Pneumonia Testing Market Summary

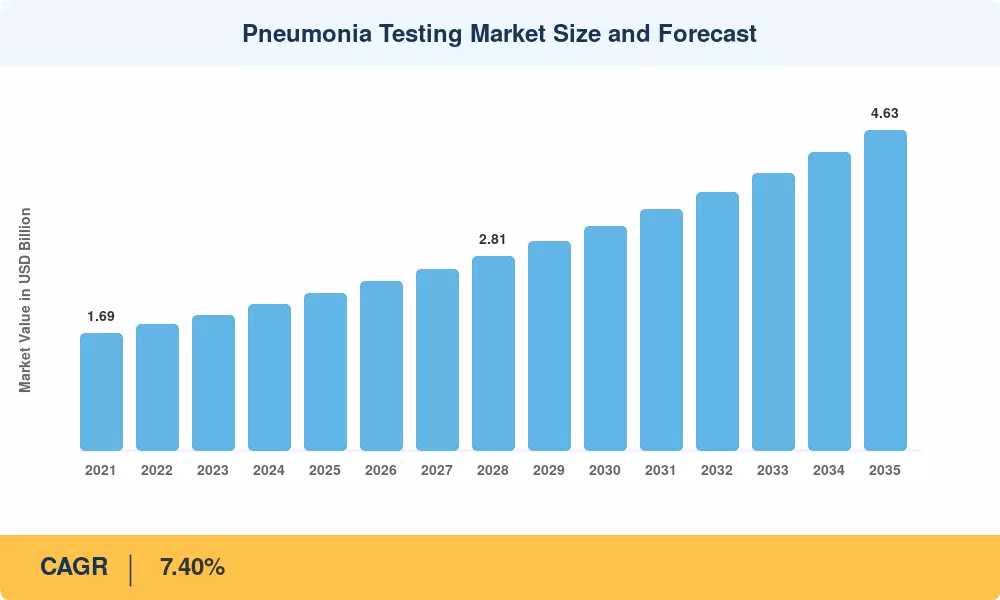

The Global Pneumonia Testing Market size was valued at USD 2.27 Billion in 2025, and the market is projected to grow from USD 2.44 Billion in 2026 to USD 4.63 Billion by 2035, registering a CAGR of 7.40% during the forecast period 2026–2035. This expansion is anchored in the global pneumonia burden — which the WHO estimates kills over 2.5 million people annually, including 700,000 children under five — and in the escalating adoption of rapid point-of-care diagnostics across primary care networks [1]. Government-led immunization campaigns and antimicrobial stewardship programs in both developed and emerging economies continue to intensify demand for accurate pathogen identification at the bedside.

A decisive shift is underway from conventional culture-based methods toward molecular and antigen-based platforms that deliver results within 15–45 minutes rather than 24–72 hours. The U.S. CDC's Advanced Molecular Detection initiative has directed over USD 170 million since its inception toward next-generation respiratory surveillance infrastructure, accelerating the integration of multiplex PCR and isothermal amplification panels into hospital emergency departments and urgent care clinics [2]. Point-of-care analyzers now account for a rapidly growing share of new installations, displacing centralized laboratory workflows in both high- and low-resource settings.

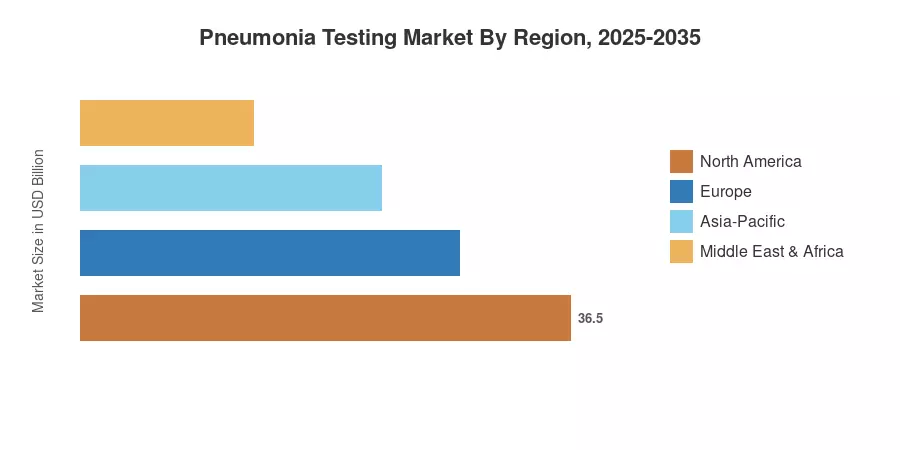

North America commands the largest share of the Pneumonia Testing Market at approximately 38.5% of global revenue, driven by high test utilization rates and robust reimbursement frameworks. Asia-Pacific is the fastest-growing region with a projected CAGR exceeding 9.1%, propelled by expanding hospital infrastructure in India and China and growing public health investment across ASEAN nations. Europe holds the second-largest regional position at roughly 27% share, supported by harmonized IVD regulatory frameworks and strong reference laboratory networks. The decade ahead will see decentralized testing architectures reshape how pneumonia is diagnosed worldwide.

Key Report Takeaways

• By Type

- Consumables dominate the Pneumonia Testing Market, accounting for approximately 63% of total revenue in 2025, reflecting recurring spend on reagent kits, cartridges, and assay panels.

- Analyzers are forecast to expand at the highest CAGR of 8.2% through 2035, as hospitals invest in next-generation multiplex platforms.

• By Method Type

- Molecular diagnostics hold the largest share of the Pneumonia Testing Market by method type, driven by PCR and isothermal amplification adoption.

- Urinary antigen testing is projected to grow at a CAGR of 7.8%, gaining traction in emergency department triage workflows.

• By Region

- North America leads the Pneumonia Testing Market with USD 0.87 Billion in 2025 revenue.

- Asia-Pacific is set to be the fastest-growing regional segment over 2026–2035, registering a CAGR above 9%

- Europe maintains the second-largest position, underpinned by established laboratory networks and regulatory incentives.

Market Size and Forecast (2021–2035)

Market Research Future's estimates draw on a triangulated methodology combining primary interviews with hospital procurement officers, laboratory directors, and diagnostics manufacturers, validated against regulatory filings, import/export databases, and publicly reported company revenues. Historical values (2021–2024) reflect audited company disclosures and syndicated datasets; forecast values (2026–2035) apply a steady-state CAGR anchored to verified demand drivers.