linear Motor Market, led by semiconductor and display fabrication hubs in China and South Korea.

- North America is projected to grow at a CAGR of 6.8%, the fastest among all regions.

- Europe holds approximately 26% of global revenue, anchored by Germany's machine tool and automotive sectors.

Market Size and Forecast (2021–2035)

Market sizing is based on a combination of bottom-up revenue analysis from equipment OEMs, distributor sell-through data, and top-down macroeconomic validation against industrial automation capital expenditure trends. Historical figures (2021–2024) reflect actual performance; the base year 2025 is estimated; and the forecast period 2026–2035 applies a calibrated CAGR of 5.9%.