Medical Dynamometer Market Summary

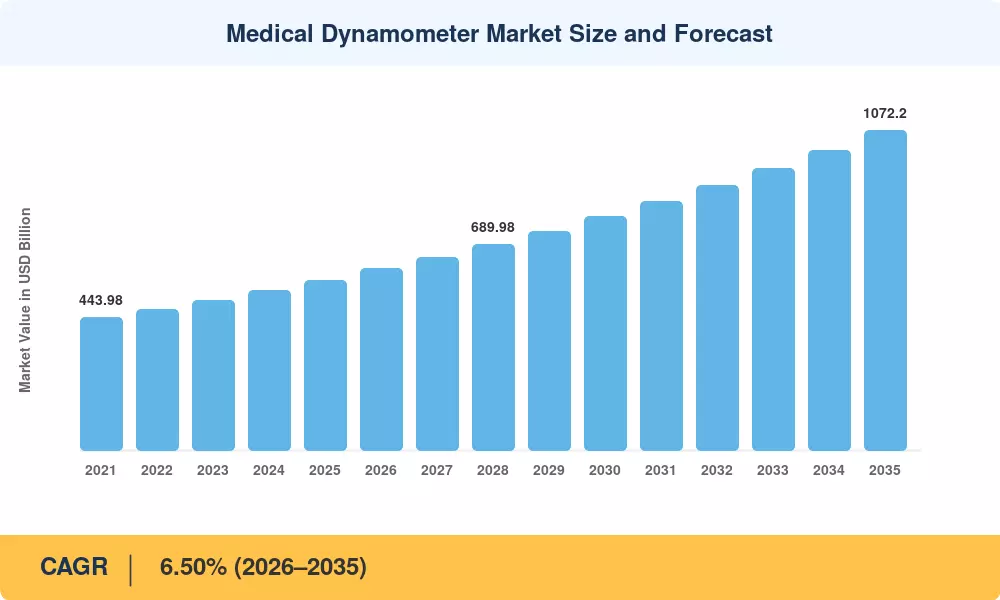

The Global Medical Dynamometer Market size was valued at USD 571.20 Million in 2025, and the market is projected to grow from USD 608.33 Million in 2026 to USD 1,072.20 Million by 2035, registering a CAGR of 6.50% during the forecast period 2026–2035. Two forces are accelerating this trajectory: the World Health Organization's formal recognition of sarcopenia as a coded muscle disorder (ICD-10-CM M62.84) and the Centers for Medicare & Medicaid Services' shift toward value-based reimbursement models that reward objective, quantifiable patient-outcome data [1]. These policy-level catalysts have transformed dynamometry from a niche rehabilitation accessory into a clinical-grade diagnostic baseline.

Legacy analog spring-scale devices — still an estimated 30% of deployed systems in low- and middle-income settings — are being replaced with digital load-cell platforms with Bluetooth, Wi-Fi and EHR connection. Now, the European Commission’s Medical Device Regulation (EU MDR 2017/745) has applied the need for full traceability for measurement data, thereby ruling out non-connected instruments. Hospitals in the G7 have allocated a total of USD 2.3 billion for rehabilitation-technology upgrades in 2024–2027, and dynamometer procurement accounts for around 8–10% of these expenditures [2].

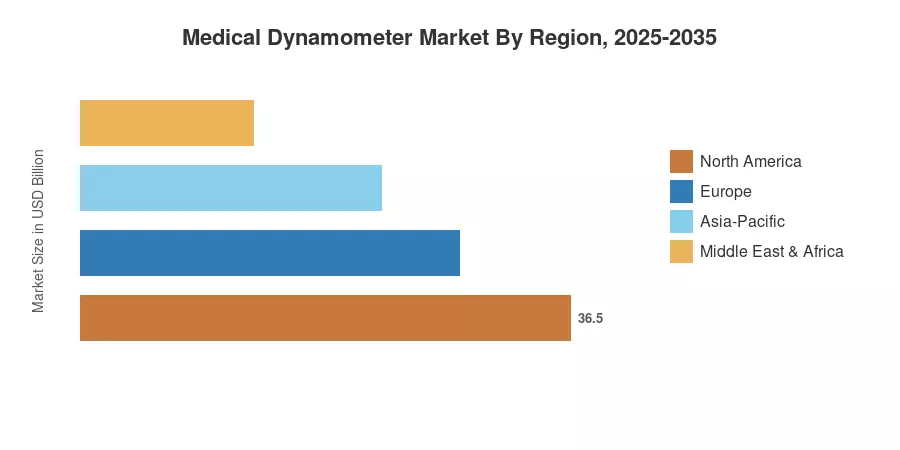

North America holds a 32.5% share of the medical dynamometer market, due to rising Medicare coverage for post-acute strength assessment. Asia-Pacific is likely to be the fastest developing market, with a projected CAGR of 11.1% from 2023 to 2035, as Japan’s super-aged culture and India’s burgeoning physiotherapy infrastructure provide dual demand poles. The second largest market is Europe, with a share of 27.0% based on the German statutory health insurance system and the NHS rehabilitation framework in the UK. The dominant factor in procurement cycles in every major health institution over the next decade will be connected, AI-enabled devices.

Key Report Takeaways

• By Product Type

- Hand dynamometers accounted for 34.0% of the medical dynamometer market in 2025, reflecting their ubiquity in outpatient grip-strength screening protocols.

- Multifunction and smart app-enabled dynamometers are the fastest-growing product category, forecast to expand at a 13.7% CAGR through 2035.

- Push-pull dynamometers contributed USD 125.66 million in 2025 revenue, underpinned by orthopedic and occupational-therapy demand.

• By Application

- Orthopedics and sports medicine represented 41.5% of the medical dynamometer market share in 2025.

- Neurology and stroke rehabilitation are projected to grow at a 12.1% CAGR to 2035, fueled by the aging population and stroke incidence.

• By Geography

- North America retained the dominant share of the medical dynamometer market, driven by Medicare reimbursement expansion.

- Asia-Pacific is set for the fastest regional expansion at an 11.1% CAGR, with Japan and India as lead contributors.

- Europe accounted for 27.0% of global revenue in 2025.

Medical Dynamometer Market Size and Forecast (2021–2035)

Market Research Future employs a multi-approach triangulation strategy that combines top-down and bottom-up approaches, such as hospital procurement databases, manufacturer revenue disclosures, insurance-claim numbers, and trade-shipment data. Historical figures (2021–2024) are based on audited results; the 2025 base year is approximated based on partial-year data; and the 2026–2035 forecast is based on a calibrated compound growth model using demographic, regulatory, and technology-adoption inputs as the basis.