Medical Equipment Rental Market Summary

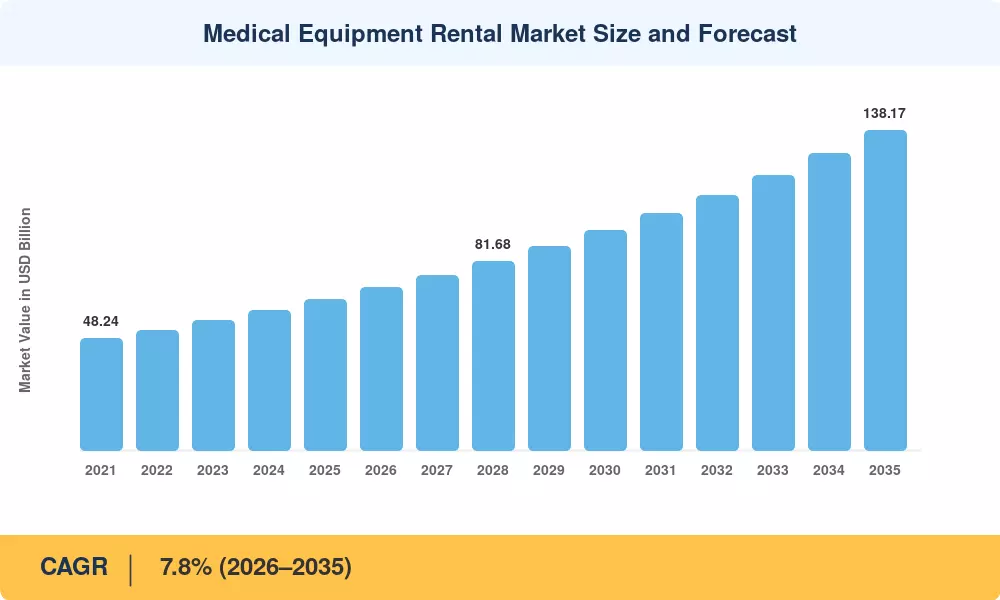

The Global Medical Equipment Rental Market size was valued at USD 65.20 Billion in 2025, and the market is projected to grow from USD 70.29 Billion in 2026 to USD 138.17 Billion by 2035, registering a CAGR of 7.8% during the forecast period 2026–2035. Two catalysts are accelerating this expansion: the U.S. Centers for Medicare & Medicaid Services (CMS) broadened its Hospital-at-Home waiver program in 2024, extending acute-care reimbursement to rented bedside devices in over 300 health systems [1], and the European Commission earmarked EUR 4.2 billion under the EU4Health 2024–2027 cycle for cross-border equipment-sharing consortia [2].

A technology overhaul is reshaping how providers source critical assets. Legacy outright-purchase models—where hospitals locked USD 1.5–8 Million per MRI or CT unit into 10-year depreciation schedules—are giving way to subscription-style rental platforms that embed predictive-maintenance telemetry, IoT utilization dashboards, and automated compliance tracking. BloombergNEF estimates that connected medical-device fleet management attracted USD 2.8 billion in venture funding during 2023–2024 alone [3]. These platforms compress technology refresh cycles from seven years to roughly three, enabling facilities to swap older imaging suites for AI-augmented models without a balance-sheet hit.

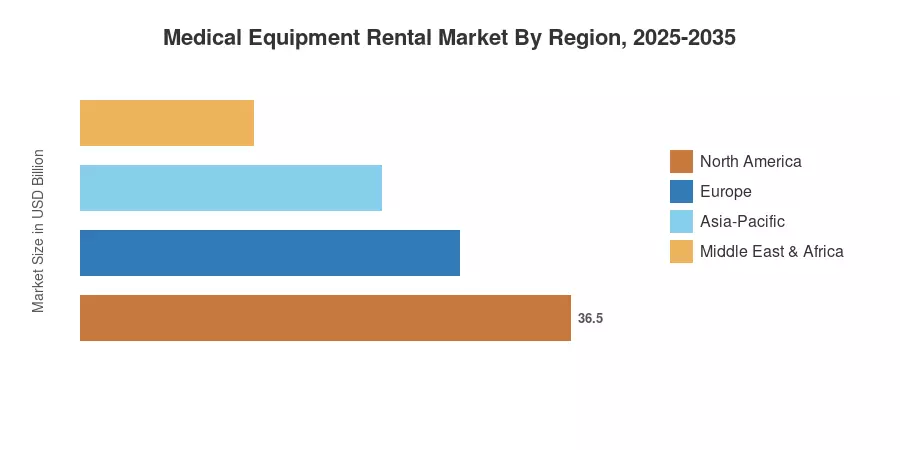

North America commands a 33.5% share of the medical equipment rental market, anchored by flexible GPO (group purchasing organization) contracting and a mature insurance-reimbursement ecosystem. Asia-Pacific is the fastest-growing region at a 7.1% CAGR, fueled by India's Ayushman Bharat Digital Mission and China's county-hospital modernization program. Europe holds the second-largest position with 31.4% share, supported by its longstanding statutory health insurance rental reimbursement frameworks. The convergence of aging demographics, value-based care mandates, and digital fleet analytics points toward sustained double-digit rental penetration gains across all five regions through 2035.

Key Report Takeaways

• By Device Category

- Durable Medical Equipment captured 32.4% of the medical equipment rental market in 2024, driven by wheelchair, hospital-bed, and respiratory-device demand across acute and post-acute settings.

- Surgical and Procedural Equipment is forecast to expand at a 6.9% CAGR through 2035, as ambulatory surgery centers increasingly rent robotic-assisted platforms rather than purchasing them.

- Home-care and Personal-use Equipment is advancing at a 7.9% CAGR, reflecting hospital-at-home program proliferation and payer support for remote patient monitoring devices.

• By End User

- Hospitals and Acute-Care Centers held 26.2% revenue share of the medical equipment rental market in 2024, leaning on rental to flex ICU capacity during seasonal surges.

- Home-care Patients are growing at an 8.4% CAGR, the fastest end-user segment, boosted by post-pandemic reimbursement expansions.

• By Service Type

- Long-Term Rentals captured 34.2% share in 2024, favored by skilled-nursing facilities seeking predictable monthly OpEx.

- Short-Term Rentals are projected to register the fastest CAGR of 8.9% through 2035, propelled by disaster-preparedness stockpiling contracts and elective-surgery rental bundles.

• By Region

- Europe commanded a 31.4% share of the medical equipment rental market in 2024.

- Asia-Pacific is poised for a 7.1% CAGR to 2035, led by government infrastructure investment across India and China.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model triangulates top-down revenue estimates from company filings, rental-fleet utilization databases, and payer-reimbursement data with bottom-up demand modeling across device categories, end users, and geographies. Historical figures (2021–2024) draw on audited annual reports and trade-association surveys; forecast figures (2026–2035) apply a calibrated 7.8% CAGR adjusted for macro-health-expenditure trajectories published by the WHO and OECD [4].