Purging Compound Market Summary

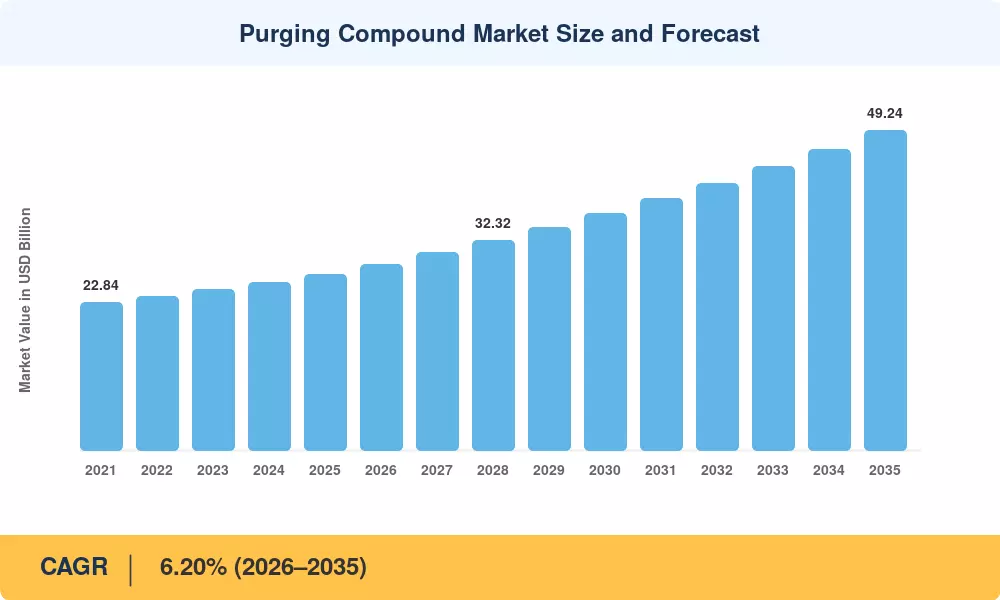

The Purging Compound Market reached an estimated 27.10 kilotons in 2025 and is poised to grow from 28.65 kilotons in 2026 to 49.24 kilotons by 2035, registering a CAGR of 6.20% across the forecast period. Two converging forces are accelerating demand: the global shift toward high-performance engineering polymers in electric-vehicle battery enclosures, and tightening environmental regulations—such as the EU's revised Industrial Emissions Directive (2024/xx)—that penalize excessive resin waste during color and material changeovers. Processors that once tolerated 15–20 kg of transition scrap per changeover are now under pressure to cut that figure by half, pushing adoption of advanced purge formulations [1].

The technology landscape is transforming. Conventional virgin-resin purging—where operators simply ran production-grade material until the barrel cleared—is giving way to engineered mechanical and chemical purge grades that slash changeover times from 45 minutes to under 10 minutes. Capital investment in smart dosing systems exceeded USD 120 million globally in 2024, according to plastics-industry capital-expenditure trackers, as Industry 4.0 plants integrate automated purge cycles into their MES platforms.

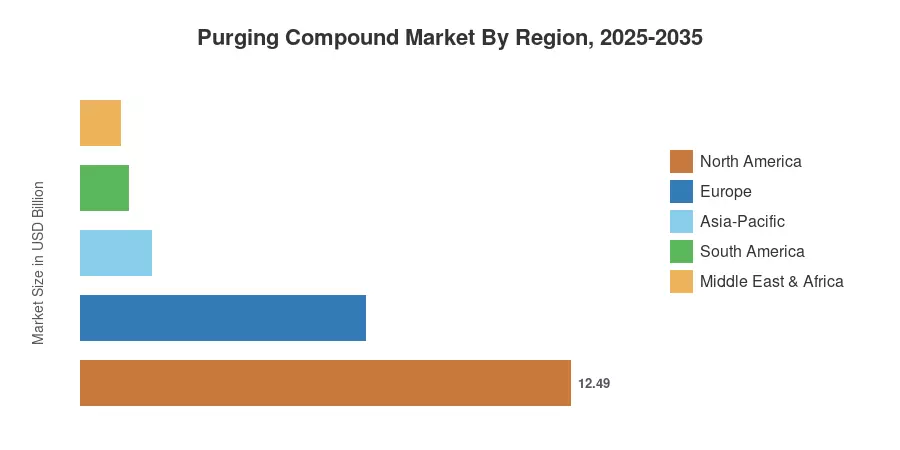

North America commanded a 46.1% share of the Purging Compound Market in 2025, underpinned by a mature automotive supply chain that enforces zero-defect part standards. Asia-Pacific is the fastest-growing region at a 6.64% CAGR, propelled by China's surging EV output and India's expanding consumer-electronics manufacturing base. Europe holds the second-largest position with a 26.8% share, where stringent sustainability mandates continue to drive processor upgrades. As lightweighting and multi-material designs proliferate, the Purging Compound Market is expected to become an indispensable component of lean plastics manufacturing through 2035.

Key Report Takeaways

• By Type

- Mechanical purge products accounted for 51.2% of the Purging Compound Market volume in 2025, driven by their compatibility with a broad range of commodity and engineering resins.

- Chemical purge formulations are forecast to register a 6.45% CAGR through 2035 as processors seek faster carbon-deposit removal in hot-runner systems.

• By Process

- Injection molding held a 54.8% volume share of the Purging Compound Market in 2025, reflecting high changeover frequency in automotive and consumer-goods molding.

- Extrusion applications are expanding at a 6.30% CAGR as film and sheet producers adopt scheduled purge protocols to reduce gel contamination.

• By Application

- Automotive and transportation captured 23.2% of the Purging Compound Market volume in 2025 on the back of strict cosmetic and structural part specifications.

- Electronics end-use is growing at the fastest segment CAGR of 6.55%, fueled by miniaturized connector housings that tolerate zero color contamination.

• By Region

- North America retained a 46.1% share of the Purging Compound Market in 2025, while Asia-Pacific is advancing at a 6.64% CAGR.

Market Size and Forecast (2021–2035)

Market Research Future's volume estimates combine bottom-up processor surveys across 22 countries with top-down resin-consumption triangulation, validated against trade-flow databases and manufacturer shipment disclosures. Historical figures (2021–2024) reflect actual reported volumes; the 2025 base year incorporates preliminary shipment data, and the 2026–2035 forecast applies the calibrated 6.20% CAGR with adjustments for anticipated capacity expansions in Asia-Pacific and South America.