Rabies Diagnostics Market Summary

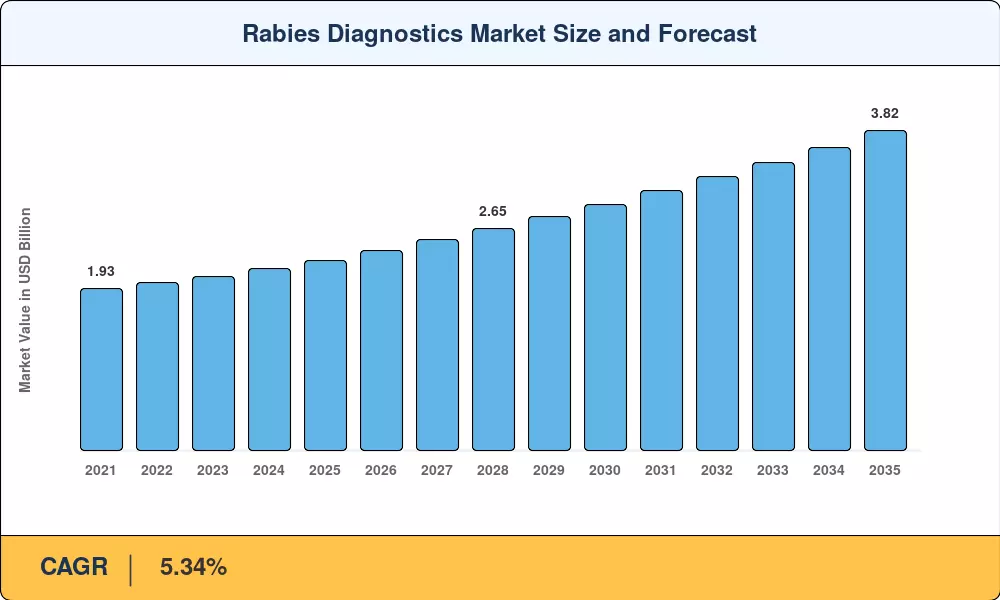

The Global Rabies Diagnostics Market size was valued at USD 2.27 Billion in 2025, and the market is projected to grow from USD 2.39 Billion in 2026 to USD 3.82 Billion by 2035, registering a CAGR of 5.34% during the forecast period 2026–2035. Two catalysts are driving this trajectory: the WHO-led "Zero by 2030" global framework for eliminating dog-mediated human rabies deaths, and a parallel surge in national One-Health surveillance budgets that now exceed USD 320 million annually across priority countries [1]. Governments in South and Southeast Asia have committed fresh procurement funding for decentralized testing, while the U.S. CDC expanded its cooperative agreement for wildlife rabies oral vaccination and monitoring programs [2].

A technological transition is transforming the rabies diagnostics market. The gold standard for over four decades, legacy fluorescent antibody testing, is gradually losing ground to real-time PCR platforms and isothermal amplification kits. These technologies provide results in under ninety minutes without the need for cryostat-equipped laboratories [3]. Between 2022 and 2024, the Gavi Alliance allocated USD 155 million to fortify the integrated vaccine-and-diagnostic supply chains of 18 Gavi-eligible nations. This initiative established a direct conduit for the rapid adoption of next-generation diagnostics [4]. By the late 2020s, traditional assay economics could be disrupted by CRISPR-based detection systems, which are currently in the proof-of-concept stage.

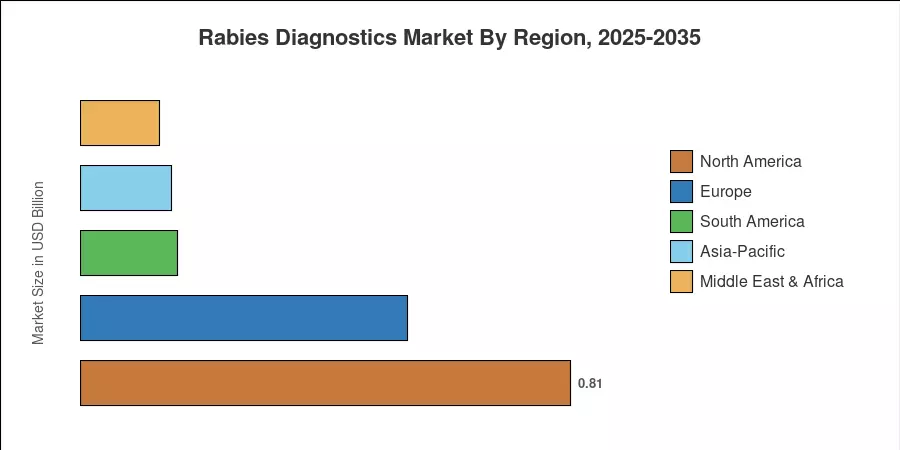

The Rabies Diagnostics Market is dominated by North America, which is responsible for approximately 35.7% of global revenue in 2024. This dominance is attributed to the continent's wildlife management infrastructure and mandatory post-exposure testing protocols [5]. Asia-Pacific is the fastest-growing region, with a projected compound annual growth rate (CAGR) of 6.67%. This growth is being driven by the National Action Plan for the Elimination of Dog-Mediated Rabies in India and the upgrading of provincial laboratories in China. Supported by EU-funded cross-border wildlife rabies monitoring programs, Europe is the second-largest region, with an approximate 24.0% share. The convergence of digital sample-tracking, portable molecular instruments, and expanded cold-chain logistics will revolutionize the manner in which rabies testing is conducted and the locations where it takes place over the next decade.

Key Report Takeaways

• By Diagnostic Method

- The Fluorescent Antibody Test accounted for approximately 44.1% of the Rabies Diagnostics Market in 2024, reflecting its entrenched role in reference-lab workflows.

- PCR and RT-PCR-based platforms are forecast to expand at an 8.89% CAGR through 2035, driven by demand for ante-mortem and field-deployable confirmation.

• By Technology

- Immunodiagnostics represented the largest technology segment in the Rabies Diagnostics Market during 2024, capturing a 57.2% revenue share.

- Molecular diagnostics will record the highest segment CAGR at 9.37% through 2035.

• By Sample Type & End User

- Brain tissue sampling held a 50.0% share of the Rabies Diagnostics Market in 2024; saliva-based testing is projected to grow at 6.88% CAGR as ante-mortem protocols expand.

• By End user

- Reference laboratories retained a 47.4% share in 2024, while point-of-care and veterinary clinics are set to post the fastest growth at 7.83% CAGR through 2035.

• By Geography

- North America led the Rabies Diagnostics Market with a 35.7% share in 2024.

- Asia-Pacific is expected to register the fastest regional CAGR of 6.67% during the forecast period.

Market Size and Forecast (2021–2035)

Market Research Future's sizing model combines primary interviews with diagnostic-kit manufacturers, reference-laboratory procurement officers, and veterinary public-health agencies alongside secondary data from the WHO, OIE (WOAH), CDC, and peer-reviewed surveillance literature. Historical figures reflect actual shipment revenues adjusted for distributor margins, while forecast values apply a calibrated CAGR anchored to the 2025 base year.