Segmentation Quick Reference

| Dimension | Sub-Segments | Dominant Segment | Fastest Growing Segment |

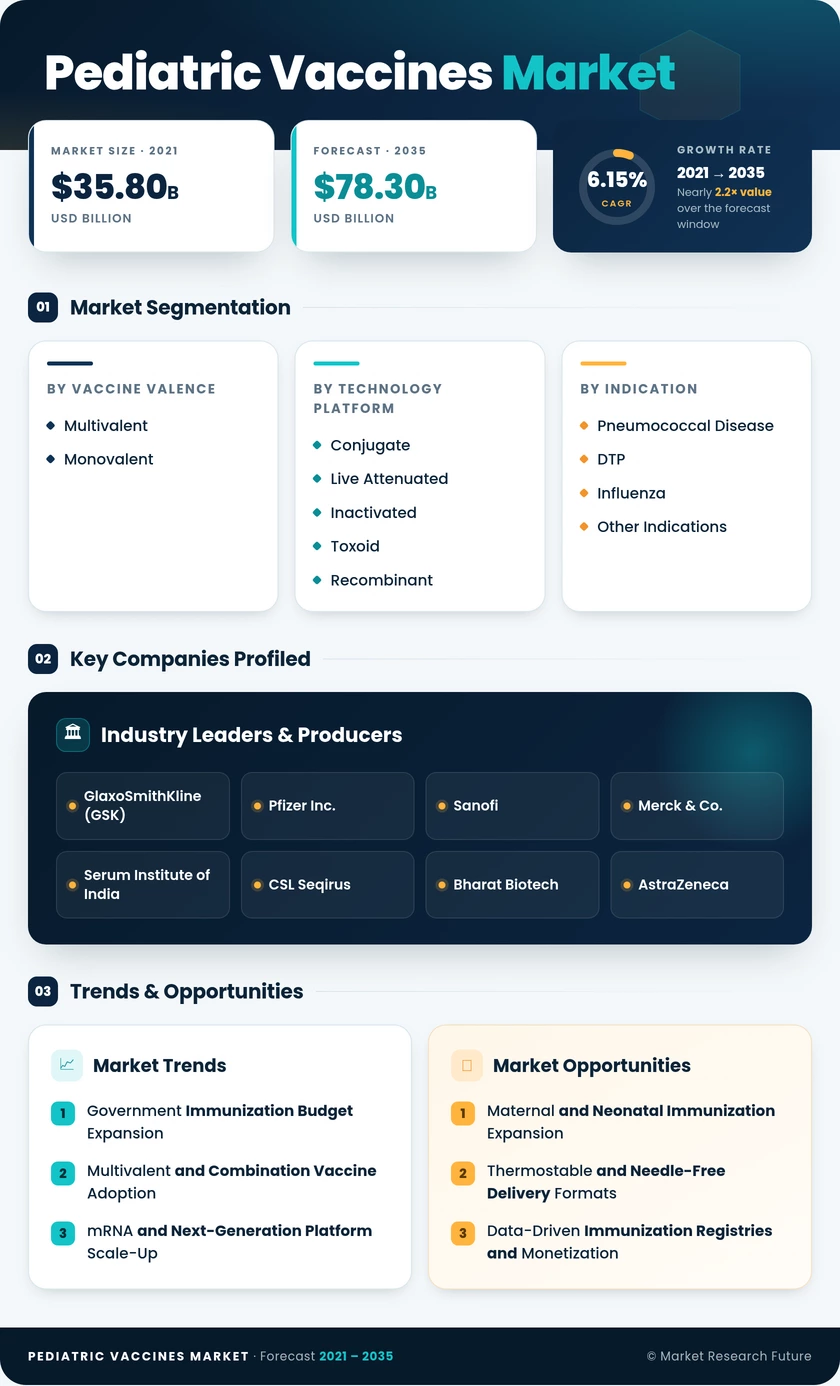

| Vaccine Valence | Multivalent, Monovalent | Multivalent (57.1% share, 2025) | Monovalent (6.89% CAGR) |

