Nickel Cadmium Battery Market Summary

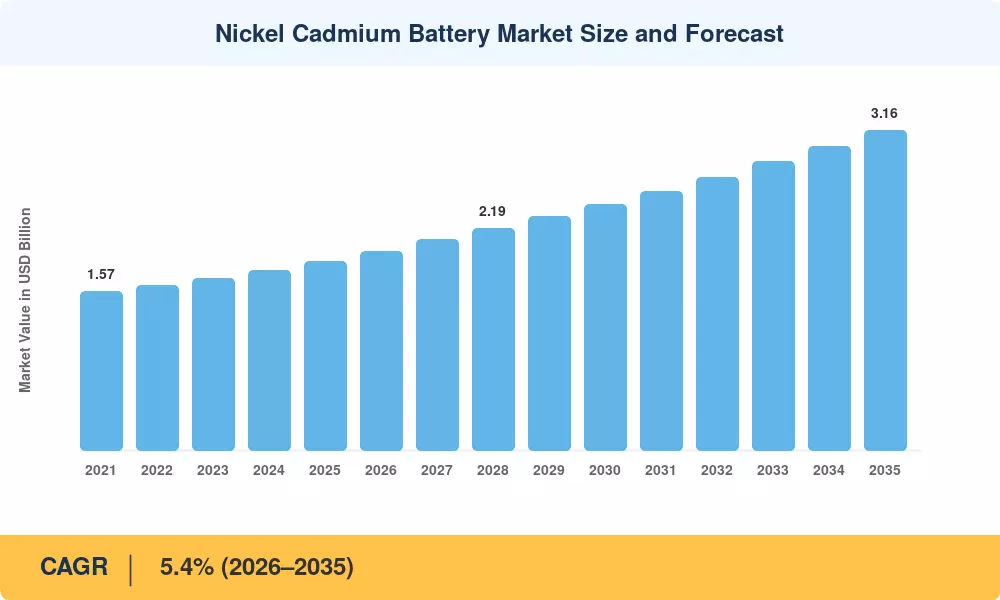

The global Nickel Cadmium Battery Market was valued at USD 1.87 billion in 2025 and is projected to reach USD 3.16 billion by 2035, expanding at a 5.4% CAGR during the 2026–2035 forecast window. Sustained demand from industrial standby power installations, aviation starter systems, and defense electronics underpins this trajectory. Government mandates requiring certified backup energy for critical infrastructure—including the U.S. FAA's Technical Standard Order C173 for aircraft batteries and the EU Battery Regulation (2023/1542) introducing mandatory recycling quotas—continue to channel procurement budgets toward nickel-cadmium chemistry [1][2].

While increasing lithium-ion degradation has squeezed consumer-grade addressable quantities, nickel-cadmium cells still have unique benefits in extreme-temperature conditions (–40 °C to +70 °C) and deep-discharge cycling applications. Combined tenders in Europe and India for vented nickel-cadmium systems were above USD 340 million in 2023–2024, highlighting the chemistry’s staying power in safety-certified sectors [3][4], such as railway signaling networks.

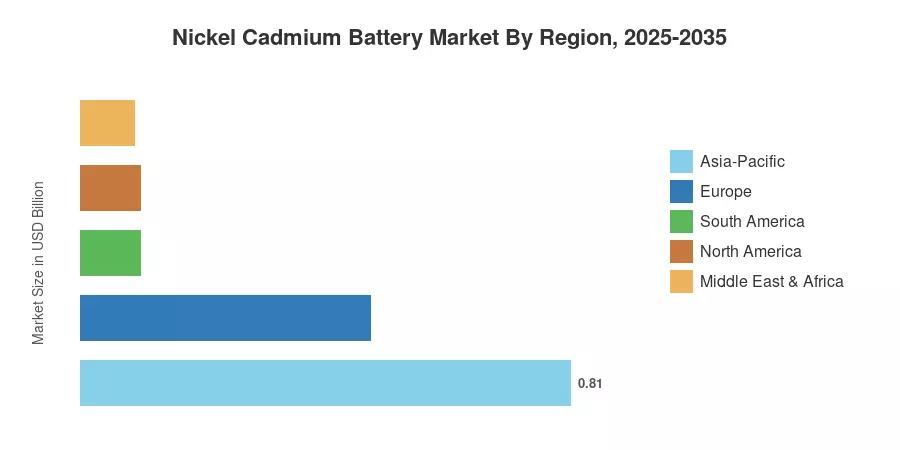

The Asia-Pacific nickel-cadmium battery market accounted for 43.4% of the market in 2024, with Chinese manufacturing and the Indian railways’ electrification projects adding to the size of the market. Aerospace OEM clusters in France and Germany led Europe, which accounted for 25.8% and ranked second. Defense modernization spending is anticipated to fuel North America’s CAGR to 5.2% through 2035. How manufacturers balance the cost of complying with recycling regulations with margins in an increasingly restrictive regulatory environment will help determine the next decade.

Key Report Takeaways

• By Battery Type

- Vented/flooded configurations held a 38.2% share of the nickel-cadmium battery market in 2024, anchored by industrial and rail installations.

- Sub-C and specialty formats are forecast to grow at a 6.4% CAGR through 2035, the fastest among all battery types.

• By Application

- Military and defense applications are poised to expand at a 6.6% CAGR to 2035, driven by NATO and Indo-Pacific procurement cycles.

- Industrial installations retained a 48.3% share of the nickel-cadmium battery market in 2024.

• By Geography

- Asia-Pacific generated a 43.4% revenue share in 2024 and is projected to advance at a 6.3% CAGR through 2035.

- North America is set to register a 5.2% CAGR, buoyed by FAA-certified aviation battery replacements and grid-edge deployments.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) sizing approach includes primary interviews with battery OEMs, Tier-1 component suppliers and institutional procurement agencies across 22 countries. Historical data (2021-2024) is based on customs trade statistics, firm annual reports, and verified cargo volumes; the forecast period (2026-2035) is based on scenario-based econometric modeling calibrated against infrastructure investment pipelines and deadlines for regulation adoption.