Liquid Nitrogen Market Summary

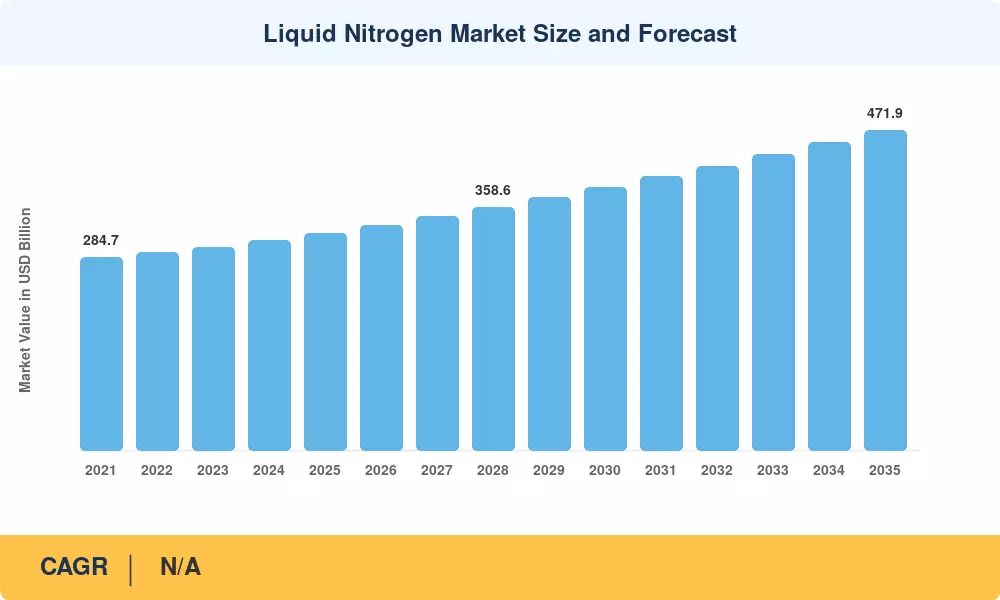

The Liquid Nitrogen Market reached a valuation of USD 319.5 Million in 2025 and is projected to grow from USD 331.5 Million in 2026 to USD 471.9 Million by 2035, expanding at a compound annual growth rate of 4.0% during 2026–2035. Two catalysts anchor this trajectory: accelerating semiconductor fabrication investments across East Asia — where ultra-pure nitrogen atmospheres are non-negotiable — and the global push toward biologics cold-chain infrastructure mandated by evolving WHO and FDA temperature-integrity guidelines [1]. Long-term supply agreements between air-separation-unit operators and anchor customers underpin pricing stability, insulating the Liquid Nitrogen Market from spot-market volatility that periodically rattles other commodity chemicals.

The industry is transitioning away from legacy bulk-delivery logistics toward digitally optimized, application-engineered supply chains. Vertically integrated majors are deploying IoT-enabled tank telemetry and energy-efficient cryogenic plants that reduce delivered cost by an estimated 12–18% compared to 2020 baselines [2]. Policy tailwinds — including the U.S. CHIPS and Science Act's USD 52.7 Billion allocation and the EU Chips Act's EUR 43 Billion target — are pulling forward capacity additions in electronics-grade nitrogen, reshaping the Liquid Nitrogen Market's revenue mix toward higher-margin specialty segments.

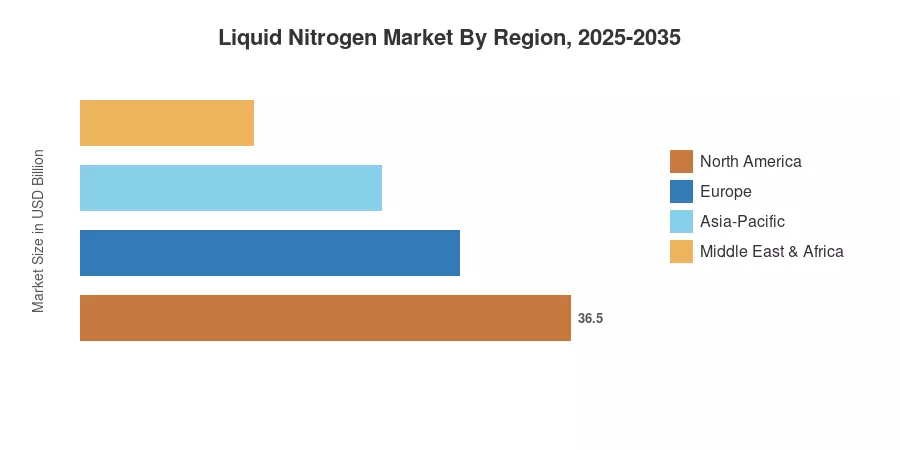

Asia-Pacific commands roughly 49.2% of global revenue, driven by China's semiconductor expansion and India's biologics manufacturing capacity. The region also posts the fastest growth at a 4.7% CAGR through 2035. North America holds the second-largest position with approximately 24.3% share, sustained by outpatient oncology adoption and pharmaceutical logistics modernization. Europe follows at 18.1%, supported by automotive lightweighting and renewable-energy component manufacturing. The Liquid Nitrogen Market is poised for sustained expansion as application complexity deepens across every major consuming sector.

Key Report Takeaways — Liquid Nitrogen Market

By Storage Type

- Packaged gas accounted for 70.0% of the Liquid Nitrogen Market in 2025, reflecting the dominance of standardized delivery formats across healthcare and laboratory end users.

- Cylinder storage is forecast to expand at a 4.5% CAGR through 2035, outpacing the overall market as point-of-use deployments in smaller clinical and research facilities proliferate.

By Function

- Coolant applications commanded 61.5% of the Liquid Nitrogen Market in 2025, anchored by demand from semiconductor wafer processing and pharmaceutical freeze-drying operations.

- Refrigerant use is advancing at a 5.1% CAGR to 2035, accelerated by regulatory phase-downs of high-GWP synthetic refrigerants under the Kigali Amendment.

By End-User Industry

- The chemical and pharmaceutical segment represented 28.5% of the Liquid Nitrogen Market in 2025, reflecting nitrogen's role as an inert blanketing agent and cryogenic process enabler.

- The food and beverage segment is growing fastest at a 5.3% CAGR through 2035, propelled by flash-freezing adoption and modified-atmosphere packaging expansion.

By Region

- Asia-Pacific led with 49.2% revenue share in 2025 and is forecast to register the highest regional CAGR of 4.7% to 2035.

- North America contributed approximately USD 77.6 Million in 2025, sustained by robust pharmaceutical cold-chain investments.

Liquid Nitrogen Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated estimation methodology combining top-down industry benchmarking, bottom-up plant-capacity audits, and proprietary trade-flow databases validated against customs and industry-association datasets. Historical figures (2021–2024) are derived from audited company filings and government trade statistics; forecast values (2026–2035) apply econometric demand modeling correlated with GDP growth, semiconductor capex cycles, and cold-chain infrastructure spending [3].

.webp?v=1783928659)