Peripheral artery disease Market Summary

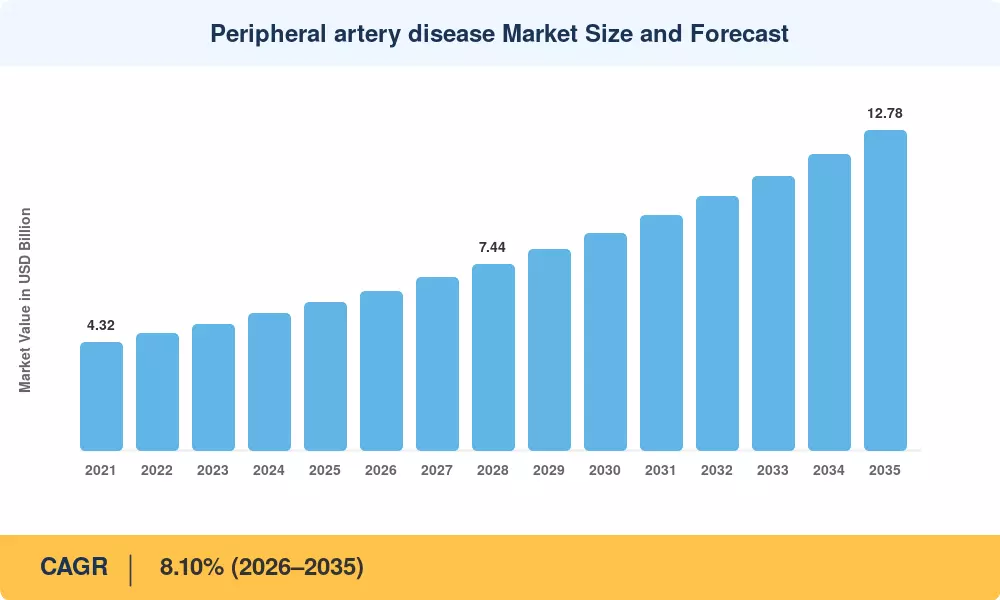

The Peripheral Artery Disease Market reached a valuation of USD 5.90 billion in 2025 and is projected to grow from USD 6.34 billion in 2026 to USD 12.78 billion by 2035, expanding at a CAGR of 8.10% during the forecast period. Rising global diabetes prevalence — the International Diabetes Federation counted over 537 million adults living with diabetes in 2024 [1] — and the parallel expansion of value-based reimbursement models in major health systems are the two strongest structural catalysts pushing procedure volumes upward. The Peripheral Artery Disease Market is now at a transition point where payer incentives and clinical evidence are converging to accelerate device and drug adoption simultaneously.

Technology is changing the delivery of care. Older open-surgical revascularization techniques are slowly being replaced by catheter-based endovascular interventions — drug-coated balloons, atherectomy devices and bioresorbable stents — performed in outpatient ambulatory settings. In 2024 alone, the FDA approved 15 new peripheral vascular devices[2]. In 2023–2024, hospital capital expenditures on hybrid catheter laboratories exceeded USD 2.3 billion across the United States and Western Europe[3]. Stryker's $4.9 billion purchase of Inari Medical is emblematic of the substantial investments device makers are making into next-generation thrombectomy and revascularization platforms.

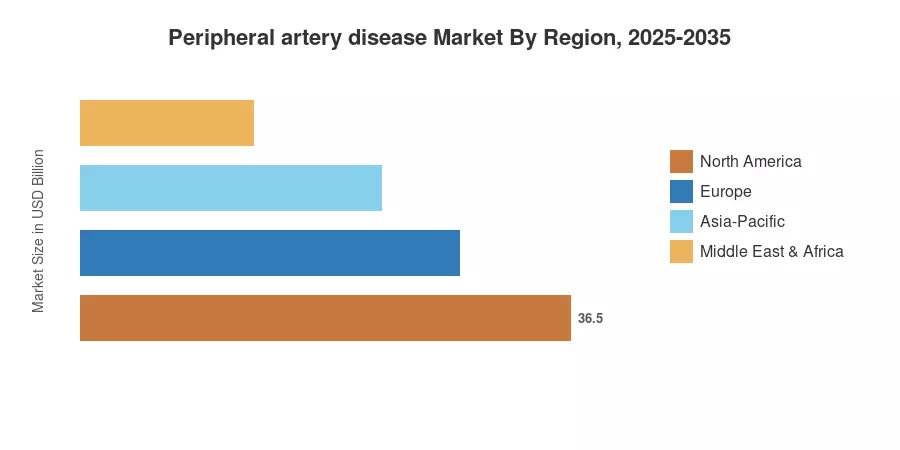

North America accounts for around 43.7% of the Peripheral Artery Disease Market, owing to its high diagnostic rate and strong private-payer coverage. The Asia-Pacific region is the fastest-growing with a CAGR of 9.14%. This is attributed to the aging population in Japan and China and the rising insurance coverage in India and ASEAN countries. Europe accounts for the second greatest percentage, at over 28.0%, with national screening programs in Germany, the UK and France continuing to boost detection rates at an early stage. Emerging economies are anticipated to experience continuous double-digit regional pockets of growth in the Peripheral Artery Disease Market through 2035 as screening infrastructure and reimbursement mechanisms improve.

Key Report Takeaways

• By Treatment Type

- Devices accounted for 61.2% of the Peripheral Artery Disease Market in 2025, reflecting the dominance of endovascular platforms and surgical instruments.

- Pharmaceutical therapies are the fastest-growing treatment category, advancing at a 10.72% CAGR through 2035 as novel antiplatelet and lipid-lowering agents gain regulatory traction.

• By End User

- Hospitals controlled 61.5% of the Peripheral Artery Disease Market in 2025, anchored by complex revascularization cases requiring hybrid operating suites.

- Ambulatory surgical centers post the strongest growth at a 10.28% CAGR, benefiting from same-day discharge protocols and lower procedural costs.

• By Disease Stage

- Intermittent claudication represented a 69.5% share of the Peripheral Artery Disease Market in 2025, given its higher prevalence relative to advanced stages.

- Critical limb ischemia procedures are expanding at a 9.24% CAGR, driven by improved limb-salvage technologies.

• By Anatomy Treated

- Lower-extremity arterial procedures captured 83.2% of the Peripheral Artery Disease Market in 2025.

- Renal-visceral interventions are projected to grow at a 10.10% CAGR through 2035.

• By Geography

- North America accounted for 43.7% of the Peripheral Artery Disease Market revenue in 2025.

- Asia-Pacific is the fastest-growing region at a 9.14% CAGR.

Market Size and Forecast (2021–2035)

Market Research Future (MRFR) estimates are based on a combination of bottom-up device and drug sales modeling, hospital procedure volume tracking from national registries, secondary literature from peer-reviewed clinical database and proprietary expert interviews. The historical figures are shipment and prescription data, and the projected predictions employ the 8.10% CAGR calibrated for 2026–2035, conducted across 12 countries.