North America: Expanding domestic healthcare costs

The North America medical tourism market has shifted rapidly in responses to continuously high domestic healthcare costs, insurance gaps, and challenges to timely access. Mexico has emerged as a popular destination for Americans seeking lower-cost dental and cosmetic services, both to geographic proximity and government efforts to promote health travel.

- CDC healthcare utilization data shows over 60% of U.S. adults delay or avoid treatment due to high costs, reinforcing outbound medical tourism demand. GE Healthcare reports a 35% increase in cross-border imaging and diagnostic equipment usage, supporting international patient referrals. These factors strengthen Mexico and nearby destinations as preferred cost-effective treatment hubs for North American patients.

In contrast, the United States, despite being an appealing location for medical tourists, attracts inbound patients seeking highly specialized care in oncology, cardiology, and advanced surgeries, offered by world-class facilities. Anecdotal evidence suggests that a retired US couple flew to Thailand, Vietnam, Mexico, and the Caribbean for cancer treatment for a cost of USD 18,807, saving almost USD 100,000 compared to US prices and bypassing Medicare constraints. A US patient chose a USD 4,000 hysterectomy in Colombia over a USD 15,000 to USD 40,000 treatment in the US.

Europe: Production healthcare systems

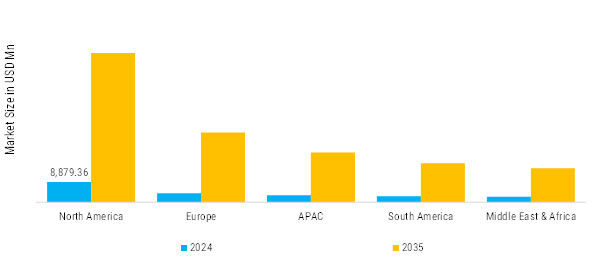

Europe medical tourism market accounted for USD 7,733.00 million in 2024 and is projected to grow at a CAGR of 15.88% during the forecast period. Europe is further segmented into the Germany, France, UK, Russia, Italy, Spain, and Rest of the Europe. Medical tourism has grown in prominence throughout Europe as patients seek more timely and cost-effective treatments in the midst of burdened home healthcare systems and long waiting lists.

- European Medicines Agency approvals indicate over 150+ advanced therapies authorized in the past decade, improving treatment availability across EU hospitals. Combined with healthcare system pressure, countries like Germany and Spain report waiting time reductions of up to 40% through cross-border patient programs, driving outbound and intra-Europe medical tourism for faster access to specialized procedures.

In the UK, post-COVID, the outflow began to accelerate. By 2022, around 350,000 UK residents traveled abroad for procedures (hip, knee replacements, cataracts, cardiology), up from around 248,000 in 2019, pushed mostly by overburdened NHS waiting times. Clinics in Lithuania, Poland, Croatia, and France are increasingly catering to these patients, providing faster access at reduced costs. A Highland patient's hip replacement in Poland, for instance, cost about half as much as private care in the UK.

Asia Pacific: Rising healthcare expenses

The Asia-Pacific medical tourism market has been strongly influenced by rising healthcare expenses in Western countries, the development of technologically advanced medical infrastructure throughout Asia, and increased consumer awareness of cross-border treatment choices. Since 2019, Thailand, India, Malaysia, and South Korea have attracted millions of patients each year seeking high-quality, low-cost medical operations ranging from cardiac surgery and orthopedics to cosmetic enhancements and fertility treatments.

Thailand's combination of refined wellness with therapeutic services has made it a top destination, particularly for cosmetic and gender-affirming procedures.

- Malaysia, which had over 1.22 million medical tourists in 2019, has emerged as a destination for cardiology, fertility, cancer, and dental treatments, with specialized patient centers and regional offices. Thailand, a long-standing leader in the region, continues to draw international patients for cosmetic, wellness, and regenerative therapies, supported by world-class facilities and tourism integration.

Rest of the World: Growing strategic infrastructure investments

The Rest of the World medical tourism market has seen significant transformation, owing to a combination of strategic infrastructure investments, government initiatives, and growing patient flows. In the Middle East, the United Arab Emirates, particularly Dubai and Abu Dhabi, have established themselves as a leading worldwide healthcare destination.

- In 2023, Dubai alone attracted roughly 691,000 medical tourists, who spent approximately AED 1 billion (nearly USD 280 million) on medical treatments. Its popularity arises from a seamless blend of high-end medical facilities, short treatment wait times, opulent recuperation alternatives, and integrated tourist, with platforms such as DXH offering one-stop access to consultations, accommodation, visas, and tourism packages.