Private LTE Market Summary

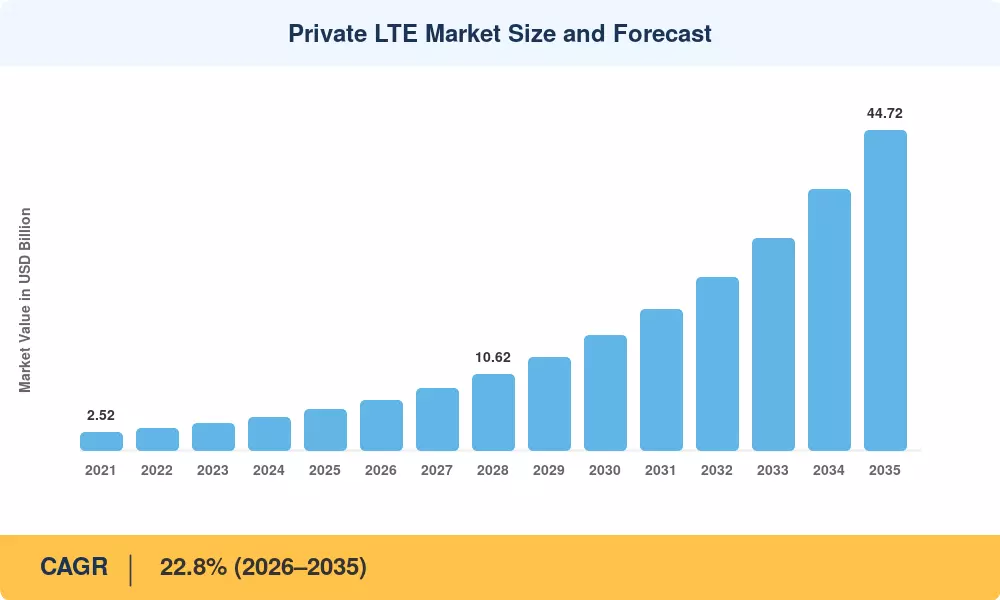

The Private LTE Market reached an estimated USD 5.57 billion in 2025 and is projected to climb to USD 7.04 billion in 2026 before expanding to USD 44.72 billion by 2035, reflecting a 22.8% CAGR across the forecast window. Accelerated enterprise digitization and the U.S. FCC's continued CBRS spectrum releases are catalyzing demand for campus LTE deployment across logistics hubs, factory floors, and remote extraction sites. Governments in Germany, Japan, and South Korea have earmarked dedicated private 4G spectrum bands, creating regulatory pull that commercial carriers alone cannot satisfy [2].

Legacy Wi-Fi and wired Ethernet backbones are rapidly giving way to enterprise LTE networks capable of deterministic latency below 10 ms and seamless handover across large industrial footprints. The World Economic Forum's 2024 "Advanced Manufacturing" initiative pegged Industry 4.0 connectivity spending at USD 78 billion globally, of which on-premise LTE solutions represent a fast-rising share [3]. Open RAN architectures and small-cell innovations are driving down the total cost of ownership by 25–30%, making industrial private wireless economically viable even for mid-sized plants.

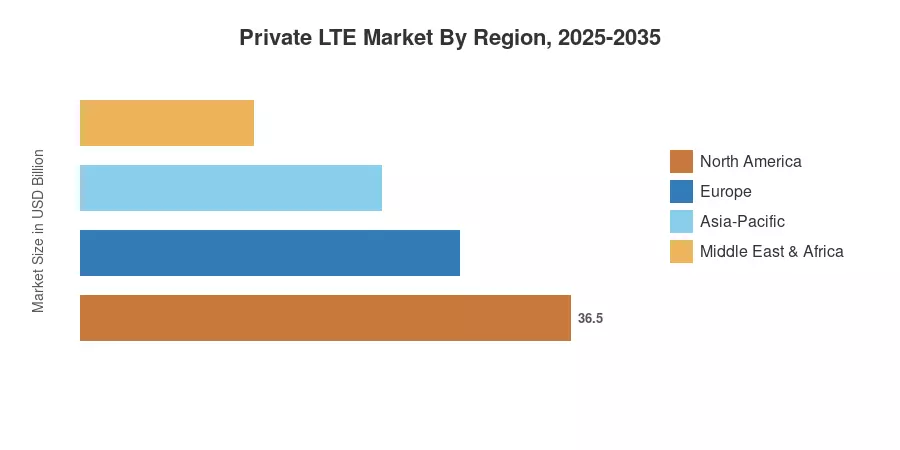

North America commanded roughly 34.8% of the Private LTE Market in 2025, buoyed by CBRS adoption and defense-sector mandates. Asia-Pacific is the fastest-growing region, propelled by smart-factory programs in China, India, and South Korea. Europe held the second-largest share at approximately 26.1%, led by Germany's "local 5G" licensing framework that doubles as a gateway for dedicated private 4G rollouts [4]. The convergence of edge computing, AI-driven analytics, and private cellular infrastructure will reshape enterprise connectivity through 2035.

Key Report Takeaways

• By Component

- Infrastructure dominated the Private LTE Market with a 57.8% revenue share in 2025, reflecting heavy capex on evolved packet core, eNodeB radios, and backhaul gear.

- Managed services are forecast to register a 16.3% CAGR through 2035 as enterprises outsource network operations to specialized integrators.

• By Technology & Deployment

- TDD captured 50.5% of revenue in 2025, favored for its spectral efficiency in campus LTE deployment scenarios.

- Distributed architecture accounted for 53.1% of the Private LTE Market share in 2025, preferred for multi-site industrial private wireless coverage.

• By End-User

- Manufacturing led end-user verticals with a 26.4% share, driven by AGV navigation and real-time MES integration across enterprise LTE networks.

• By Region

- North America retained dominance at 34.8% share; Asia-Pacific's CAGR leads all regions through 2035.

Market Size and Forecast (2021–2035)

MRFR's estimates integrate primary surveys of 120+ network integrators, public procurement databases, and vendor revenue disclosures. Historical figures are validated against ITU broadband deployment data and national spectrum auction records.