Makeup Remover Market Summary

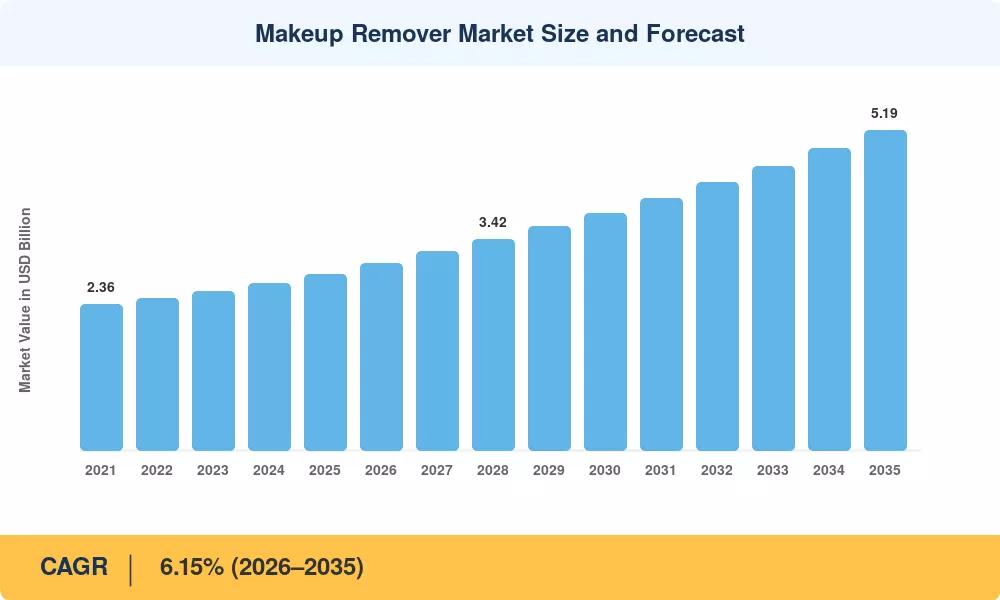

The Makeup Remover Market stood at USD 2.86 billion in 2025 and is projected to reach USD 5.19 billion by 2035, expanding at a CAGR of 6.15% during the 2026–2035 forecast period. This trajectory is rooted in shifting consumer perceptions of cleansing — no longer a quick end-of-day chore, but a deliberate step in multi-stage skincare routines backed by dermatological research. Regulatory momentum, particularly the U.S. Modernization of Cosmetics Regulation Act of 2022 (MoCRA), has compelled manufacturers to register facilities and list products with the FDA, raising compliance costs but simultaneously clearing counterfeit products from shelves and rewarding established brands with stronger consumer trust [1].

Formulation science has advanced rapidly across the Makeup Remover Market. Legacy alcohol-laden toners and harsh surfactant wipes are giving way to micro-emulsion technologies, water-free fiber substrates, and enzyme-activated cleansing balms that dissolve long-wear and waterproof cosmetics without stripping the skin barrier. Global investment in clean-beauty R&D surpassed USD 1.8 billion in 2024, according to industry estimates, as conglomerates race to reformulate portfolios around biodegradable actives and upcycled botanical extracts.

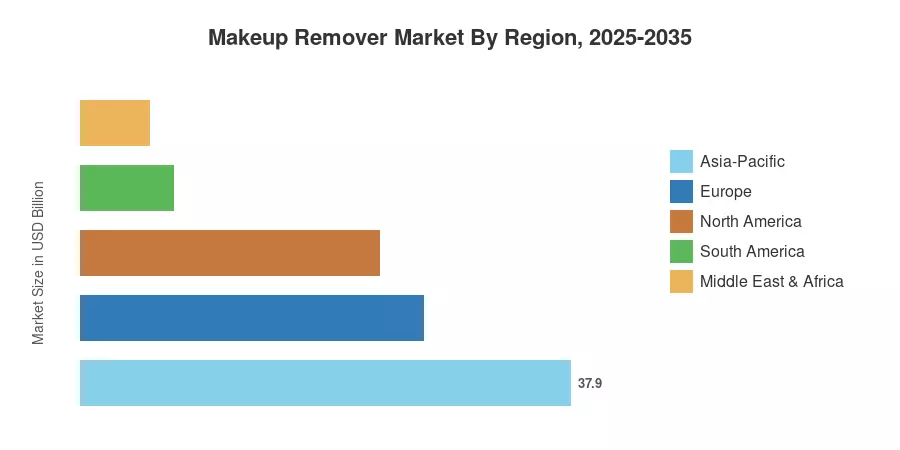

Asia-Pacific commands the largest share of the Makeup Remover Market at approximately 37.9% of 2025 revenue, propelled by deeply embedded K-beauty and J-beauty routines that normalize multi-step cleansing. The region is also the fastest-growing, forecast to register a 7.96% CAGR through 2035. Europe holds the second-largest position at roughly 26.5% share, driven by EU cosmetics regulation tightening and rising demand for organic-certified formulations [3]. North America rounds out the top three, with premiumization and dermatologist-endorsed product lines fueling steady expansion. As social media platforms continue to amplify skincare education globally, the Makeup Remover Market is positioned for broadening penetration across income segments and geographies alike.

Key Report Takeaways

• By Product Type

- Cleansing Liquids and Micellar Water captured approximately 37.4% of Makeup Remover Market revenue in 2025, reflecting consumer preference for no-rinse, low-irritation formats.

- Cleansing Oils and Balms are forecast to register the fastest segment CAGR of 7.69% through 2035, driven by the global spread of double-cleansing practices.

• By Category

- Conventional formulations accounted for roughly 77.4% of Makeup Remover Market share in 2025, underscoring their price accessibility across mass channels.

- Organic variants are projected to grow at an 8.65% CAGR to 2035 as clean-beauty certifications gain traction.

• By Distribution Channel

- Health and Beauty Stores held an estimated 47.9% share of the Makeup Remover Market in 2025, benefiting from in-store sampling and expert consultations.

- Online Retail is expected to post the channel's highest CAGR of 8.78% through 2035.

• By Region

- Asia-Pacific led the Makeup Remover Market with 37.9% share in 2025, while South America presents strong latent demand with accelerating urbanization rates.

- Europe represented the second-largest region at approximately 26.5% share.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model integrates bottom-up revenue estimates from 45+ countries with top-down cross-validation against trade databases, corporate filings, and customs data. Historical figures (2021–2024) are actuals; the base year (2025) blends trailing actuals with early-year shipment data; forecast years (2026–2035) apply segment-weighted CAGR projections adjusted for regulatory, demographic, and macroeconomic variables.