Pediatric Vaccines Market Summary

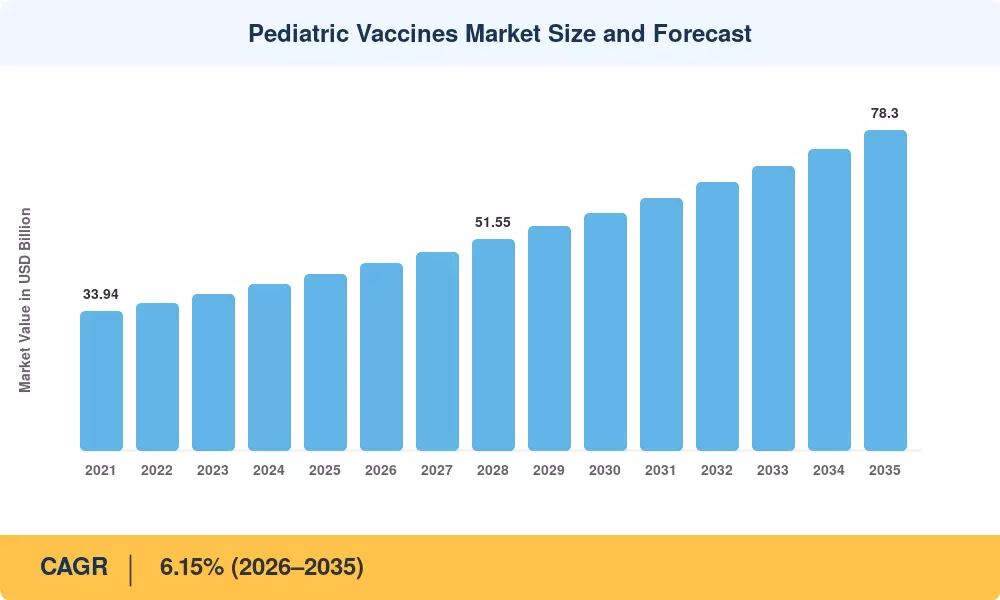

The Global Pediatric Vaccines Market size was valued at USD 43.10 Billion in 2025, and the market is projected to grow from USD 45.75 Billion in 2026 to USD 78.30 Billion by 2035, registering a CAGR of 6.15% during the forecast period 2026–2035. Two policy forces anchor this trajectory: the United States Vaccines for Children Program, which covers approximately 50% of all American children, and a USD 5.4 billion federal investment through Project NextGen aimed at accelerating next-generation prophylactic platforms [1][2]. These public commitments underpin both procurement volumes and manufacturer R&D confidence across the Pediatric Vaccines Market.

A technology shift is redefining how pediatric immunizations reach children. Legacy single-antigen regimens are steadily giving way to higher-valent conjugate and recombinant platforms that reduce injection burden while broadening pathogen coverage. Manufacturers have committed over USD 3.8 billion in capital expenditure since 2022 to scale mRNA production lines originally built for COVID-19 toward RSV, influenza, and combination pediatric candidates [3]. Digital cold-chain automation and blockchain-enabled traceability are also cutting the roughly one-in-three global vaccine wastage rate, protecting billions in annual value [4].

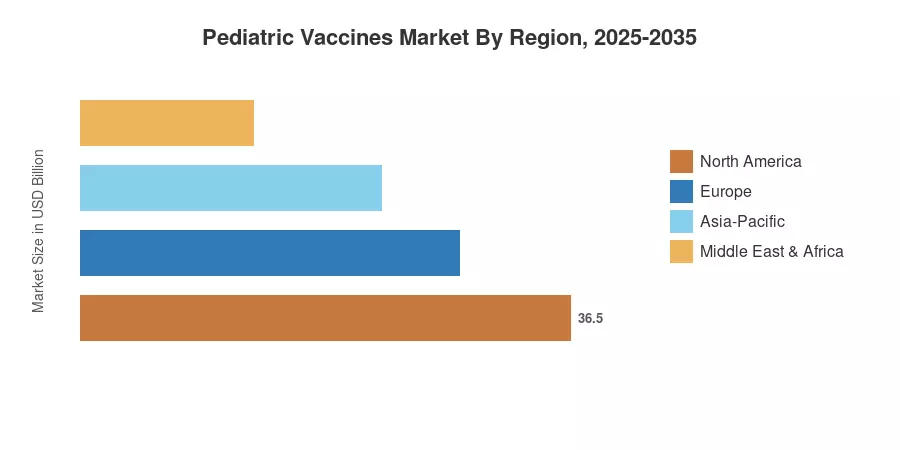

From a regional standpoint, North America commands the largest share of the Pediatric Vaccines Market at approximately 41.6% of 2025 revenue, driven by robust insurance reimbursement and mandatory school-entry schedules. Asia-Pacific is the fastest-growing region, posting a projected CAGR of 7.01% through 2035, fueled by Gavi-supported national rollouts in India and Southeast Asia. Europe holds the second-largest share at roughly 27.0%, anchored by unified EMA regulatory pathways and strong public-health procurement across Germany, France, and the Nordic states [5][6]. The decade ahead will be shaped by how quickly next-generation platforms scale into routine schedules worldwide.

Key Report Takeaways

• By Vaccine Valence

- Multivalent products captured approximately 57.1% of the global Pediatric Vaccines Market revenue in 2025, reflecting the clinical and logistical advantages of combination schedules.

- Monovalent vaccines are projected to post the fastest segment CAGR of 6.89% through 2035 as new single-antigen candidates for RSV and emerging pathogens enter routine use.

• By Technology Platform

- Conjugate vaccines held the leading platform share of 38.4% in 2025, underpinned by pneumococcal and meningococcal demand across all age cohorts.

- The recombinant segment is set to expand at a 6.84% CAGR to 2035, driven by next-generation protein-subunit and virus-like-particle candidates.

• By Indication

- Pneumococcal formulations accounted for roughly 35.5% of the Pediatric Vaccines Market revenue in 2025, reinforced by WHO-recommended universal infant schedules.

- Influenza vaccines exhibit the highest indication-level CAGR at 6.74% through 2035, supported by seasonal boosters and cell-culture manufacturing advances.

• By Distribution Channel

- The public sector commanded 61.3% of global Pediatric Vaccines Market sales in 2025 through centralized procurement mechanisms such as UNICEF Supply Division and Gavi.

- Private-channel distribution is forecast to grow at a 6.70% CAGR as middle-income families increasingly access pediatric immunizations through private clinics.

• By Region

- North America captured 41.6% of the 2025 Pediatric Vaccines Market revenue, supported by comprehensive insurance mandates and CDC-recommended schedules.

- Asia-Pacific is on track for the leading regional CAGR of 7.01% to 2035, as India, China, and ASEAN nations expand universal immunization infrastructure.

Pediatric Vaccines Market Size and Forecast (2021–2035)

Market Research Future employs a hybrid bottom-up and top-down methodology, triangulating manufacturer revenue disclosures, public procurement records from WHO/UNICEF, regulatory approval databases, and proprietary primary interviews with immunization program directors across 28 countries. Historical figures (2021–2024) draw on audited annual reports and national health expenditure datasets; forecast estimates (2026–2035) apply a calibrated CAGR anchored to validated 2025 base-year revenue [1][7].