Medical Marijuana Market Summary

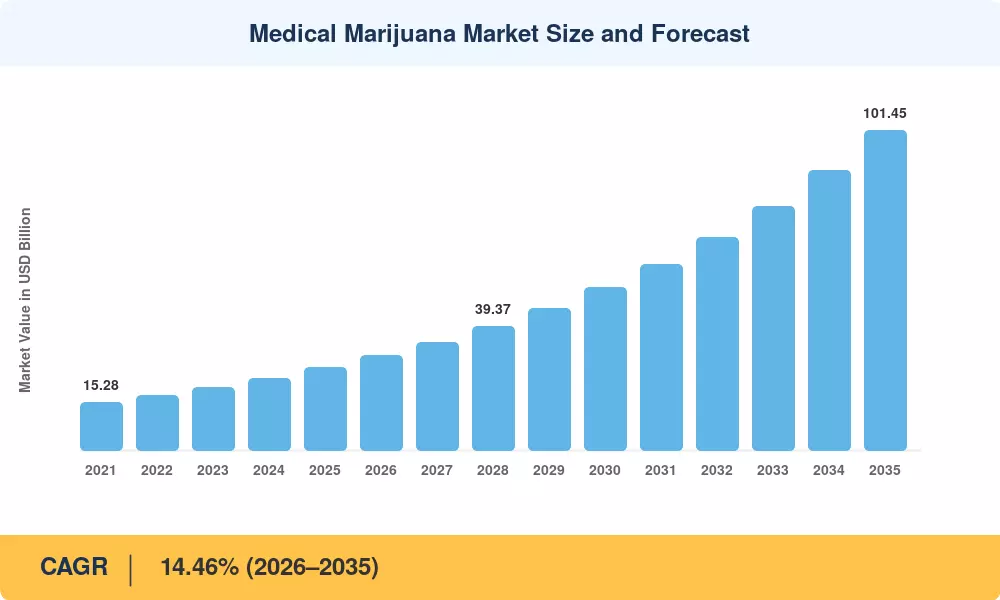

The Global Medical Marijuana Market size was valued at USD 26.24 Billion in 2025, and the market is projected to grow from USD 30.08 Billion in 2026 to USD 101.45 Billion by 2035, registering a CAGR of 14.46% during the forecast period 2026–2035. Two catalysts are accelerating this trajectory: the wave of evidence-based legislative reforms sweeping OECD nations, and the integration of cannabis-derived molecules into Phase 3 clinical pipelines targeting chronic pain and oncology indications. Institutional investor allocations to the sector exceeded USD 4.8 Billion globally in 2024, signaling a decisive shift from speculative venture bets to pharmaceutical-grade capital deployment.

A transformation is underway in how cannabis medicines move from cultivation to the patient. Legacy cottage-style grow operations are being replaced by controlled-environment vertical farms equipped with AI-driven phenotyping, automated nutrient dosing, and EU-GMP-certified extraction lines [3]. The U.S. Drug Enforcement Administration's rescheduling review, combined with Health Canada's expanded research-license framework and Germany's 2024 partial-legalization act, has opened cross-border clinical validation pathways that were unthinkable five years ago [4]. Pharmaceutical firms are now securing FDA orphan-drug designations for cannabinoid formulations, pulling the Medical Marijuana Market firmly into mainstream healthcare.

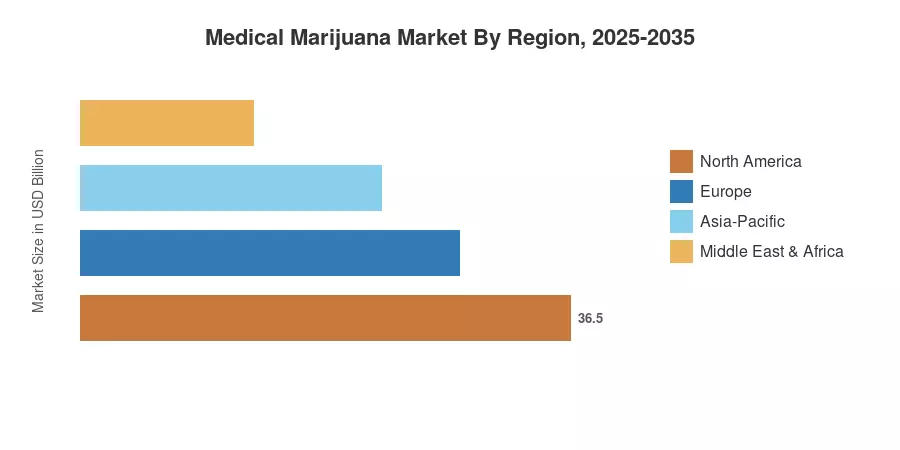

North America commands roughly 45.3% of the global Medical Marijuana Market revenue, anchored by mature dispensary networks across 40 U.S. states and Canada's federal licensing system. Asia-Pacific represents the fastest-growing region at a 17.5% CAGR through 2035, driven by regulatory pilots in Australia, Thailand, and South Korea [5]. Europe holds the second-largest share at approximately 24.8%, with Germany, Italy, and the United Kingdom leading prescriber adoption. As insurance reimbursement expands and batch-to-batch variability declines, the Medical Marijuana Market is poised for sustained double-digit growth well into the next decade.

Key Report Takeaways

• By Formulation Type

- Oil-based formulations held 45.2% of Medical Marijuana Market revenue in 2025, reflecting strong patient preference for precise dosing and sublingual delivery.

- Topical and transdermal gel formats are expanding at an 18.25% CAGR through 2035, supported by dermatology and localized pain applications.

• By Cannabinoid Composition & Route of Administration

- CBD-dominant products represented 46.1% of the Medical Marijuana Market in 2025, benefiting from broader regulatory acceptance and lower scheduling hurdles.

- Oral delivery captured 47.8% of revenue in 2025, while sublingual formats recorded a 17.4% CAGR through 2035.

• By Application & Distribution Channel

- Chronic pain accounted for 35.7% of the Medical Marijuana Market in 2025.

- Online distribution platforms exhibit an 18.8% CAGR to 2035, reflecting telehealth integration and direct-to-patient fulfillment models.

• By Region

- North America contributed 45.3% of the global Medical Marijuana Market revenue in 2025.

- Asia-Pacific is projected to grow at a 17.5% CAGR, making it the fastest-expanding regional market through 2035.

Medical Marijuana Market Size and Forecast (2021–2035)

Market sizing combines bottom-up revenue modeling from licensed cultivators, pharmaceutical distributors, and dispensary point-of-sale data with top-down cross-referencing against national health-authority prescription registries and trade databases. Historical figures (2021–2024) reflect audited company filings and government import-export records; the 2025 base year incorporates preliminary Q3 2025 data. Forecast projections apply a calibrated CAGR of 14.46% across 2026–2035, adjusted for anticipated regulatory inflection points and capacity additions.