Non Emergency Medical Transportation Market Summary

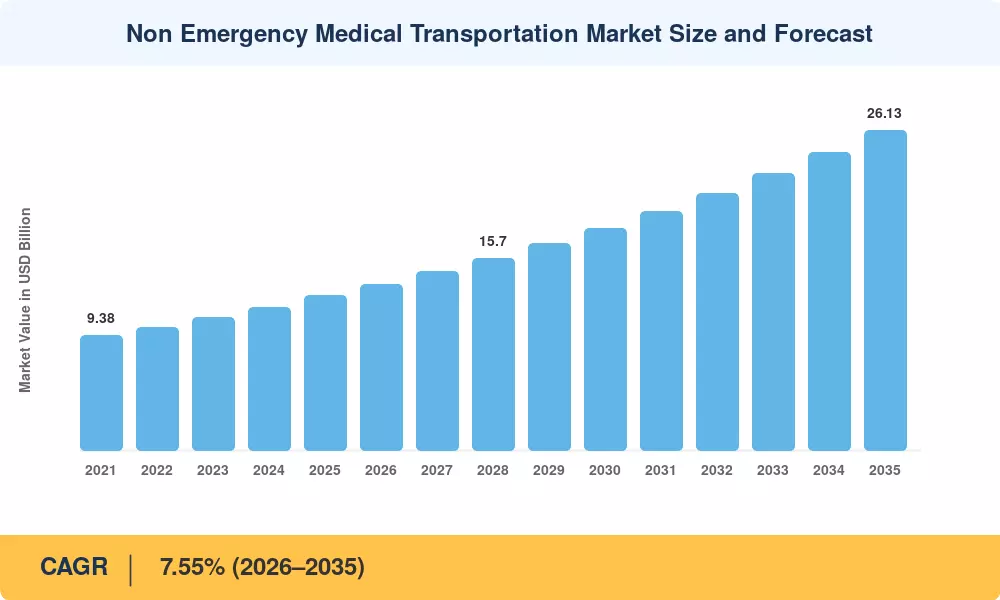

The Non-Emergency Medical Transportation Market was valued at USD 12.62 billion in the base year 2025 and is projected to reach USD 13.57 billion in 2026 before climbing to USD 26.13 billion by 2035, registering a compound annual growth rate of 7.55% during the 2026–2035 forecast window. Two catalysts are doing the heavy lifting: the expansion of Medicaid managed-care contracts that now tie reimbursement to verified ride completion, and the U.S. Centers for Medicare & Medicaid Services' 2025 Final Rule mandating real-time ride-tracking for all managed-care plan transportation benefits [1]. Together, these policy shifts are converting a historically fragmented, paper-based sector into a data-driven logistics discipline.

Legacy call-center dispatch is giving way to cloud-based platforms that pair predictive routing with GPS-verified pickup and drop-off timestamps. The Federal Transit Administration's Low or No Emission Vehicle Program allocated USD 1.7 billion in fiscal-year 2025 grants, with a growing share directed toward paratransit and medical-ride operators replacing diesel fleets with battery-electric wheelchair-accessible vans [2]. This electrification wave is trimming per-trip fuel costs by an estimated 35–40% while helping providers comply with state-level zero-emission fleet mandates now active in California, New York, and Washington.

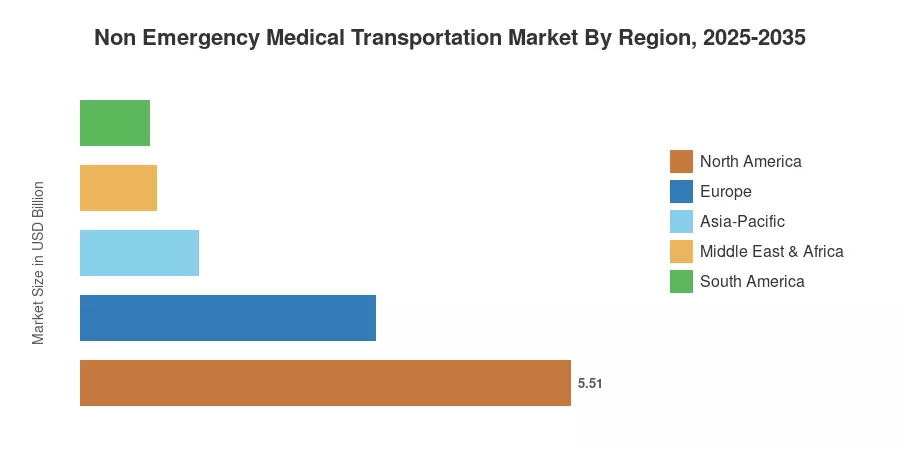

North America commands roughly 43.7% of the global Non-Emergency Medical Transportation Market revenue, driven by the sheer scale of Medicaid-funded rides—an estimated 104 million trips annually across the United States alone [3]. Asia-Pacific emerges as the fastest-growing region at a projected 10.52% CAGR through 2035, propelled by universal-health-coverage rollouts in India and Indonesia. Europe holds the second-largest share, anchored by the United Kingdom's NHS patient-transport contracts and Germany's statutory-health-insurance mandate. The next decade will increasingly reward operators that blend fleet electrification with AI-powered scheduling and value-based performance reporting.

Key Report Takeaways

• By Vehicle Type

- Wheelchair-enabled vans captured 46.2% of the Non-Emergency Medical Transportation Market in 2025, underpinned by ADA compliance requirements and aging population demographics.

- Hybrid and electric vans are forecast to expand at a 10.15% CAGR through 2035 as FTA electrification grants accelerate fleet turnover.

• By Payment Type & Application

- Medicaid constituted 55.6% of the Non-Emergency Medical Transportation Market in 2025, reflecting state-level managed-care expansions across 42 U.S. states.

- Mental-health transportation appointments record the highest application-level CAGR at 10.28% through 2035, driven by broadened behavioral-health coverage.

- Dialysis transportation represented USD 3.95 billion in 2025, making it the single largest application segment.

• By Region

- North America led the Non-Emergency Medical Transportation Market with 43.7% revenue share in 2025.

- Asia-Pacific is poised to grow at a 10.52% CAGR, the fastest among all regions, through 2035.

- Europe accounted for 26.3% of global revenue in 2025, anchored by NHS and statutory-insurance mandates.

Non-Emergency Medical Transportation Market Size and Forecast (2021–2035)

Market Research Future's proprietary sizing model integrates bottom-up provider-revenue aggregation with top-down payer-claims analysis across 38 countries. Historical figures (2021–2024) rely on audited financial disclosures, Medicaid Transportation Management reports, and fleet-census data, while forecast projections (2026–2035) incorporate regression-based demand modeling, demographic aging indices, and announced policy pipelines.