Passive Authentication Market Summary

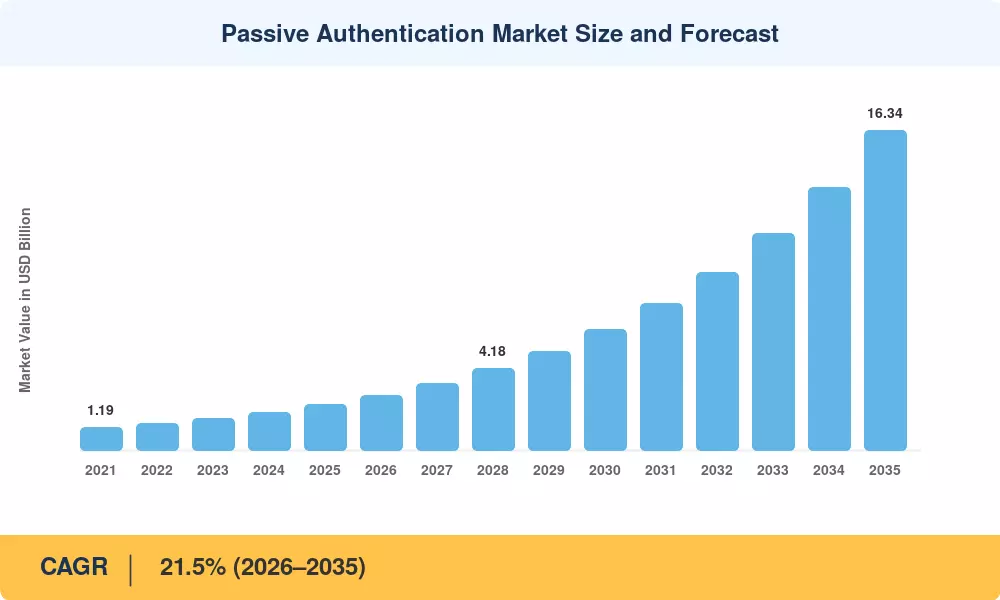

The Passive Authentication Market was valued at USD 2.33 billion in 2025 and is projected to reach USD 2.83 billion in 2026 before climbing to USD 16.34 billion by 2035, advancing at a 21.5% CAGR during 2026–2035. This trajectory is driven by an acute rise in AI-powered identity fraud — synthetic deepfakes increased 3,000% between 2022 and 2024 according to industry trackers [1] — and by regulatory mandates compelling financial institutions and healthcare providers to embed stronger, non-intrusive verification layers into digital workflows. The Passive Authentication Market sits at the intersection of cybersecurity urgency and consumer experience design.

A fundamental technology shift underpins this growth. Legacy challenge-response models — passwords, one-time PINs, knowledge-based questions — are giving way to ambient signal analysis that evaluates keystroke cadence, device posture, geolocation patterns, and session behavior in real time. Europe's PSD2 Strong Customer Authentication requirements and Asia's evolving biometric mandates have pulled these capabilities from niche pilots into mainstream procurement [2]. Global enterprise spending on identity-centric security surpassed USD 28 billion in 2024, and a rising share of that budget now flows toward passive verification architectures [3].

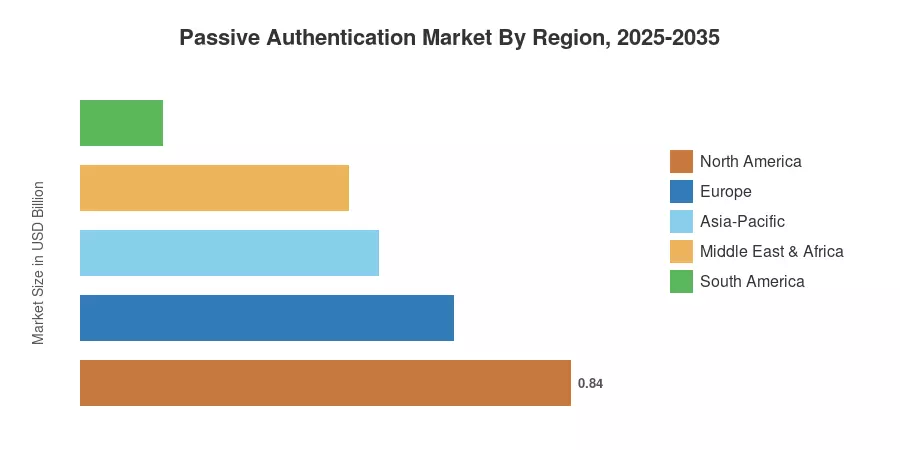

North America held 36.2% of the Passive Authentication Market in 2025, anchored by early zero-trust adoption across U.S. financial services and federal agencies. Europe captured the second-largest share at approximately 27.5%, propelled by PSD2 and eIDAS 2.0 compliance cycles. Asia-Pacific is tracking the fastest regional CAGR of 21.9% through 2035, fueled by India's Digital Personal Data Protection Act and China's expanding mobile-payment ecosystem. As digital identity frameworks mature globally, the Passive Authentication Market is poised to become a foundational layer of enterprise security architecture.

Key Report Takeaways

• By Component

- Solutions represented 76.0% of the Passive Authentication Market in 2025, reflecting strong demand for integrated software platforms.

- Services are projected to expand at a 22.2% CAGR through 2035, driven by managed detection and deployment consulting engagements.

• By Authentication Technology

- Behavioral analytics captured 34.3% of total revenue in 2025, remaining the single largest technology segment.

- Multi-modal authentication is forecast to grow at a 22.7% CAGR, reflecting enterprise preference for layered signal fusion.

• By End-User Industry

- BFSI accounted for 44.3% of the Passive Authentication Market in 2025, led by fraud-prevention mandates.

- Healthcare and life sciences are forecast to grow at a 21.8% CAGR, as patient-portal security regulations tighten.

• By Region

- North America held the dominant share of the Passive Authentication Market, driven by federal zero-trust mandates.

- Asia-Pacific is expanding at a 21.9% CAGR, the fastest among all regions, propelled by digital payment proliferation.

Market Size and Forecast (2021–2035)

Market Research Future derived historical estimates from verified vendor revenues, regulatory filings, and third-party spending surveys across identity and access management sectors. Forecast projections apply a compound growth model calibrated to macroeconomic indicators, regulatory pipeline analysis, and end-user adoption curves across 42 countries.