Pet Oral Care Products Market Summary

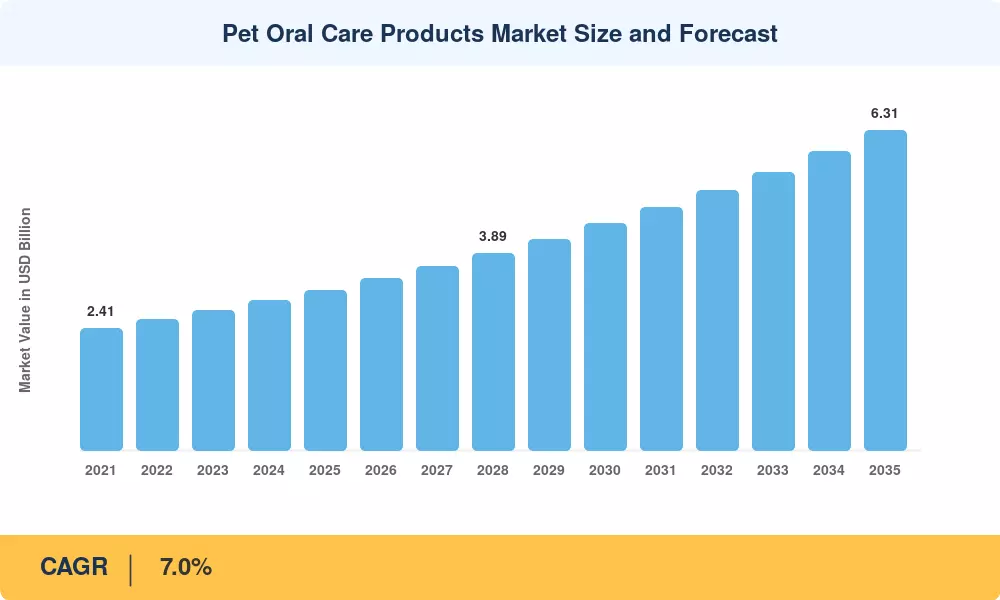

The pet oral care products market reached USD 3.16 billion in 2025, is projected to stand at USD 3.43 billion in 2026, and is forecast to climb to USD 6.31 billion by 2035 at a 7.0% CAGR during 2026–2035. Rising pet ownership rates across North America and Europe, combined with growing awareness that periodontal disease affects roughly eight in ten adult companion animals, are channeling preventive spending toward dog and cat dental hygiene solutions[2]. Veterinarian recommendations and pet insurance expansions have further legitimized routine oral care as a standard household budget line.

A technology-led shift is reshaping how owners approach pet oral care. Traditional manual brushing is giving way to enzymatic formulations, ultrasonic pet toothbrush and toothpaste kits, and AI-enabled plaque-detection cameras that sync with smartphone apps. Functional dental chews and water additives infused with seaweed extracts, postbiotics, and chlorhexidine alternatives now command premium shelf space, with ingredient-innovation investment exceeding USD 420 million globally in 2024 [3]. This transformation is converting one-time buyers into subscription-based recurring customers.

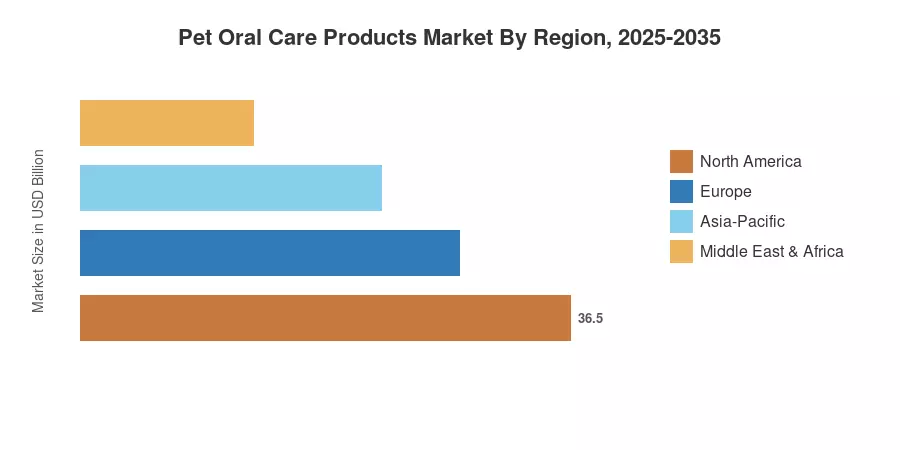

North America held approximately 50.2% of the pet oral care products market in 2025, propelled by the highest per-pet healthcare spending globally. Asia-Pacific is the fastest-growing region at a 7.1% CAGR through 2035, driven by a booming middle class in China and India adopting Western pet-parenting habits. Europe remained the second-largest region, contributing roughly a quarter of global revenue. As telehealth veterinary consultations expand worldwide, the next decade should sustain robust growth for veterinary oral care products and consumer-grade solutions alike.

Key Report Takeaways

• By Product Type

- Dental chews and treats commanded 44.2% of the pet oral care products market share in 2025, reflecting strong consumer preference for convenient, treat-based compliance solutions.

- Oral probiotic tablets are forecast to expand at an 8.0% CAGR through 2035, propelled by microbiome research linking oral health to systemic wellness.

• By Animal Type

- Dogs accounted for a 69.0% share of the pet oral care products market in 2025, underscoring canine dominance in preventive dental spending.

- Cats are advancing at a 6.6% CAGR to 2035, as feline-specific formulations and pet breath freshener products gain traction among cat owners.

• By Distribution Channel

- Online platforms captured 39.4% of revenue in 2025, fueled by auto-replenishment subscriptions and same-day delivery infrastructure.

- Subscription box services are projected to grow at an 8.5% CAGR through 2035.

• By Region

- North America held a 50.2% share of the pet oral care products market in 2025.

- Asia-Pacific is the fastest-growing region at a 7.1% CAGR through 2035.

Pet Oral Care Products Market Size and Forecast (2021–2035)

MRFR's proprietary sizing model integrates primary survey data from 1,200+ veterinary clinics, distributor sell-through reports, and publicly filed revenue disclosures from leading manufacturers. Historical figures (2021–2024) are validated against trade association data and customs statistics; forecast values (2026–2035) apply regression-adjusted growth overlays calibrated to pet population dynamics, disposable income trends, and e-commerce penetration rates.