| Pediatric Vaccines Market Platform | Conjugate, Live Attenuated, Inactivated, Toxoid, Recombinant | Conjugate (38.4% share, 2025) | Recombinant (6.84% CAGR) |

| Indication | Pneumococcal Disease, DTP, Influenza, Other Indications | Pneumococcal Disease (35.5% share, 2025) | Influenza (6.74% CAGR) |

| Distribution Channel | Public, Private | Public (61.3% share, 2025) | Private (6.70% CAGR) |

| Region | North America, Europe, Asia-Pacific, South America, Middle East & Africa | North America (41.6% share, 2025) | Asia-Pacific (7.01% CAGR) |

Market Segmentation Overview

By Vaccine Valence

| Sub-Segment | Key Trend |

| Multivalent | Pentavalent and hexavalent combinations becoming standard in 120+ national schedules; reduces injection burden and improve completion rates |

| Monovalent | New single-antigen candidates for RSV, seasonal influenza, and novel pathogens entering routine use; fastest-growing valence segment |

Multivalent formulations continue to dominate procurement volumes as WHO-recommended combination schedules expand across both high-income and Gavi-eligible countries. Monovalent vaccines are regaining growth momentum as pathogen-specific candidates — particularly for respiratory syncytial virus — fill previously unaddressed gaps in pediatric immunization calendars.

By Pediatric Vaccines Market Platform

| Sub-Segment | Key Trend |

| Conjugate | PCV13/PCV15/PCV20 and meningococcal conjugates anchor demand; moving toward higher-valent formulations |

| Live Attenuated | OPV, MMR, and varicella schedules sustain volumes; gradual IPV transition reducing OPV share |

| Inactivated | IPV mandate driving substitution from OPV; hepatitis A expansion in new markets |

| Toxoid | DT/Td boosters maintain steady demand; limited pipeline innovation |

| Recombinant | Protein-subunit and VLP platforms advancing rapidly; key growth frontier for next-generation candidates |

Conjugate technology remains the revenue leader, driven by the entrenched position of pneumococcal conjugate vaccines in infant schedules worldwide. Recombinant platforms represent the highest-growth frontier, with multiple protein-subunit and virus-like-particle candidates progressing through late-stage clinical development for pediatric respiratory and gastrointestinal indications.

By Indication

| Sub-Segment | Key Trend |

| Pneumococcal Disease | PCV20 expansion increasing per-dose value; competitive dynamics between Pfizer and Merck intensifying |

| DTP (Diphtheria-Tetanus-Pertussis) | Foundational schedule antigen with universal coverage; stable but mature growth profile |

| Influenza | Seasonal pediatric flu vaccination transitioning from recommendation to routine; cell-culture manufacturing improving strain match |

| Other Indications | Rotavirus, hepatitis B, meningococcal, MMR, and HPV collectively comprise a diverse and growing segment |

Pneumococcal vaccines command the largest indication share, reflecting both universal schedule inclusion and the premium pricing of higher-valent conjugate formulations. Influenza vaccines represent the fastest-growing indication as an increasing number of countries incorporate seasonal pediatric flu shots into mandatory or strongly recommended childhood schedules.

By Distribution Channel

| Sub-Segment | Key Trend |

| Public | Centralized procurement through UNICEF, Gavi, and national health agencies; dominant volume channel |

| Private | Rising middle-class demand in Asia-Pacific and South America; premium combination vaccines driving revenue growth |

Public-sector procurement dominates global pediatric vaccine distribution, with UNICEF Supply Division and national immunization programs serving as the primary purchasing channels for the majority of the world's children. Private-channel growth is accelerating as expanding middle-class populations in emerging economies increasingly access pediatric vaccinations through private clinics, hospital networks, and pharmacy chains.