Compound Feed Market Summary

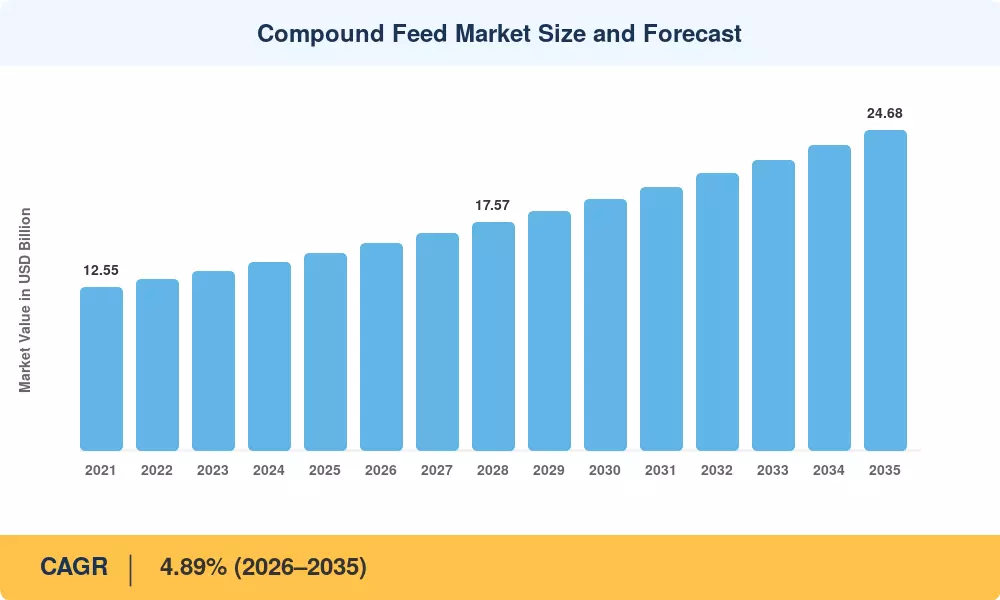

The Compound Feed Market reached a valuation of USD 15.19 Billion in 2025, with an estimated starting forecast value of USD 15.93 billion in 2026 and a projected endpoint of USD 24.68 billion by 2035, expanding at a CAGR of 4.89% across the forecast period. National food-security mandates — including the EU's Farm to Fork Strategy targeting a 50% reduction in antimicrobial use by 2030 and China's 14th Five-Year Plan earmarking over USD 12 billion for livestock modernization — continue to propel balanced livestock feed formulation investment globally [1]. The push toward self-sufficiency in animal protein production, particularly across South and Southeast Asia, is accelerating procurement volumes at an unprecedented pace.

A comprehensive technical revolution is reshaping the production of compound feed. Legacy hammer-mill and batch-mixing systems are being replaced with precision-dosing platforms, near-infrared (NIR) real-time quality analyzers and IoT-connected extrusion lines. Producers seeking better nutrient homogeneity and fewer waste drove an expected USD 1.7 billion in capital expenditures for the worldwide smart-feed-mill equipment industry in 2024 alone [2]. Regulatory pressure on antibiotic growth promoters is reshaping poultry compound feed ingredients and ruminant complete feed blend formulations towards enzyme-based and probiotic alternatives, with the EU’s complete ban effective January 2022 and similar phase-downs under India’s National Action Plan on AMR.

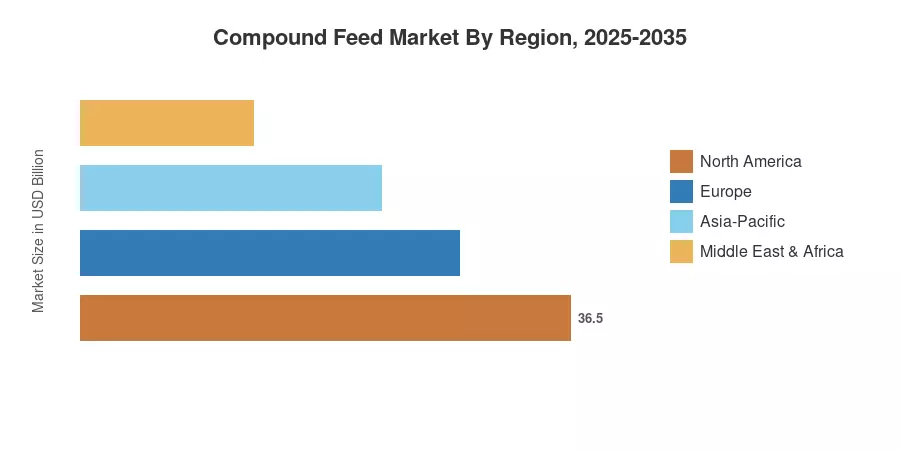

The revenue share of North America in the Compound Feed Market is at 29%, with vertical integration in the US Midwest and the growing poultry market in Mexico. The Asia-Pacific is the fastest-expanding region with a CAGR of 6.12% expected till 2035, driven by increasing per-capita meat consumption in China and India. Europe comes second with the highest market of around 26%, and here, stricter sustainability rules are driving innovation in aquafeed compound nutrition. In emerging economies, where protein demand curves are steepening, the Compound Feed Market will see sustained structural expansion over the next decade

Key Report Takeaways

• By Animal Type

- Poultry dominated the Compound Feed Market with approximately 48% share in 2025, reflecting the birds' superior feed-conversion ratio and short production cycles

- Aquaculture is projected to register the fastest CAGR of 9.34% through 2035, driven by government aquaculture expansion programs and rising aquafeed compound nutrition demand

- Ruminant complete feed blend accounted for roughly USD 3.41 billion in 2025 as dairy intensification accelerated across South Asia and Latin America

• By Ingredient

- Cereals represented 56% of the Compound Feed Market in 2025, with corn and wheat remaining the dominant energy substrates

- Supplements are tracking a 10.18% CAGR through 2035 as producers shift toward precision micro-nutrient and enzyme dosing

• By Feed Form

- Pellets held 63% revenue share in 2025, benefiting from superior storage stability and automated feeding-line compatibility in the Compound Feed Market

- Extruded feeds are expanding at a 10.84% CAGR as aquafeed compound nutrition applications and high-fat poultry diets gain traction

• By Region

- North America controlled roughly 29% of the Compound Feed Market in 2025; Asia-Pacific is set to register the highest regional CAGR of 6.12% to 2035

- Europe's Compound Feed Market accounted for approximately 26% share, with sustainability mandates underpinning balanced livestock feed formulation upgrades

Compound Feed Market Size and Forecast (2021–2035)

MRFR’s market sizing is based on bottom-up production-volume analysis across 40+ countries and top-down revenue calibration based on trade databases (UN Comtrade, FAO), corporate financials, and exclusive primary surveys of 200+ feed-mill operators throughout the globe.