Manufactured Housing Market Summary

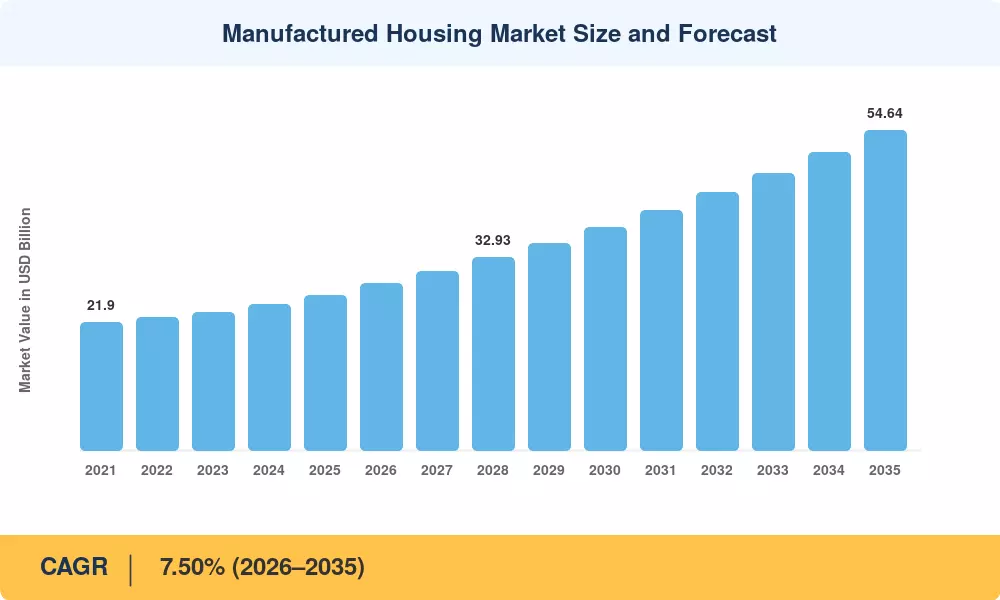

The manufactured housing market was valued at USD 26.50 billion in 2025 and is projected to grow from USD 28.49 billion in 2026 to USD 54.64 billion by 2035, registering a CAGR of 7.50% during the forecast period. This expansion is anchored by a persistent affordability crisis across developed economies, where the average factory-built home costs roughly USD 128,000 before land — a fraction of the USD 315,000-plus price tag attached to conventional site-built construction [1]. The September 2024 HUD code revision, permitting up to four-unit manufactured configurations, has opened a new pathway for workforce housing pipelines and build-to-rent portfolios [2].

Traditional site-built construction continues to lose market share to controlled-environment production methods, which decrease build cycles by 30–50% and material waste by up to 15%. Fannie Mae and Freddie Mac duty-to-serve regulations have opened up secondary-market financing for chattel loans [3], bringing institutional capital into a category that was hitherto exclusive to personal-property lending. In 2024, shipments increased to almost 110,000 units, up around 16% year over year but still far below historical peaks, indicating a lot of untapped potential in the manufactured home business [1].

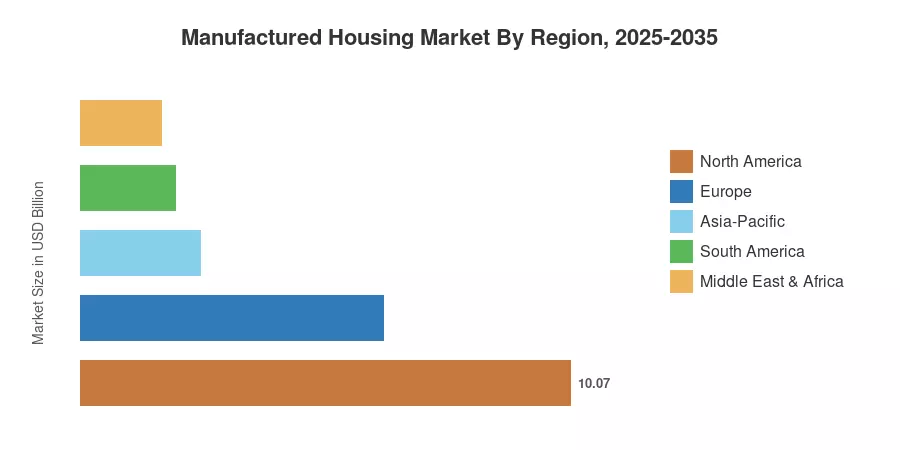

North America has the largest revenue share of 38.0% in 2025, driven by federal incentive schemes and increasing investment in land-lease communities. Asia-Pacific is expected to be the fastest-expanding market for manufactured housing with a CAGR of 9.30% over the forecast period. This growth is attributed to prefabrication targets in China and housing-for-all initiatives in India. Sustainability regulations and volumetric modular uptake in the UK and Scandinavia buoy Europe to the second greatest market share at 23.5%. Over the next decade, manufactured housing is projected to transition from a niche cost-saving alternative to a mainstream pillar of residential supply chains around the world.

Key Report Takeaways

• By Structure Type

- Multi-section units held an estimated 53.2% of the manufactured housing market in 2025, reflecting buyer preference for larger floor plans that rival site-built homes in livable area.

- Other structure types, including compact and tiny-home configurations, are forecast to grow at a 7.17% CAGR through 2035 as downsizer demand intensifies.

• By Application

- Single-family deployments commanded approximately 71.0% of the manufactured housing market size in 2025, underscoring the dominance of owner-occupied and land-lease placements.

- Multi-family formats are projected to expand at an 8.59% CAGR to 2035, fueled by build-to-rent operators and workforce housing developers.

• By Material

- Timber-framed units captured 46.2% of 2025 revenue, benefiting from a mature supply chain and favorable strength-to-weight ratios.

- Concrete-based systems represent the fastest-growing material category in the manufactured housing market, advancing at an 8.68% CAGR through 2035.

• By Geography

- North America generated 38.0% of 2025 revenue in the manufactured housing market, led by the United States' robust community-acquisition pipeline.

- Asia-Pacific is set to accelerate at a 9.30% CAGR through 2035 on the back of ambitious government prefabrication mandates across China and India.

Manufactured Housing Market Size and Forecast (2021–2035)

Market Research Future (MRFR)’s forecasting model combines bottom-up manufacturer shipment data, regional permit filing data, trade association statistics from the Manufactured Housing Institute, and proprietary demand indices based on census and HUD databases. Historical numbers are based on real industry data, and predictions for the forecast period are based on the calibrated 7.50% CAGR with adjustments for expected regulatory and macroeconomic changes.