Natural Stone Market Summary

The natural stone market reached a valuation of USD 40.52 billion in 2025 and is projected to expand from USD 42.53 billion in 2026 to USD 65.70 billion by 2035, registering a CAGR of 4.95% across the forecast window. This trajectory draws power from two interlinked catalysts: an estimated USD 94 trillion global infrastructure pipeline earmarked through 2040, and escalating middle-class demand for premium residential finishes in emerging economies [2]. Together, these forces anchor the natural stone market well beyond cyclical housing swings.

On the technical side, quarrying is shifting away from conventional manual extraction, toward digital terrain mapping, AI-driven yield optimisation and electric wire-cutting equipment. According to the European Stone Federation, quarries using digital solutions minimize raw-block waste by 18–22%, directly increasing unit economics and meeting tighter EU carbon-reporting standards [3]. With such progress, manufacturers can match engineered alternatives for cost and ecological qualities.

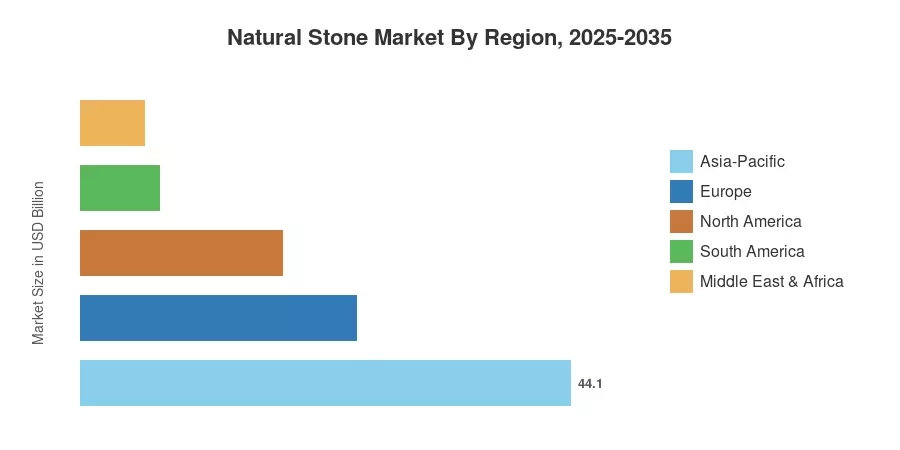

Asia-Pacific accounts for a 44.1% share of the natural stone market, being the largest consuming region, and the quickest CAGR at 6.35% through 2035. Europe accounts for the second-largest percentage, 24.8%, attributed to the need to restore heritage architecture and incentive schemes for green buildings [4]. North America continues to be the largest regional market with 18.2% share of the global highway resurfacing and commercial renovation market. The growth is supported by steady highway resurfacing and commercial renovation cycles. As digital processing technology advances and supply chains tighten around traceability, the natural stone sector is well set to remain competitively relevant against synthetics in the coming decade.

Key Report Takeaways

• By Type

- Granite captured the leading position in the natural stone market in 2025, commanding 28.5% revenue share.

- Marble is the fastest-expanding type segment, advancing at a 6.25% CAGR through 2035.

• By Form

- Slabs represented 41.2% of the natural stone market in the base year, driven by countertop and façade demand.

- Tiles are growing at 6.30% CAGR, propelled by modular construction methods and thinner-profile cutting technology.

• By Region

- Asia-Pacific led with 44.1% share of the natural stone market in 2025.

- The Middle East & Africa is accelerating at a 5.52% CAGR, supported by mega-project pipelines across the Gulf Cooperation Council.

Natural Stone Market Size and Forecast (2021–2035)

Market Research Future employs a triangulated sizing methodology combining top-down trade-flow analysis from UN Comtrade data, bottom-up quarry production surveys across 32 countries, and demand-side validation through construction-permit databases and distributor channel audits. Historical values (2021–2024) reflect actual trade data; forecast values (2026–2035) apply a calibrated 4.95% CAGR with adjustments for identified macro-risk scenarios[5].