Polyurethane Foam Market Summary

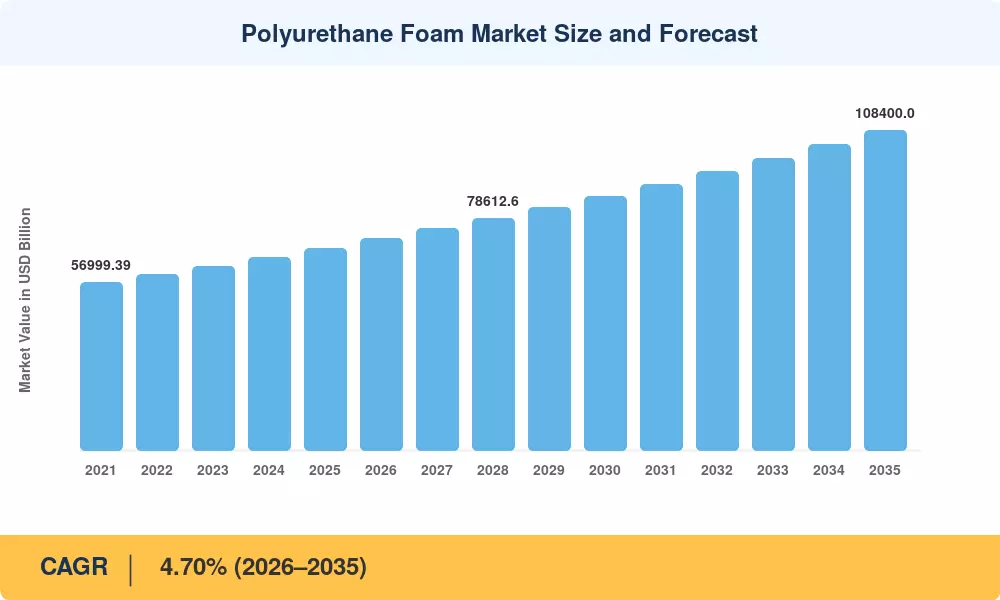

The Polyurethane Foam Market reached an estimated USD 68,500 Million in 2025 and is projected to grow from USD 71,700 Million in 2026 to USD 108,400 Million by 2035, registering a CAGR of 4.70% during the forecast period. Tightening energy-efficiency mandates—including Europe's revised Energy Performance of Buildings Directive and the United States' 2024 International Energy Conservation Code—are converting optional rigid foam insulation upgrades into compliance-driven purchases, pulling baseline demand upward across commercial and residential construction [2]. At the same time, the electric-vehicle production ramp is creating entirely new specification windows for automotive foam materials used in battery-pack thermal enclosures and lightweight interior modules [3].

A technology shift is reshaping how polyurethane insulation reaches job sites. Conventional slab-stock and pour-in-place processes are steadily giving way to spray polyurethane foam systems that deliver high R-values in irregular cavities, cut installation labor by up to 40%, and seal air leakage paths that rigid boards miss [4]. The International Energy Agency estimates that buildings still account for roughly 30% of global final energy consumption, a statistic that continues to funnel public and private capital into advanced insulation foam products [5].

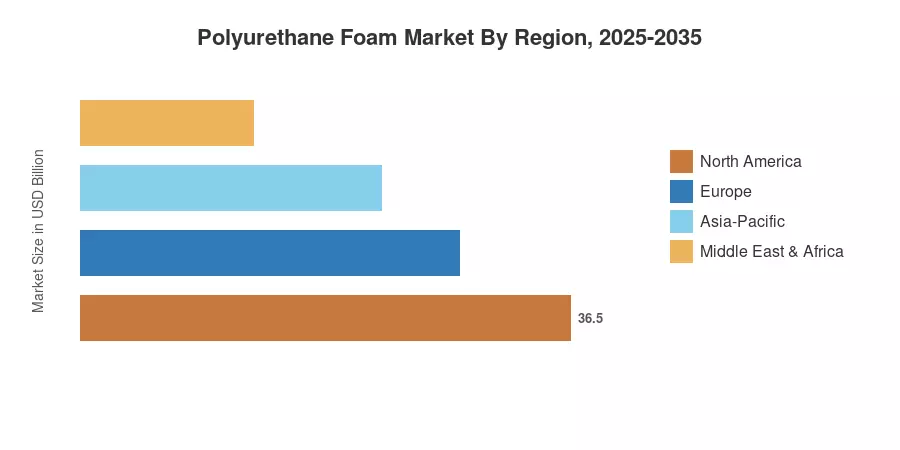

Asia-Pacific commands approximately 46% of global consumption, driven by China's GB 50189-2024 building standard and India's rapid urbanization cycle. The region is also the fastest-growing, expanding at an estimated 5.80% CAGR through 2035. North America holds the second-largest position with around 23% share, buoyed by cold-chain logistics investment and residential retrofit activity. Europe follows closely, where circular-economy directives are accelerating bio-based polyol adoption and reshaping the competitive landscape for cushioning foam solutions and flexible polyurethane foam producers alike [6].

Key Report Takeaways — Polyurethane Foam Market

By Type

- Flexible polyurethane foam accounted for roughly 52% of volume in 2025, anchored by bedding, furniture, and automotive seating demand.

- Rigid foam insulation is forecast to expand at a 5.10% CAGR through 2035, propelled by building energy codes and cold-chain infrastructure.

- Other foam types—integral-skin, viscoelastic, and spray formats—are projected to post the fastest segment CAGR of 7.00% through 2035.

By End-Use Industry

- Building and construction absorbed approximately 38% of the Polyurethane Foam Market in 2025, the single largest demand center.

- Packaging is advancing at a leading 7.80% CAGR, fueled by e-commerce protective packaging and pharmaceutical cold-chain requirements.

- Automotive foam materials consumed an estimated USD 9,200 Million in 2025, reflecting lightweighting and EV-specific thermal management needs.

By Region

- Asia-Pacific dominated with a 46% share in 2025, led by China and India.

- North America held roughly 23% of global revenue, supported by residential insulation retrofits and industrial foam products demand.

- South America is projected to record a 5.40% CAGR through 2035, the fastest among emerging regions outside Asia-Pacific.

Polyurethane Foam Market Size and Forecast (2021–2035)

Market size estimates draw on MRFR's proprietary modeling framework, triangulated against industry shipment data, trade statistics, and manufacturer disclosures. Historical values (2021–2024) are actuals; 2025 is the calibrated base year; 2026–2035 are forecasts anchored to a 4.70% compound annual growth rate.