Polymer Filler Market Summary

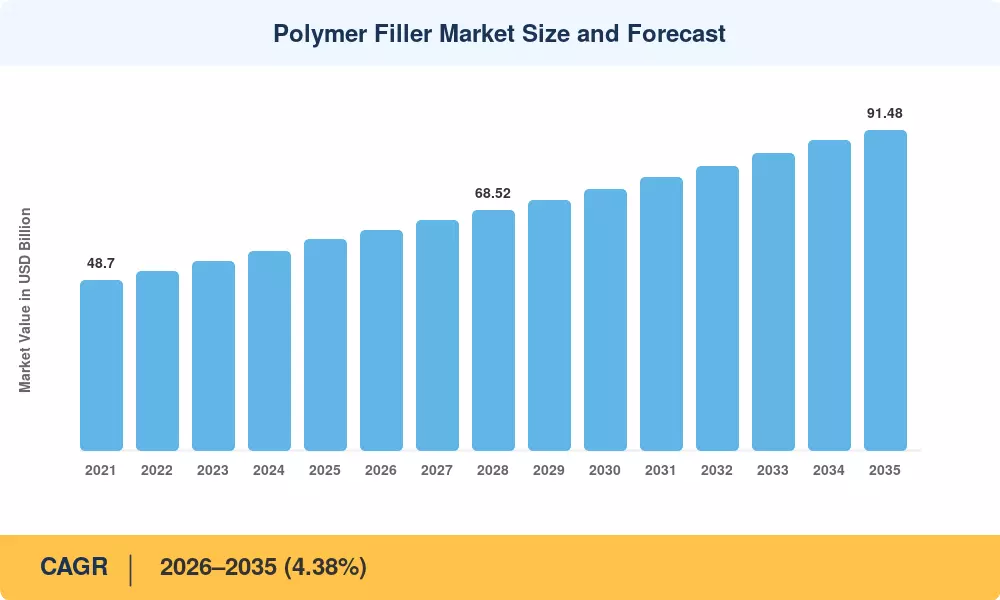

The Polymer Fillers Market reached an estimated USD 60.32 billion in 2025 and is projected to grow from USD 62.89 billion in 2026 to USD 91.48 billion by 2035, registering a CAGR of 4.38% during the forecast period. Two catalysts are reshaping demand: tightening lightweight-vehicle mandates under Euro 7 emission norms and an infrastructure spending surge anchored by the U.S. Bipartisan Infrastructure Law, which earmarks over USD 550 billion for roads, bridges, and utilities that consume large volumes of calcium carbonate fillers and thermoplastic compounds [2][3].

A generational shift is underway in how formulators select plastic filler materials. Legacy single-function extenders—primarily ground calcium carbonate used to cut resin costs—are giving way to engineered mineral fillers that simultaneously reinforce stiffness, improve flame retardancy, and lower carbon footprint. Global investment in surface-treated and nano-grade functional fillers exceeded USD 4.2 billion in 2024, signaling that compounders now treat talc fillers, precipitated silica, and bio-based organic grades as performance-critical polymer additives rather than commodity dilutants [4][5].

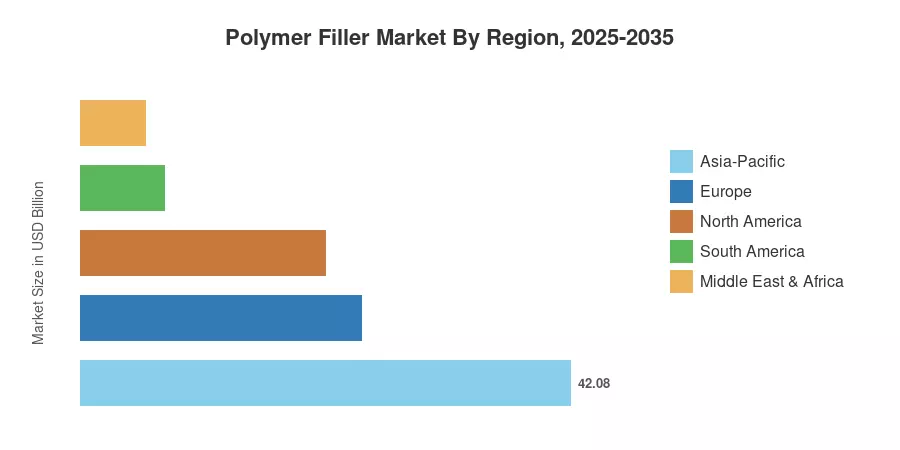

Asia-Pacific commands approximately 42% of the Polymer Fillers Market, driven by capacity expansions across China and India. The region is also the fastest-growing, with a projected CAGR of 5.68% through 2035. Europe holds the second-largest share at roughly 24%, buoyed by circular-economy regulations that favor recycled-content reinforcing fillers. North America contributes a steady demand through EV battery-housing applications and residential construction recovery. As composite filler materials penetrate new end uses—from 3D-printed building panels to flexible electronics substrates—the Polymer Fillers Market is poised for sustained expansion well into the next decade [6][7].

Key Report Takeaways

• By Product Type

- Inorganic fillers—including calcium carbonate fillers, silica, and talc fillers—held a 72.46% revenue share of the Polymer Fillers Market in 2025, reflecting their cost-performance advantage in high-volume thermoplastic compounds

- Organic filler grades are forecast to expand at a 5.48% CAGR through 2035, propelled by demand for bio-based and natural-fiber reinforcing fillers in automotive interiors

• By Polymer Matrix

- Thermoplastic fillers accounted for 57.16% of the Polymer Fillers Market in 2025, with polypropylene and polyethylene remaining the largest resin platforms for mineral fillers

- Elastomer-based applications are advancing at a 5.27% CAGR, fueled by EV vibration-damping components that rely on functional fillers for noise reduction

• By End-User Industry

- Building and construction held USD 23.38 billion of the Polymer Fillers Market value in 2025, anchored by PVC pipe, roofing membranes, and insulation panels loaded with calcium carbonate fillers

- Automotive and transportation segments are projected to grow at a 5.84% CAGR to 2035 as lightweighting targets accelerate the adoption of composite filler materials

• By Region

- Asia-Pacific captured 42.08% of the Polymer Fillers Market in 2025 and is expected to register a 5.68% CAGR through 2035

- North America's share stood at approximately 21% in 2025, supported by EV incentives and infrastructure renewal programs

Market Size and Forecast (2021–2035)

The historical and forecast data below draw on MRFR's proprietary bottom-up model, triangulated against trade association shipment data, customs records, and annual reports from leading mineral fillers producers. Base-year 2025 figures reflect actual production volumes, while 2026–2035 projections apply a compound growth framework calibrated to macroeconomic indicators and regional capacity pipelines.