Medical Device Connectivity Market Summary

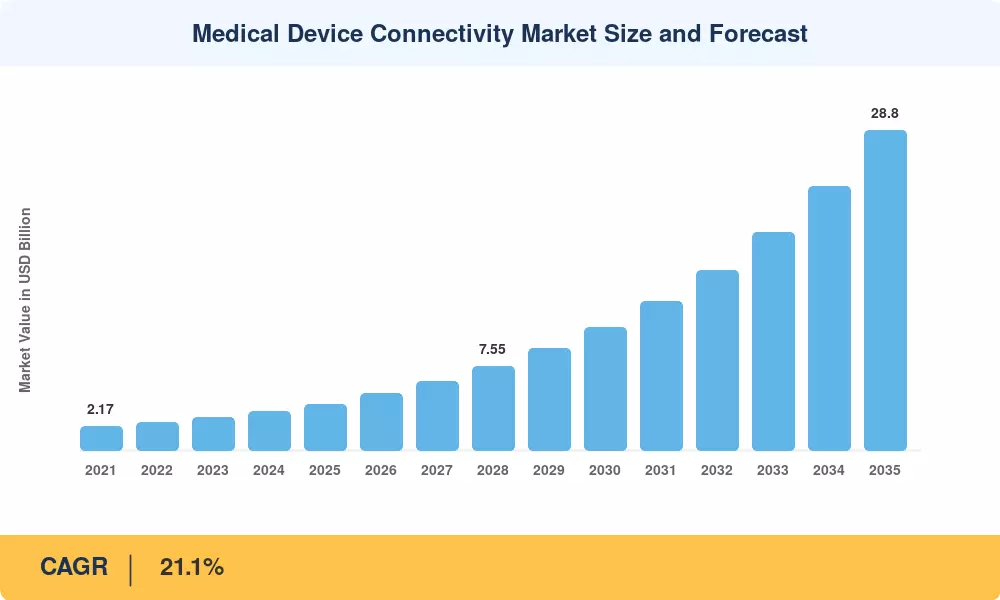

The Medical Device Connectivity Market size was valued at USD 4.18 Billion in 2025, and the market is projected to grow from USD 5.15 Billion in 2026 to USD 28.80 Billion by 2035, registering a CAGR of 21.1% during the forecast period 2026–2035. This growth trajectory reflects a fundamental shift in how clinical devices communicate with enterprise health IT systems — a shift catalyzed by the US 21st Century Cures Act's information-blocking provisions and the European Health Data Space regulation, both of which penalize proprietary data silos and incentivize open-standard connectivity [1][2]. Hospital systems that once tolerated manual transcription of bedside-device readings now face workforce shortages severe enough that automated data capture is no longer optional; it is an operational imperative.

The technology space is clearly shifting away from antiquated serial-port interfaces and point-to-point middleware to cloud-native integration engines based on HL7 FHIR and IEEE 11073 standards. In 2024, global healthcare IT capital spending exceeded USD 630 billion, with a greater share of spending going toward connection infrastructure as health organizations look to real-time clinical decision support and predictive analytics [3]. In the US, EU and Japan, regulatory agencies are increasing cybersecurity requirements for connected medical devices, forcing manufacturers to include secure communication protocols at the design stage rather than adding them to legacy gear.

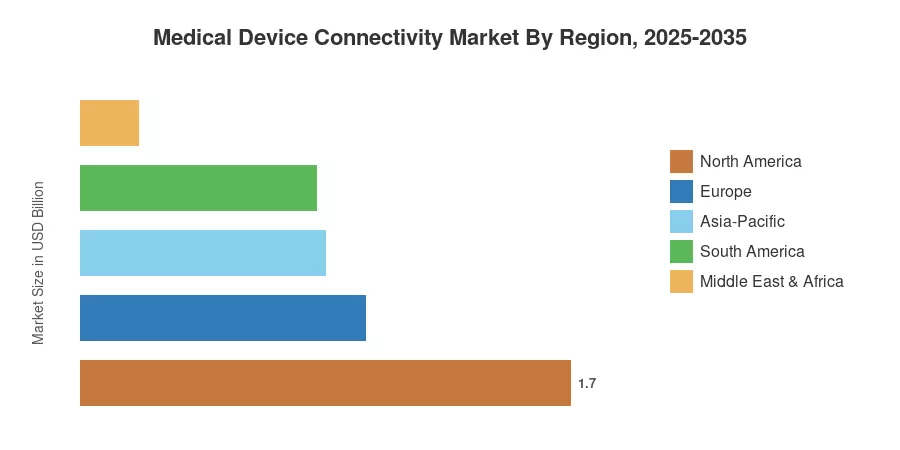

North America accounted for a share of around 40.7% of the Medical Device Connectivity Market in 2025, owing to high acute-care IT investment and mature EHR adoption rates around 95% across US hospitals [4]. Europe is the fastest-expanding region, supported by the EU4Health digital transformation strategy and increased post-pandemic telemedicine deployments. The Asia-Pacific region garnered the second-largest share of 20.3%, supported by India’s Ayushman Bharat Digital Mission and China’s rise in smart-hospital building [5]. The Medical Device Connectivity Market is poised for continued double-digit increase through 2035, with 5G and early 6G research providing ultra-reliable low-latency links for critical care.

Key Report Takeaways

• By Component

- Connectivity solutions accounted for 67.3% of the Medical Device Connectivity Market share in 2025, reflecting strong demand for device interface modules and gateway hardware.

- Connectivity services are forecast to grow at a 23.2% CAGR through 2035, with implementation and integration engagements driving recurring revenue.

• By Technology

- Wired interfaces held 61.4% of the Medical Device Connectivity Market in 2025, though wireless technologies are expanding rapidly as hospitals upgrade to Wi-Fi 6E and Bluetooth 5.3 infrastructure.

- Wireless connectivity is projected to register a 22.9% CAGR between 2026 and 2035.

• By Application

- Continuous patient monitoring represented 49.2% of the Medical Device Connectivity Market in 2025, fueled by sepsis-alert and early-warning-score algorithms that require uninterrupted device data streams.

- Tele-ICU and tele-stroke applications are forecast to advance at a 24.2% CAGR, reflecting specialist-shortage pressures across rural and mid-size hospitals.

• By End User

- Hospitals and clinics commanded 71.4% of the Medical Device Connectivity Market share in 2025.

- Home healthcare is poised for the fastest segment growth at a 24.8% CAGR, as chronic-disease management shifts to decentralized settings.

• By Geography

- North America led with 40.7% of global revenue in 2025.

- Europe is set to expand at the highest regional CAGR, supported by cross-border data exchange mandates.

- Asia-Pacific represented USD 0.85 billion in 2025 and is accelerating through government-backed digitization programs.

Market Size and Forecast (2021–2035)

Historical period (2021–2024) data is based on verified industry disclosures, public corporate filings and regulatory databases. A custom bottom-up model was used for the projected period (2026-2035), which was benchmarked against primary interviews with hospital CIOs, device OEMs, and integration specialists. All amounts are at unchanged 2025 exchange rates, in USD billion.