Long Fiber Thermoplastics Market Summary

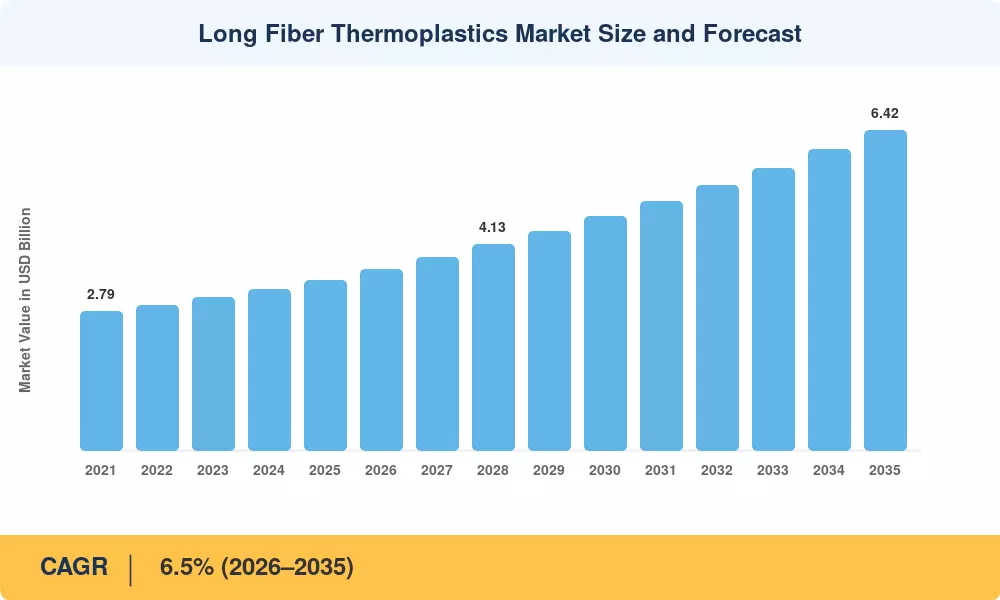

The Long Fiber Thermoplastics Market reached an estimated USD 3.42 billion in 2025 and is projected to grow from USD 3.64 billion in 2026 to USD 6.42 billion by 2035, registering a CAGR of 6.5% during the forecast period. Stringent automotive emissions standards — including the EU's Euro 7 framework and U.S. CAFE targets [1] — are compelling OEMs to adopt lighter structural materials, and long fiber thermoplastics sit at the intersection of weight reduction and cost efficiency. Government-backed lightweighting initiatives across major auto-producing nations continue to funnel R&D funding into this space.

A pronounced shift away from traditional metal stampings and short-fiber compounds toward continuous-fiber-reinforced alternatives is reshaping the Long Fiber Thermoplastics Market. Automakers alone have committed over USD 4.8 billion in lightweighting programs through 2030 [2], creating a pull effect that benefits LFT producers scaling up direct-inline compounding and pultrusion technologies. Aerospace interior programs and electronics housings are adding incremental demand channels.

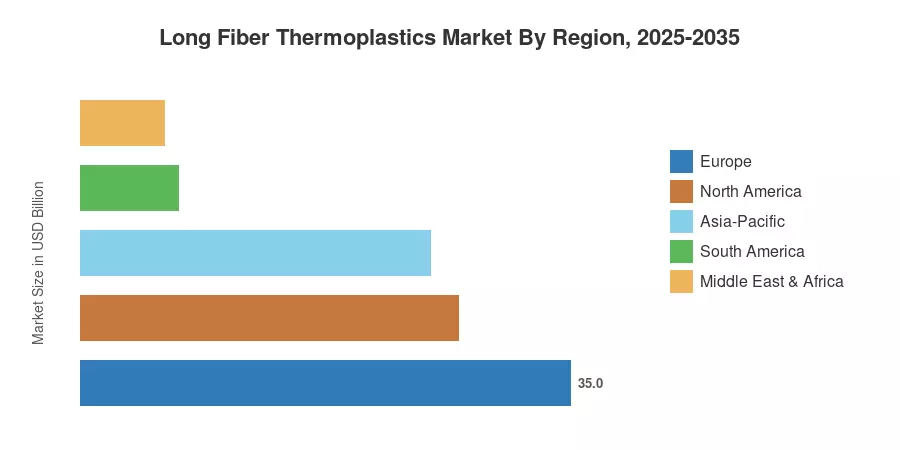

Europe commands the largest regional share at roughly 35% of the Long Fiber Thermoplastics Market, driven by Germany's automotive cluster and Italy's appliance sector. Asia-Pacific is the fastest-growing region with a projected CAGR of 7.8%, fueled by China's EV expansion and India's infrastructure build-out. North America holds the second-largest share, near 27%, anchored by pickup-truck underbody shields and consumer electronics enclosures. The decade ahead will be defined by capacity expansions in Southeast Asia and circular-economy formulations in Europe.

Key Report Takeaways

• By Resin Type

- Polypropylene-based LFT holds the dominant share at approximately 48% of the Long Fiber Thermoplastics Market, reflecting its cost-to-performance advantage in automotive under-hood and structural parts.

- Polyamide LFT is the fastest-growing resin segment, posting a CAGR of 7.4% as demand rises for heat-resistant components in EV powertrains.

• By End-User Industry

- The automotive sector accounts for roughly 45% of global demand, reinforced by regulatory pressure to cut vehicle mass.

- Electrical and electronics applications are expanding at a CAGR of 7.1%, supported by 5G infrastructure rollouts and miniaturized housing designs.

• By Region

- Europe leads the Long Fiber Thermoplastics Market with a 35% share, anchored by OEM lightweighting mandates.

- Asia-Pacific is forecast to grow at a CAGR of 7.8%, the highest among all regions, driven by China and India.

Market Size and Forecast (2021–2035)

Market Research Future's sizing methodology combines primary interviews with Tier-1 compounders, trade-association production data, and downstream OEM procurement disclosures. Historical figures reflect actual shipments; forecast values apply the calibrated CAGR with adjustments for planned capacity additions and regulatory timelines.