Medical Recruitment Market Summary

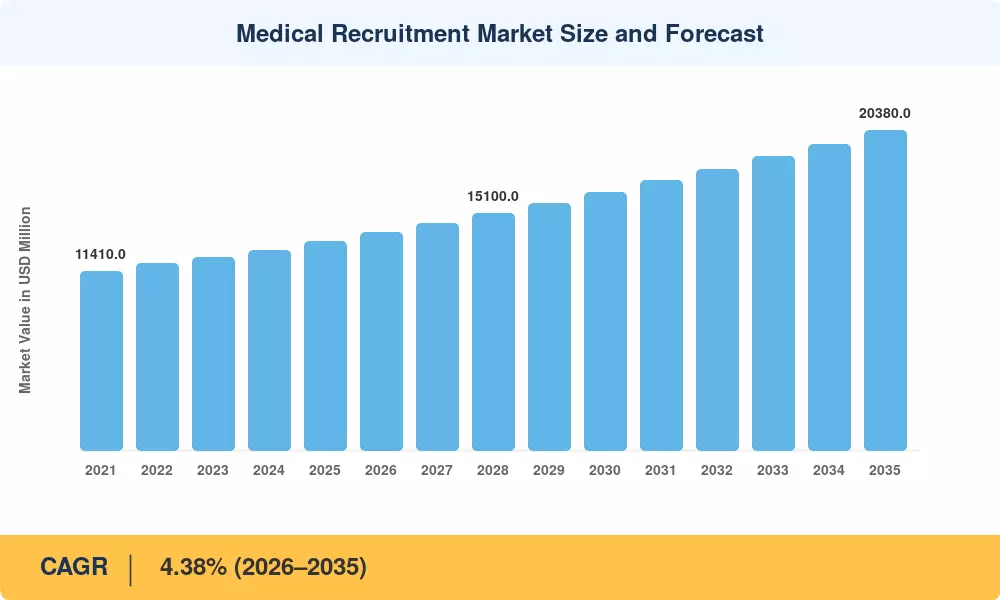

The global medical recruitment market stood at an estimated USD 13,280 Million in 2025 and is projected to reach USD 20,380 Million by 2035, advancing at a CAGR of 4.38% during the 2026–2035 forecast window. A chronic shortage of qualified healthcare professionals sits at the heart of this expansion — the Association of American Medical Colleges projects a shortfall of up to 124,000 physicians in the United States alone by 2034 [1]. Governments from India to the United Kingdom have responded with multi-billion-dollar hospital construction programs, each one intensifying the scramble for clinical talent. The medical recruitment market is translating these structural deficits into sustained commercial demand for staffing intermediaries and workforce management platforms.

Traditional recruitment workflows — paper-based credentialing, manual CV screening, and fragmented telephonic outreach — are giving way to cloud-native applicant tracking systems, AI-driven candidate matching engines, and blockchain-enabled credential verification. Healthcare staffing solutions providers invested over USD 1.2 billion in recruitment technology between 2022 and 2024, according to industry estimates [5]. This digital pivot is compressing time-to-fill from an average of 90 days to under 45 days for specialist physician roles.

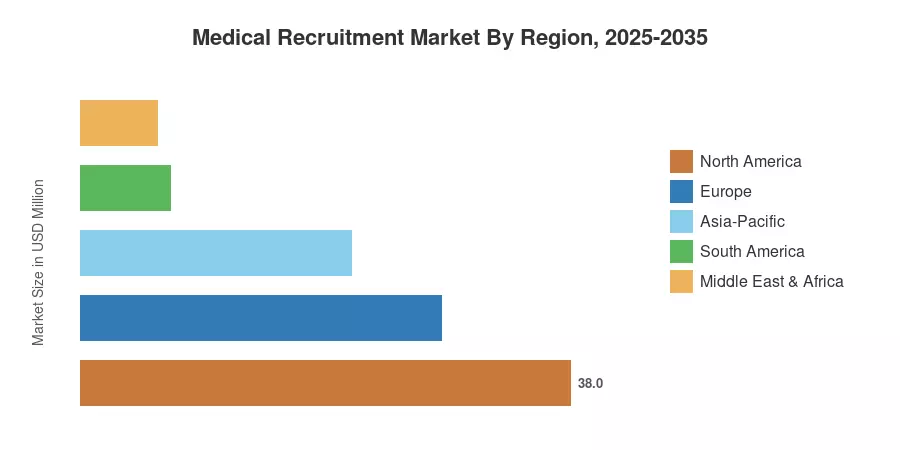

North America commands roughly 38% of the medical recruitment market, anchored by high physician compensation levels and an entrenched locum tenens culture. Asia-Pacific is the fastest-growing region, posting a projected CAGR of 5.62%, driven by India's Ayushman Bharat program and China's county-hospital modernization initiative. Europe holds the second-largest share at approximately 28%, supported by NHS workforce expansion in the United Kingdom and EU cross-border mobility directives. As workforce gaps widen across every continent, the medical recruitment market is positioned for a decade of compounding growth.

Key Report Takeaways

• By Services

- Recruitment Services capture the largest share of the medical recruitment market at 42%, reflecting persistent demand for contingency and retained search models.

- Managed Services represent the fastest-growing service segment with a projected CAGR of 5.15%, as health systems shift toward vendor-neutral programs.

• By Industry Verticals

- Nursing/Healthcare accounts for 38% of verticals, making it the dominant hiring category across the medical recruitment market.

- Pharmaceuticals and biotechnology are expected to reach USD 4,650 million by 2035, fueled by clinical trial staffing needs.

• By Region

- North America leads with USD 5,046 million in 2025 market value.

- Asia-Pacific registers the steepest growth trajectory at a 5.62% CAGR.

- Europe holds a 28% share, underpinned by cross-border recruitment frameworks.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on primary interviews with recruitment executives, healthcare HR directors, and government workforce planners, cross-validated against public filings, trade association surveys, and national labor-force statistics.