Pharmaceutical Cartridges Market Summary

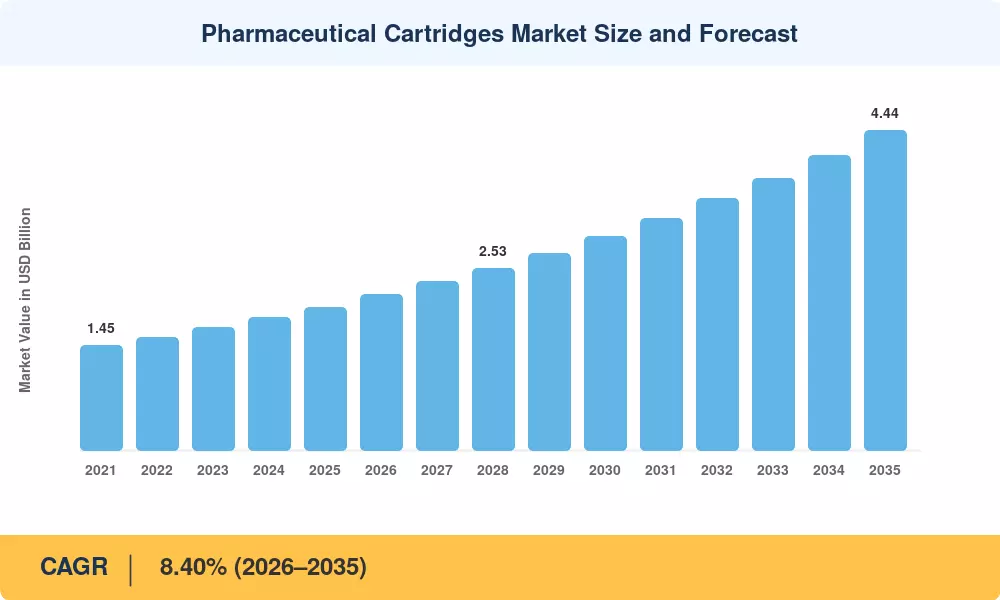

The Global Pharmaceutical Cartridges Market size was valued at USD 1.99 Billion in 2025, and the market is projected to grow from USD 2.15 Billion in 2026 to USD 4.44 Billion by 2035, registering a CAGR of 8.40% during the forecast period 2026–2035. This trajectory is propelled by the rapid migration of biologic therapies into self-administration formats and by the European Union's revised Annex 1 sterility guidelines, which are pushing fill-finish operations toward ready-to-use cartridge configurations that eliminate costly depyrogenation steps [2]. Multibillion-dollar capacity investments announced by leading glass and polymer suppliers in 2024–2025 have further reinforced confidence in the Pharmaceutical Cartridges Market outlook.

A structural technology shift is reshaping this space. Legacy bulk-washed glass cartridges are giving way to pre-sterilized, ready-to-use formats—supported by AI-driven fill-finish automation that has reduced glass breakage rates by up to 40% and halved false rejection rates on inspection lines [3]. Engineering plastics based on cyclic olefin copolymer (COC) and cyclic olefin polymer (COP) are gaining traction for their superior break resistance and chemical inertness, though Type I borosilicate glass still commands the majority of volume across the Pharmaceutical Cartridges Market.

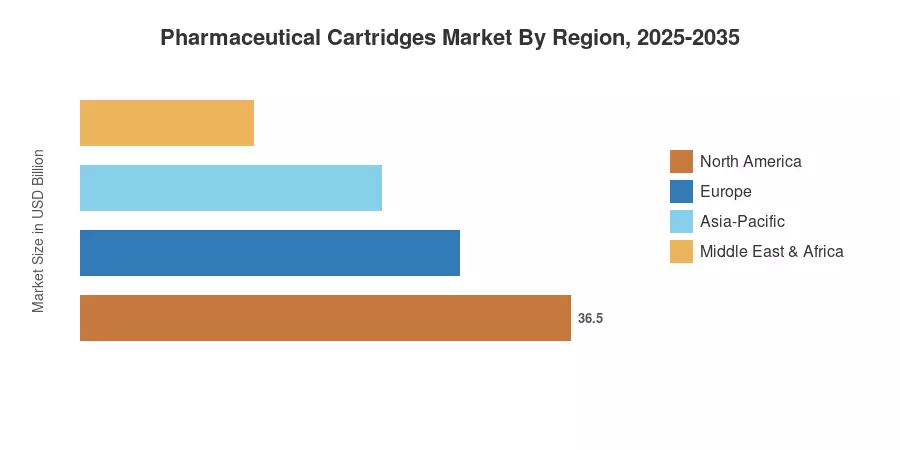

Regionally, North America maintained the largest share of the Pharmaceutical Cartridges Market at approximately 40.9% of global revenue in 2025, anchored by a dense network of contract fill-finish facilities and robust biosimilar uptake [4]. Asia-Pacific is emerging as the fastest-growing region with a projected CAGR of 10.5% through 2035, driven by expanding insulin pen programs in China and India. Europe, the second-largest region, continues to benefit from stringent EU GMP regulations that incentivize high-quality cartridge adoption.

Key Report Takeaways

• By Material

- Glass (Type I borosilicate) accounted for roughly 67.8% of the Pharmaceutical Cartridges Market in 2025, reflecting its dominance across insulin and biologic delivery platforms.

- Engineering plastics (COC/COP) are forecast to expand at a 12.5% CAGR during 2026–2035, the fastest pace among material segments.

• By Delivery Device Compatibility

- Reusable pen injectors held approximately 46.6% revenue share of the Pharmaceutical Cartridges Market in 2025.

- Wearable on-body delivery pumps are projected to grow at an 11.8% CAGR through 2035, outpacing all other device categories.

• By Therapeutic Area

- Diabetes represented the leading therapeutic segment with a 25.8% share of the Pharmaceutical Cartridges Market in 2025.

- Oncology cartridge demand is anticipated to rise at a 13.1% CAGR as antibody-drug conjugates shift to cartridge-based delivery.

• By Region

- North America captured 40.9% of the Pharmaceutical Cartridges Market in 2025, driven by large-scale fill-finish expansions.

- Asia-Pacific is poised to register the highest regional CAGR of 10.5% during 2026–2035.

Pharmaceutical Cartridges Market Size and Forecast (2021–2035)

Market Research Future derived the historical market size using a combination of bottom-up revenue modeling across cartridge manufacturers, validated against top-down pharmaceutical packaging benchmarks from WHO, IQVIA, and trade association databases. Forecast projections apply the calibrated 8.40% CAGR for 2026–2035 with adjustments for regulatory adoption curves and capacity ramp-ups[5].