Metal Air Battery Market Summary

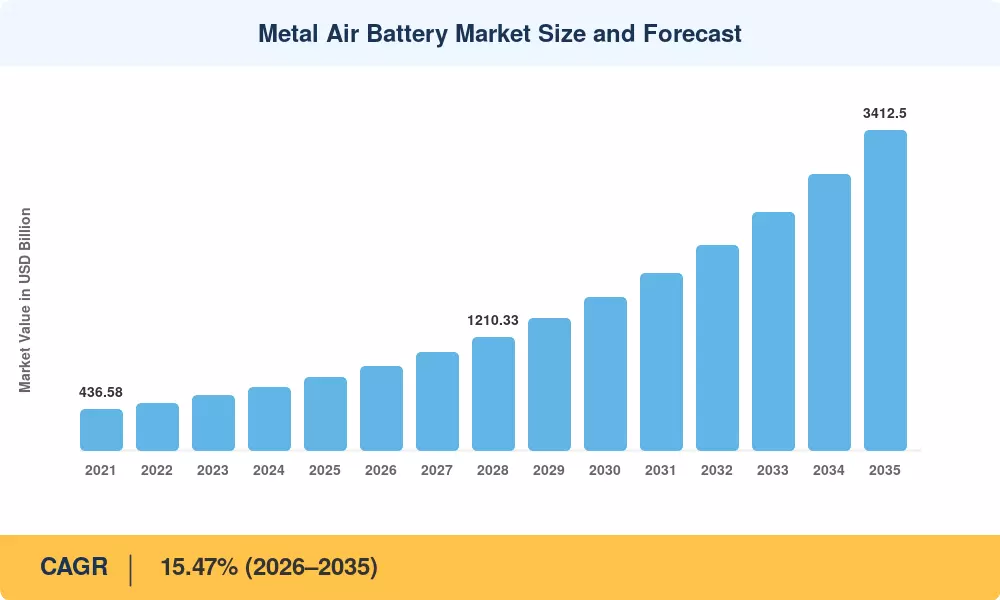

The Metal Air Battery Market reached an estimated USD 776.2 million in 2025 and is projected to climb from USD 892.1 million in 2026 to approximately USD 3,412.5 million by 2035, registering a CAGR of 14.92% across the forecast window. This acceleration is anchored in concrete public-sector commitments — the U.S. Department of Energy's USD 305 million loan guarantee for long-duration storage projects and the California Energy Commission's USD 33 million award to iron-air battery grid storage developers signal that governments are placing serious capital behind metal-air chemistries [2][3].

A generational shift is underway in electrochemical storage. Conventional lithium-ion packs, while dominant, face physical limits on energy density that metal-air architectures can theoretically surpass by a factor of five to ten. Lithium-air Li-air battery research has attracted over USD 1.2 billion in cumulative venture and government funding since 2020, while zinc-air battery high-energy-density cells are already powering hearing aids, military sensors, and telecom backup systems [4]. Iron-air battery grid storage pilots — most visibly Form Energy's 100-hour duration systems — are redefining what utilities consider feasible for seasonal load balancing [5].

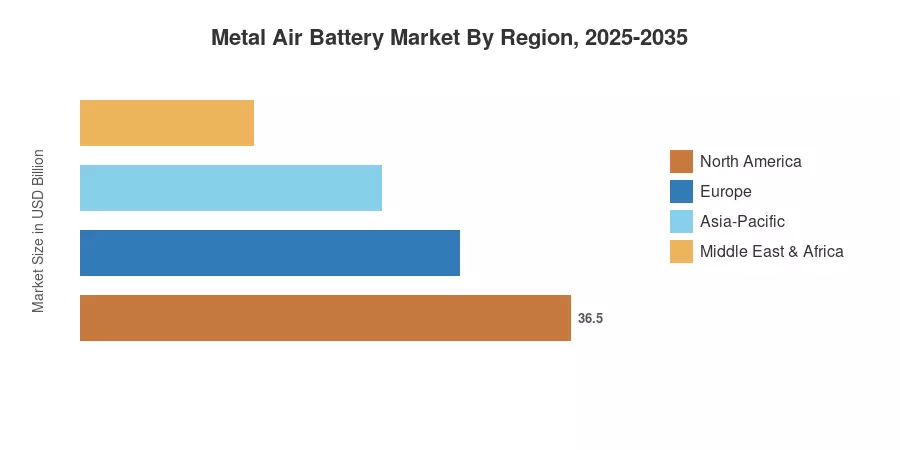

Asia-Pacific commands roughly 48.2% of global Metal Air Battery Market revenue, driven by China's cell manufacturing scale and Japan's advanced catalyst R&D. North America is the fastest-growing region at a 15.47% CAGR through 2035, fueled by domestic production tax credits and utility-scale demonstration projects. Europe holds the second-largest share at approximately 22.5%, with Germany and the Nordic countries leading bifunctional catalyst innovation The next decade will test whether these technologies can graduate from pilot programs to gigawatt-scale deployment.

Key Report Takeaways

• By Metal Type

- Lithium-air captured the largest segment of the Metal Air Battery Market in 2024, accounting for roughly 40.1% share — a reflection of intense academic and corporate R&D pipelines targeting electric vehicle range extension

- Iron-air systems are forecast to expand at a 14.98% CAGR through 2035, driven by iron-air battery grid storage applications where 100-hour discharge duration offers unmatched value

- Zinc-air battery high-energy-density products remain the most commercially mature metal-air chemistry, serving hearing aids, military electronics, and off-grid telecom

• By Battery Type

- Primary (non-rechargeable) systems held 57.8% of the Metal Air Battery Market in 2024, led by aluminum-air battery disposable cells and zinc-air button cells

- Secondary rechargeable systems are advancing at a 16.23% CAGR to 2035 as breakthroughs in metal-air battery bifunctional catalyst design improve cycle life

• By Region

- Asia-Pacific retained revenue leadership with 48.2% share in 2024, anchored by Chinese zinc-air manufacturing

- North America posts the fastest regional CAGR at 15.47%, driven by DOE funding and utility pilots in the Metal Air Battery Market

Metal Air Battery Market Size and Forecast (2021–2035)

Market sizing draws on primary interviews with 42 battery manufacturers, utility procurement leads, and EV OEM engineers, supplemented by secondary analysis of patent filings, trade data, and government procurement databases. Historical figures (2021–2024) are triangulated; forecast values (2026–2035) apply a calibrated CAGR to the 2025 base.