Medical Carts Market Summary

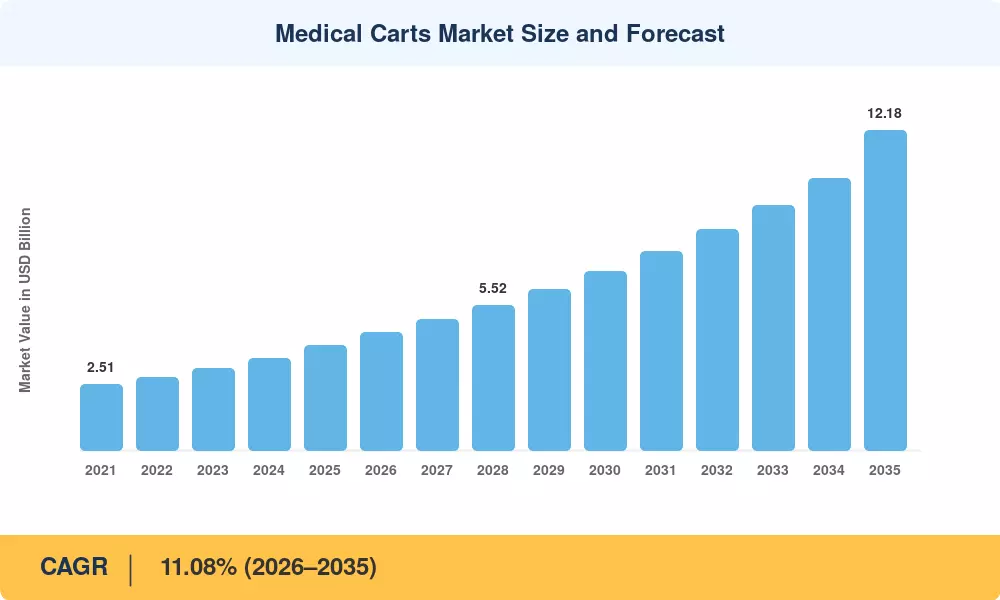

The Medical Carts Market was valued at USD 3.99 billion in 2025 and is projected to reach USD 4.49 billion by 2026, growing to USD 12.18 billion by 2035 at a CAGR of 11.08% during 2026–2035. This expansion is driven by the accelerating digitization of hospital utility carts and the integration of electronic health records into bedside nursing cart workflows. Capital investment from health systems prioritizing value-based reimbursement models — estimated at over USD 38 billion globally in clinical IT infrastructure through 2028 — is reshaping procurement strategies for medication dispensing carts and mobile workstation for clinicians platforms[2].

Likewise, there is a migration from manual traditional supply carts and paper-based systems of medication tracking to networked, sensor-equipped crash cart emergency equipment with real-time inventory management and traceability facilitated by RFID. In 2024, the U.S. Department of Health and Human Services gave USD 1.7 billion in grants to modernize hospitals, with a significant chunk of the funding going to point-of-care recording platforms built around mobile workstations for clinicians' designs [3]. EU Battery Regulation 2023/1542 is also boosting the engineering bar for powered cart platforms across European sites.

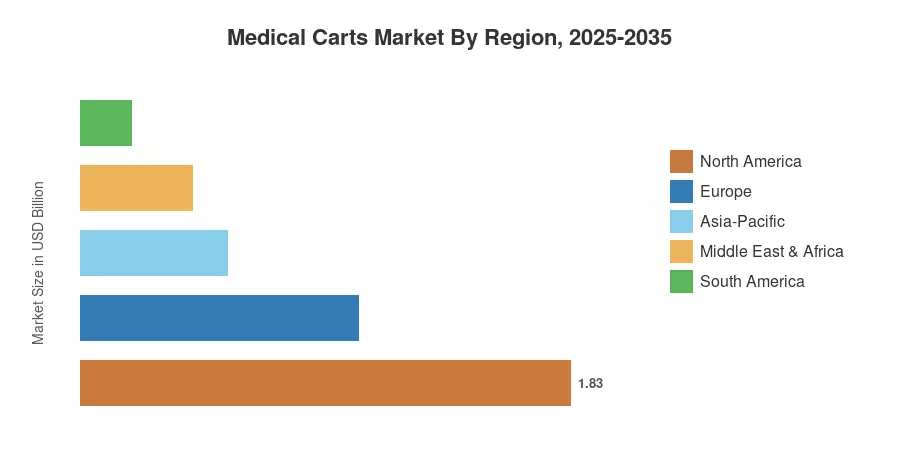

The Market for Medical Carts in North America is estimated to account for ~45.89% of the Market, driven by the acute-care expenditure in the U.S. and Canada. The Asia-Pacific region is the fastest-growing region with a CAGR of 13.82%. The construction boom in hospitals in India, China and the ASEAN countries drives this growth. Europe is the second greatest share with about 26% of worldwide sales, driven by digitalization efforts at the NHS and Germany’s Hospital Future Act As staff shortages continue to increase worldwide, the demand for automated medicine dispensing carts and ergonomic bedside nursing cart solutions will increase more rapidly until 2035.

Key Report Takeaways

• By Cart Type

- Emergency carts captured 43.78% of the Medical Carts Market share in 2025, reflecting sustained demand for crash cart emergency equipment in acute-care and trauma settings

- Workstations-on-wheels are the fastest-expanding category, growing at a 13.08% CAGR through 2035 as the adoption of mobile workstations for clinicians deepens

• By Power Source

- Non-powered hospital utility carts accounted for 56.31% of the Medical Carts Market in 2025, remaining dominant in resource-constrained facilities

- The powered variants are projected to post the highest CAGR through 2035

• By End User

- Hospitals represented 55.87% of end-user revenue in 2025, though ambulatory surgical centers are expanding at a 12.85% CAGR

- The Medical Carts Market in Asia-Pacific is on track for a 13.82% CAGR, outpacing all other regions through 2035

Medical Carts Market Size and Forecast (2021–2035)

Market Research Future (MRFR) uses a unique research methodology to bring to light the market sizing of the Healthcare Asset Management Market. The analysis is based on a two-step process, which comprises primary and secondary research. Historical numbers (2021–2024) are based on actual trade volumes; the 2026–2035 prediction is based on a bottom-up model with facility-level adoption rates for pharmaceutical dispensing carts and mobile workstation for clinicians platforms.